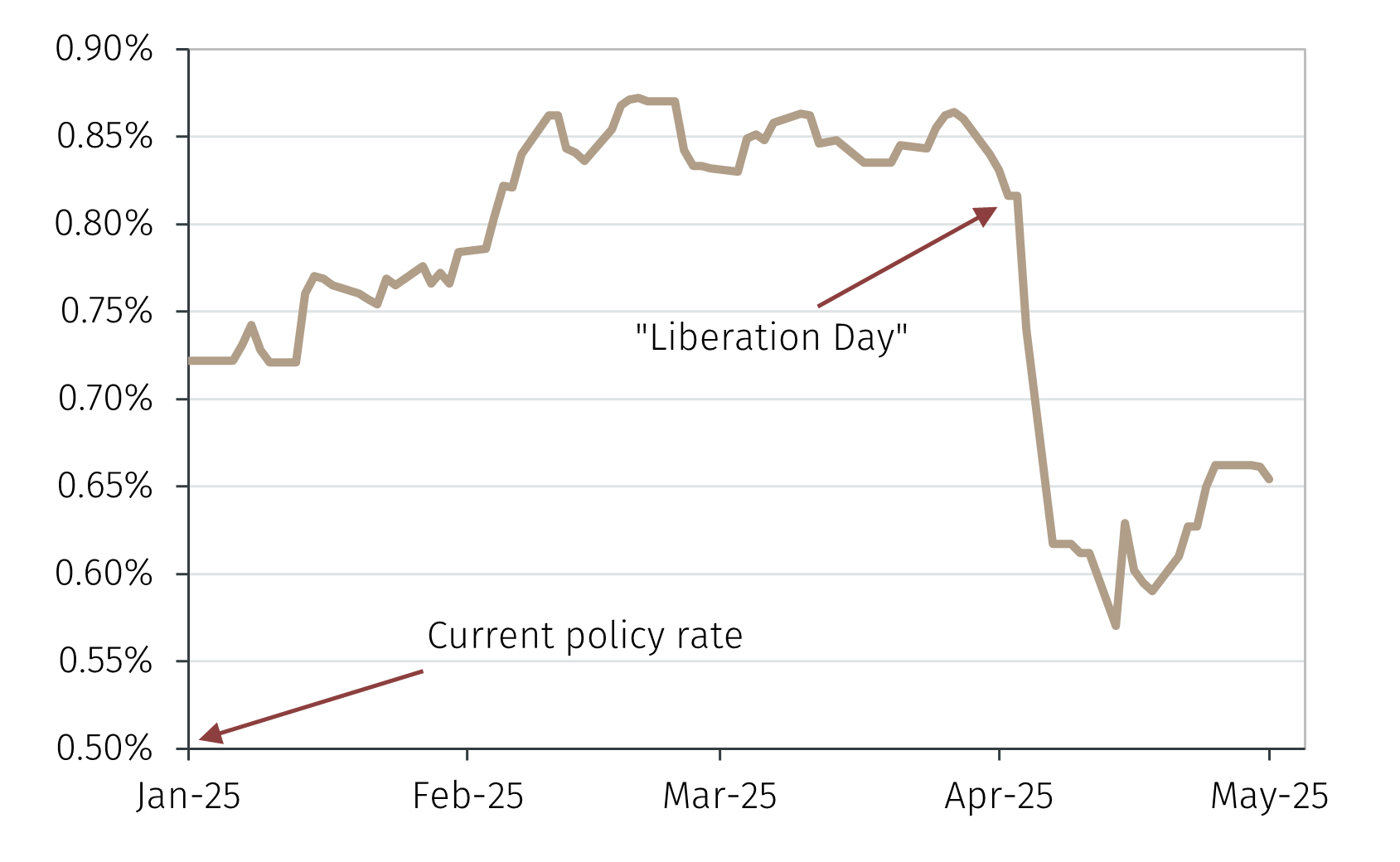

At its meeting in May, the BoJ Policy Board voted unanimously to leave the policy rate unchanged at 0.5%. The BoJ has been gradually raising the policy rate since March 2024, when it exited its Negative Interest Rate policy. The tone of each meeting since then has implied a bias to continue to tighten policy, with hawkish comments from Governor Ueda, forecasts of inflation above target and GDP growth above potential.1 Elevated uncertainty due to the Trump administration’s trade policy resulted in less hawkish rhetoric from the BoJ at its May meeting.

