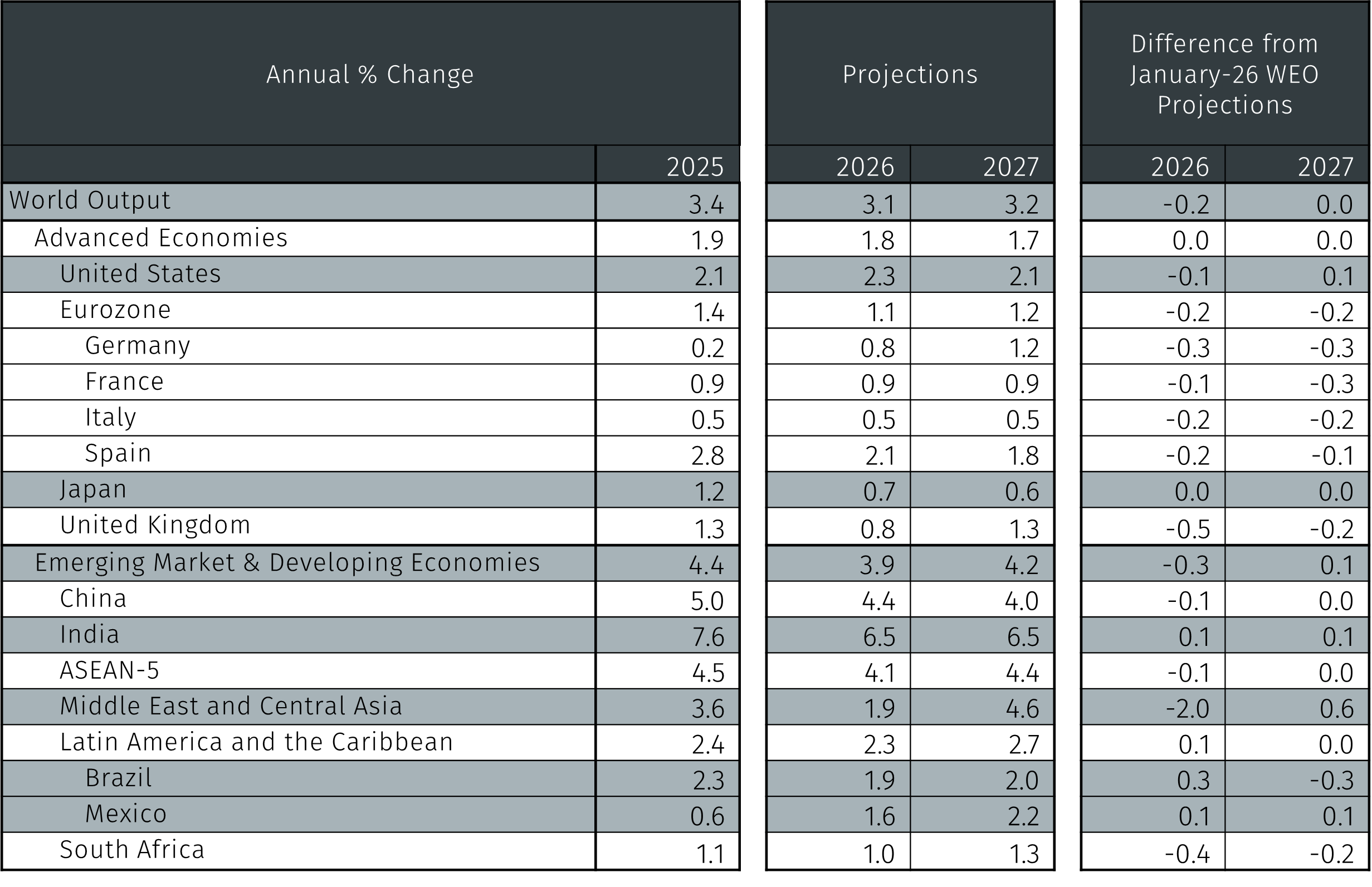

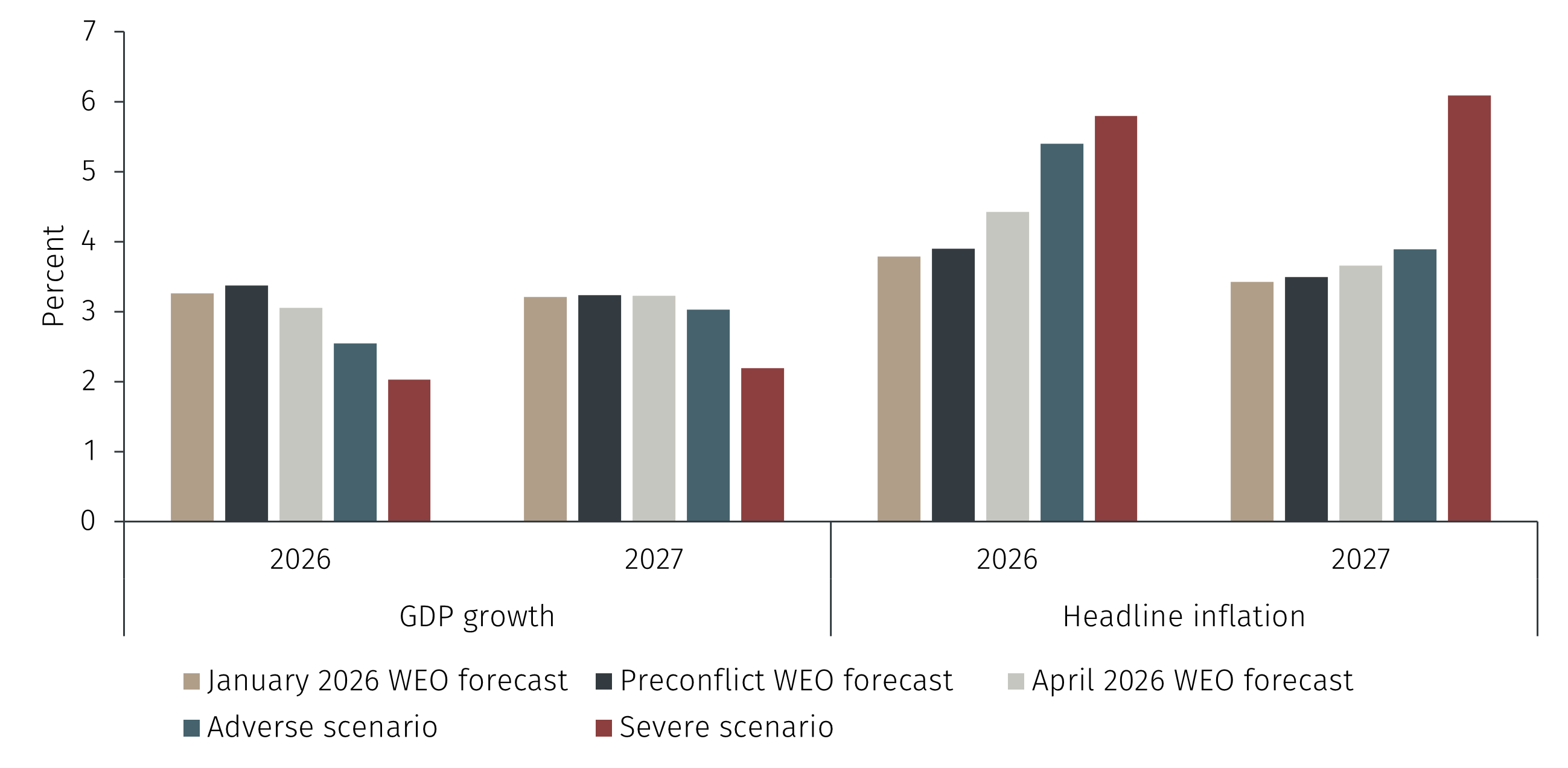

According to the IMF’s latest WEO, economies around the world face several repercussions related to the conflict in the Middle East, for example through the direct impact of higher commodity prices, indirect second-round effects on inflation and risks to financial market sentiment. At the same time, the outbreak of war introduced a level of uncertainty that makes it difficult to rely on a single-path projection. To deal with this, the IMF provides three sets of forecasts to capture different possible states of the world. The reference forecast assumes the Middle East conflict remains limited in duration, with disruptions fading by mid-2026, consistent with commodity futures pricing as of 10 March.1

Absent the war, 2026 global growth would have been revised upward relative to the January 2026 WEO. Stronger-than-expected data at the end of 2025 and lower effective US tariff rates had laid the groundwork for a more optimistic picture. Instead, the IMF revised down the 2026 growth outlook, due almost entirely to the impact of the war. On this basis, the IMF expects global growth to be 3.1% in 2026, down from January’s forecast of 3.3%. It should be noted that the reduction simply returns the 2026 growth forecast back to where it was in October last year, albeit with some regional variations.