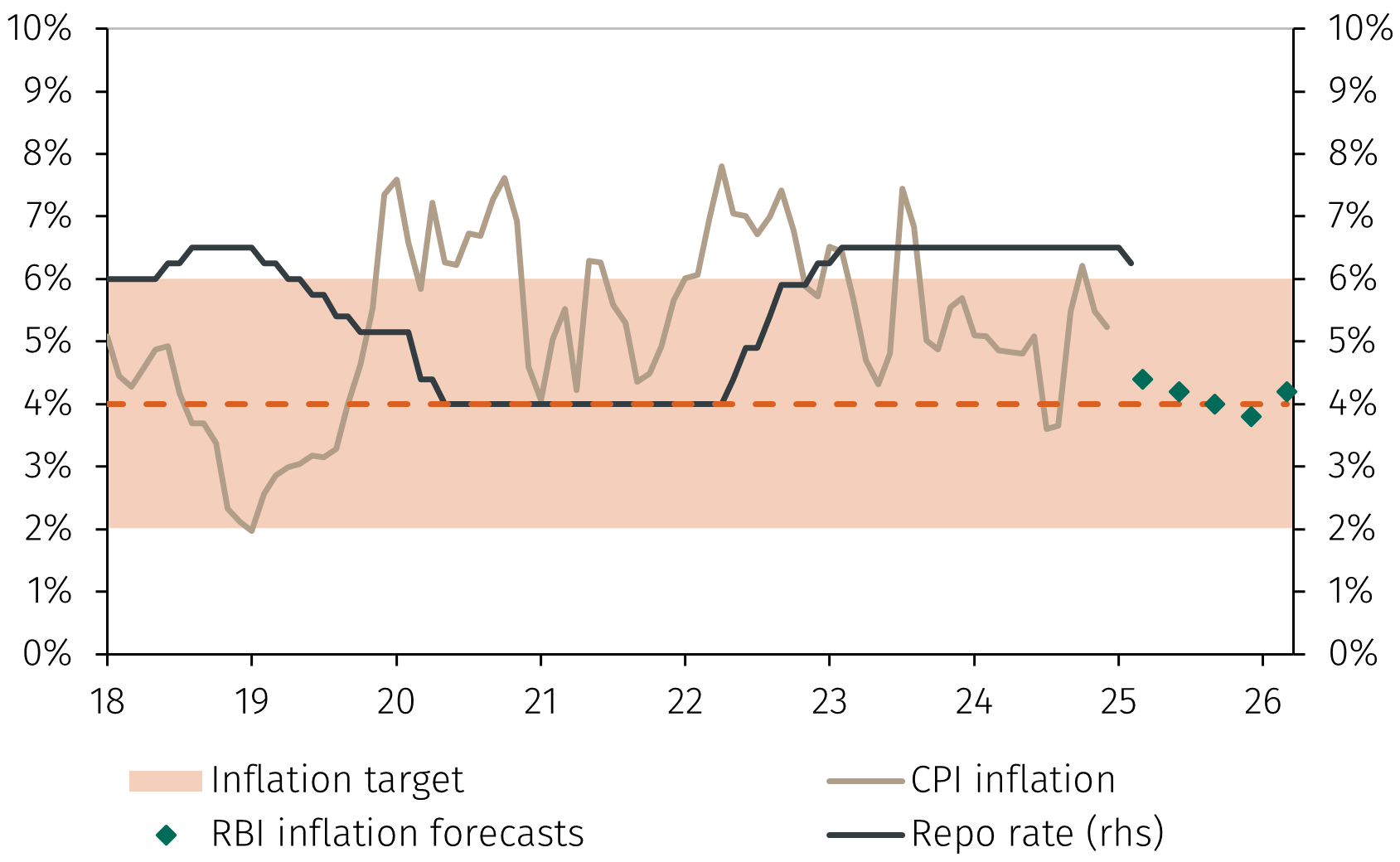

GDP growth surprised on the downside in Q2 FY 2024-25 at 5.4% year-on-year, below the 6.7% registered in Q2 FY 2024-25 and the RBI’s forecast of 7.0%. The slowdown in growth reflected weakness in the manufacturing sector.3 Although early corporate results for Q3 FY 2024-25 indicate a recovery in the manufacturing sector, and the MPC expects growth to rebound in the remaining two quarters of FY 2024-25, annual GDP growth is still forecast to slow to 6.4% from the 8.2% registered in FY 2023-24.4

The MPC outlined that the rationale for its monetary policy decision was the need to support growth, with lower inflation opening up the policy space to do so. While this would suggest that the MPC’s decision represents the start of a significant rate cutting cycle, there are other factors that make us cautious about drawing this conclusion.