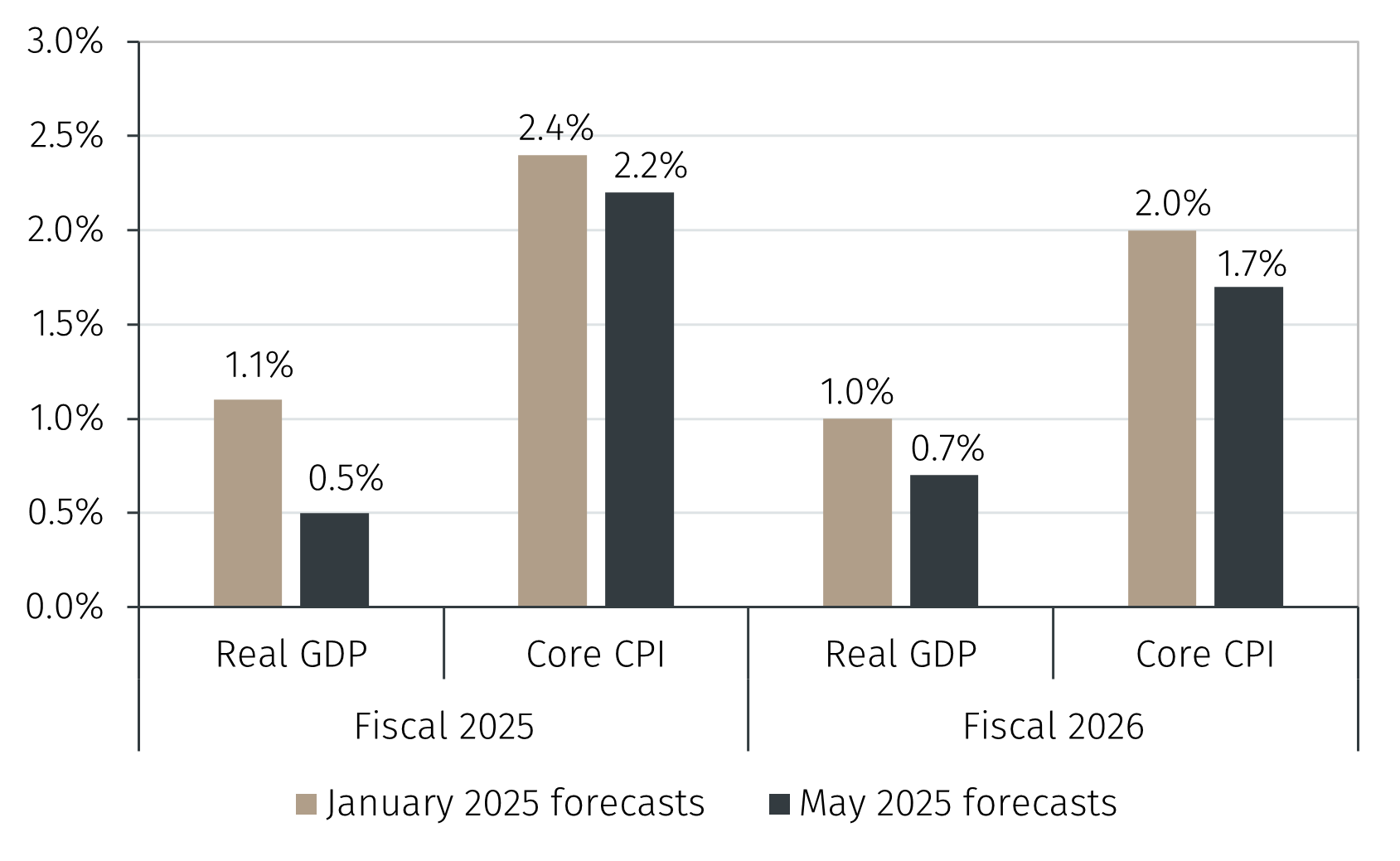

The BoJ’s updated ‘Outlook for Economic Activity and Prices’ saw downward revisions to Policy Board members’ forecasts for average annual real gross domestic product (GDP) growth and core consumer price index (CPI) inflation (see Chart 1).2 In addition, risks were viewed as being skewed to the downside.