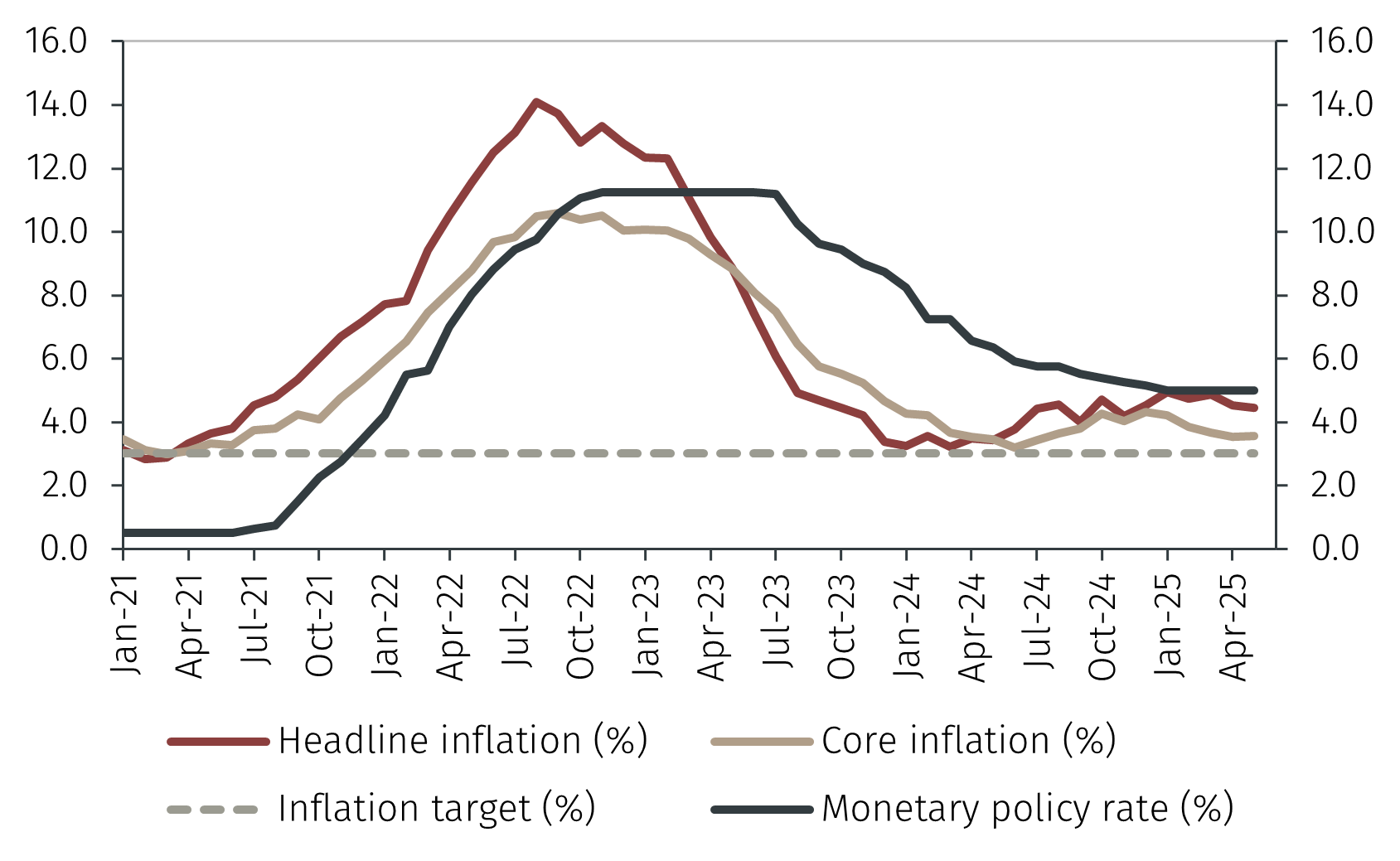

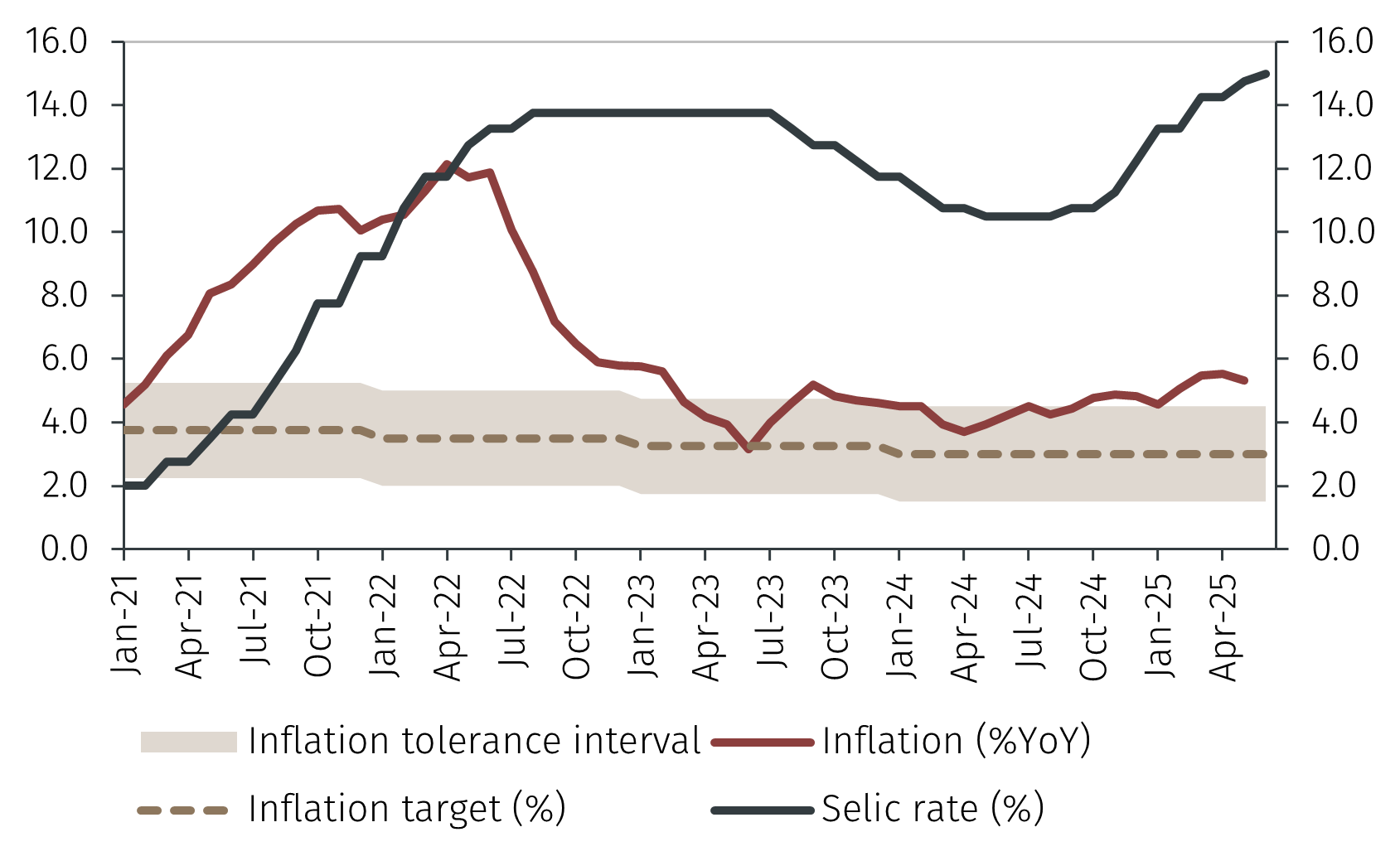

The Banco Central do Brasil's (BCB) Monetary Policy Committee (Copom) raised the Selic rate by 25 basis points to 15.00%, judging that a restrictive monetary policy is necessary to anchor inflation expectations and to return inflation to target. Copom assessed that economic conditions remain characterised by de-anchored inflation expectations, high inflation projections, resilient domestic economic activity and pressure in the labour market. Additionally, international conditions are seen as highly uncertain, particularly due to US trade and fiscal policy and geopolitical tensions.

Copom also believes that risks to the inflation outlook, both upward and downward, remain elevated. As a result, it intends to pause further increases to the Selic rate to assess the cumulative effects of past tightening but remains prepared to resume raising interest rates if inflation does not converge as expected.

At its June meeting, the Central Bank of Chile (CBC) decided to leave interest rates unchanged at 5%, citing a balance of risks to both domestic and external conditions. In its view, global uncertainty remains high, driven by escalating trade tensions and the conflict in the Middle East. However, the CBC noted that the potential impact of these on the Chilean economy are low.