The MPC unanimously voted to maintain a neutral stance on monetary policy rather than shifting to an accommodative stance.5 Its Monetary Policy Statement noted that “the strong dollar, inter alia, continues to strain emerging market currencies and enhance volatility in financial markets”.

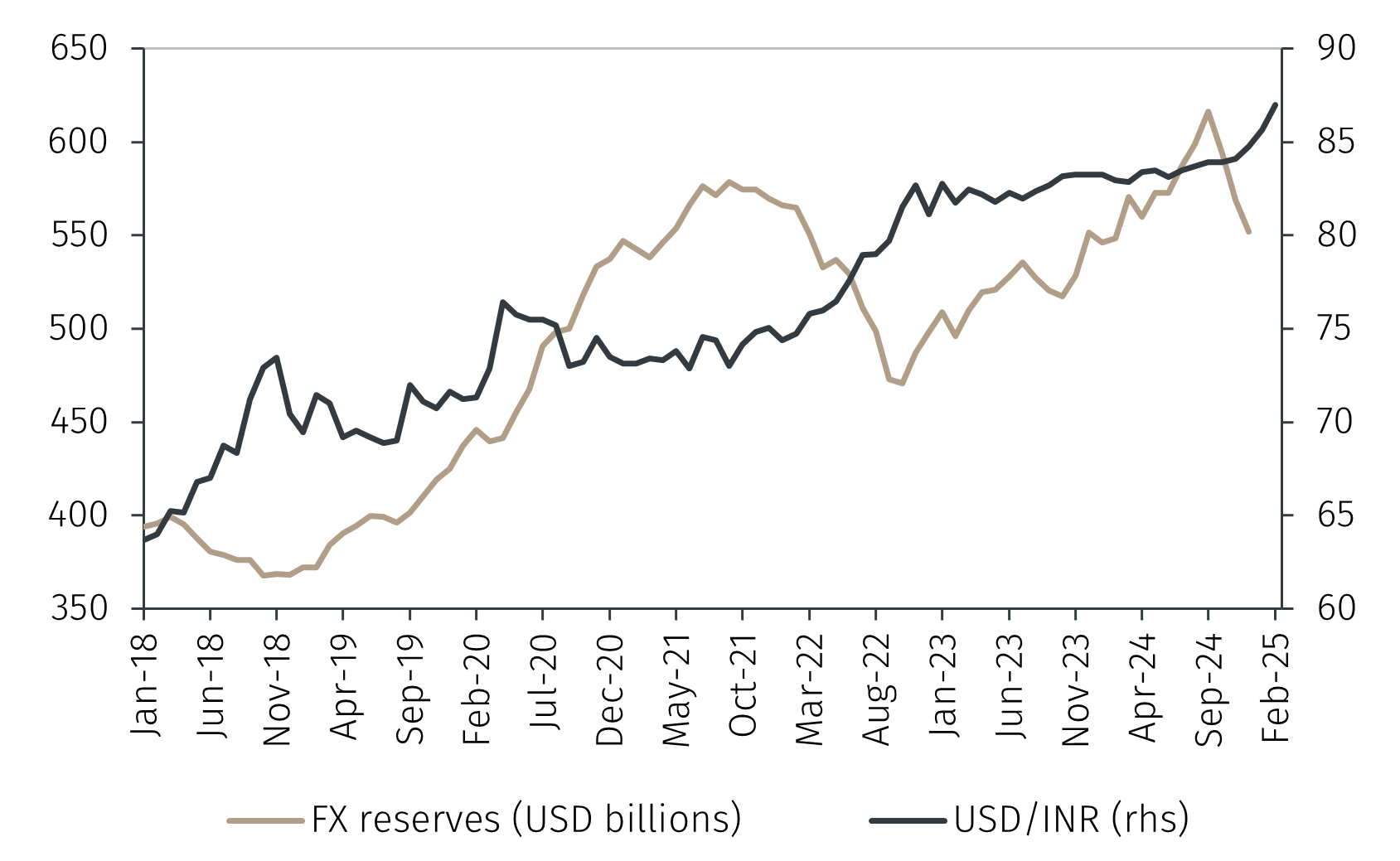

The Indian rupee has depreciated against the US dollar by 1.4% year-to-date, 3.2% since the US election and 4.1% since the start of FY 2024-25. This compares to a decline of 1.4% in the whole of FY 2023-24.6

The speed of the decline since the US election can be, at least partially, explained by the strength of the US dollar amid expectations surrounding Trump policies. Nonetheless, the RBI has sought to intervene by utilising its foreign exchange (FX) reserves, which have declined by around USD 41.8 billion since October 2024 (see Chart 2).7