The EU Carbon Border Adjustment Mechanism (CBAM)

After a two-year preparation phase, CBAM regulation was enforced at the beginning of 2026, representing a structural shift in how economic systems price carbon.

Together with the ETS (Emissions Trading System), CBAM completes the EU framework to tax greenhouse gas (GHG) emissions. While ETS focuses on emissions produced within EU, the CBAM aims to prevent "carbon leakage," i.e. the relocation of emissions-intensive industries to regions with weaker climate policies, by imposing a carbon cost on imports of selected goods. Importers of products such as steel, cement, aluminium, fertilizers, and hydrogen must purchase CBAM certificates covering the embedded emissions of those imports. The price of these certificates is designed to be equivalent to the EU ETS carbon price, ensuring that foreign producers face the same effective carbon cost as EU producers. The taxation will increase in steps reaching 100% of the embedded carbon emissions of imported goods by 2035. Its scope is set to gradually expand by 2030 to include petroleum products, organic chemicals (polymers), and other industrial gases, covering more sectors and potentially downstream goods like cars.1

CBAM not only ensures EU industries aren't disadvantaged compared to foreign competitors, but in doing so, it extends carbon pricing to global supply chains, encouraging producers outside the EU to adopt stronger carbon pricing or cleaner technologies.2

CBAM’s supporters and opposition

The mechanism is creating some tensions and major EU trading partners have voiced strong objections, labelling CBAM unilateral and potentially trade-distorting, arguing it may violate World Trade Organization (WTO) principles and unfairly penalize developing economies.3 Russia even initiated a WTO dispute regarding EU’s carbon border adjustment and emissions trading schemes.4

The EU on the other hand views CBAM as a fair measure as it aligns the carbon taxation, and it creates an incentive for emissions reductions and the creation of regional homogeneous carbon pricing policies. When a comparable carbon price is paid in the country of origin, that amount is deducted from the CBAM and the countries of origin can retain the proceeds rather than seeing them transferred to the EU, thereby increasing fiscal revenues. Unsurprisingly many jurisdictions – including Canada, the United States, Australia, Taiwan, the United Kingdom and Turkey – are defining or exploring similar policies on their own.5

CBAM stepping in as free allowances phase out

The introduction of the CBAM is structurally linked to the progressive phase-out of free allowances allocated to European industries under ETS I (a process set to take place between 2026 and 2034) increasing the overall scarcity of permits in the carbon market, and potentially pushing carbon prices up by 50% in the next five years.6

European companies are lobbying to soften part of the rules, usually ETS related, and tighten others. The EU is expected to continue revising both ETS and CBAM regulations over the next few months and years and some industries (e.g. fertiliser) may even be temporarily exempted given possible impacts on agricultural prices. However, while changes are to be expected, we do not foresee major adjustments, not least because of significant revenues already included in fiscal planning.

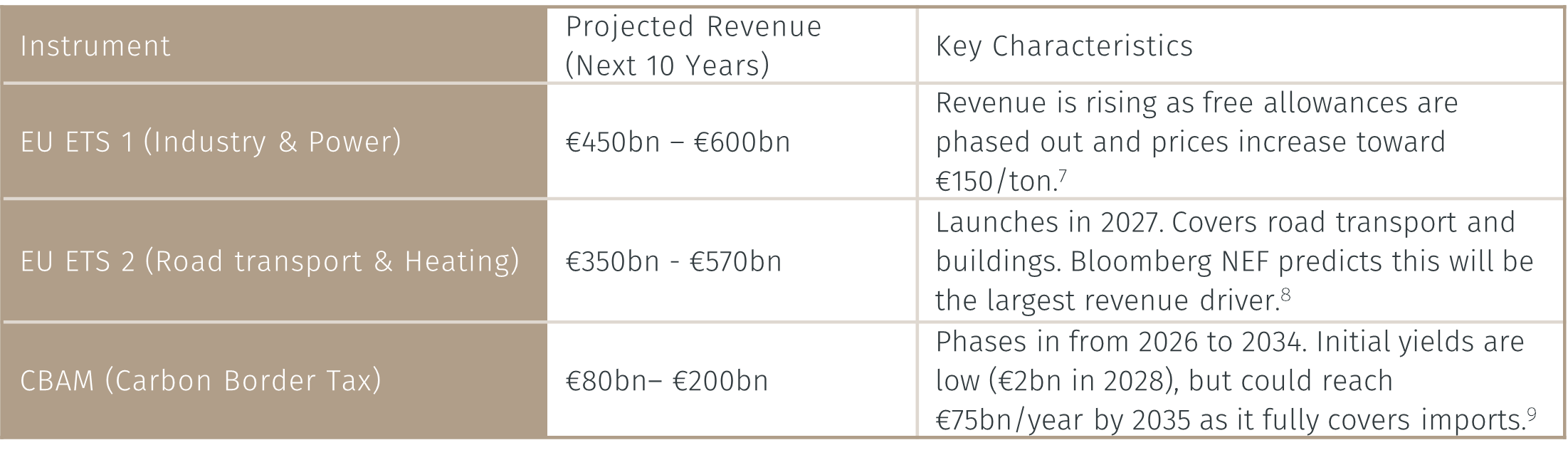

Over the next decade (2025–2035), the European Union is projected to generate between €1 trillion and €1.4 trillion (see table) of fiscal revenues from its carbon pricing mechanisms.