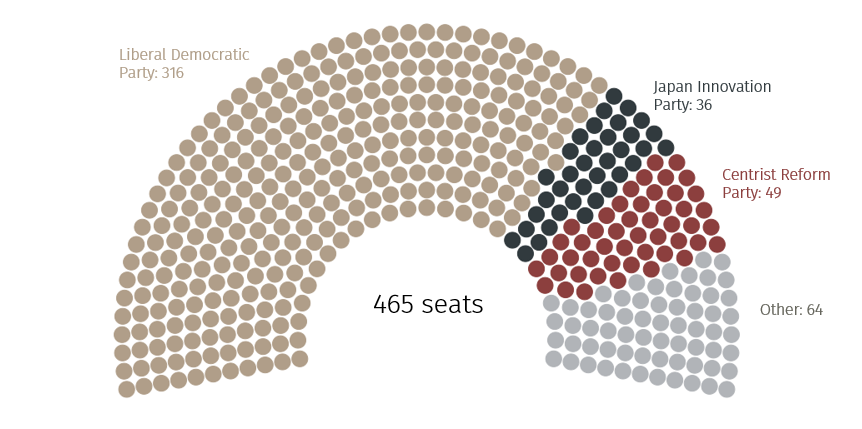

The Liberal Democratic Party won a large majority in Japan’s general election on 08 February, gaining over two-thirds of the lower house (see Chart 1). The seat count is the highest of any individual party in Japan since World War II and the 118 seat gain is among the largest in Japanese election history, making it an extraordinary result for Prime Minister Sanae Takaichi.

No need for negative SNB rates

Investment Insights • Macro

2 min read

Takaichi wins big in Japan’s election

Sanae Takaichi’s Liberal Democratic Party won a supermajority in Japan’s general election on 08 February. In this Macro Flash Note, Economist Sam Jochim provides an update on the implications for policy and markets.

Chart 1. Japan’s lower house composition

Source: NHK. Data as at 09 February 2026.

A vote for Takaichi, rather than the party

As discussed in a previous note, Takaichi took a gamble in calling the election and, clearly, it has paid off.1 The implication is that the LDP no longer needs to negotiate with smaller or opposition parties to pass legislation, and it can also overrule vetoes in the upper house of the National Diet, which it does not control.

Takaichi went into the election with extremely high approval ratings, despite her party being far from popular.2 The LDP’s election success was a reflection of the Prime Minister’s ability to frame the vote as a referendum on the individual running the country, rather than the party governing it. With such a strong mandate to rule, Takaichi has few excuses not to implement her election pledges.

Consumption tax concerns and the bond market

The most eye-catching pledge in the run up to the election was Takaichi’s promise to cut the consumption tax rate. This has historically been a politically sensitive subject in Japan. Even her mentor, former Prime Minister Shinzo Abe did not cut the consumption tax when he was implementing his fiscally stimulative policies that became a pillar of “Abenomics”.3

The bond market became concerned about government debt in Japan following this pledge (the importance of fiscal responsibility was highlighted in our 2026 Outlook).4 Yet Takaichi has stressed that the tax reduction would be temporary and that it would be implemented without additional issuance of government bonds. Whether this turns out to be the case will be key for markets in assessing how fiscally responsible Japan’s Prime Minister is in the absence of political checks.

Following the election, the bond market is now the main check for Takaichi. She will be keen to avoid having a “Liz Truss moment” and having promised a “responsible yet aggressive fiscal policy”, the onus will be on her to place extra emphasis on the “responsible” element on this mantra.5,6 The key question is therefore whether the supermajority emboldens Takaichi to implement a more expansive fiscal policy or has the opposite effect since she no longer needs to negotiate with smaller parties to pass legislation. At this stage, it is too early to know the answer to this question.

Market response and the road ahead

Market reaction to the election result has been mixed. Japanese equities have rallied, spurred on by stronger growth expectations, with the Nikkei 225 index rising 3.89%.7 Japanese government bonds are little changed as markets await clearer signals on the extent of the fiscal policy expansion and where the funding will come from. The Japanese yen initially depreciated against the US dollar before reversing that trend after authorities reiterated warnings about yen volatility, sparking anticipation of currency market intervention by Japan’s Ministry of Finance.8 At the time of writing, the yen has appreciated by around 1.0% against the US dollar.9

In summary, the LDP’s landslide election victory has given Prime Minister Takaichi a clear mandate to govern and to deliver on her election pledge for a more expansive fiscal policy. While there are very few remaining political checks in place, the bond market has become the key check for preventing irresponsible fiscal policy in Japan. However, initial market reaction suggests the bond market is yet to make up its mind and will await further signals before judging Takaichi’s fiscal policy. Japan’s Prime Minister will need to tread carefully to avoid a “Liz Truss moment” of her own.

1 See previous Macro Flash Note, ‘Takaichi’s gambit’

2 The Takaichi cabinet’s approval rating in December 2025 was 75% according to a Nikkei/TV Tokyo survey. This is the highest approval rating since Abe in 2013. The same survey showed the LDP’s approval rating was below 40%.

3 https://japan.kantei.go.jp/letters/message/abenomics/TheThreeArrowsOfAbenomics_EN.pdf

4 https://www.efginternational.com/uk/insights/outlook-2026.html

5 “Liz Truss moment” refers to the UK mini-budget in 2022 – when an unfunded reduction in taxation, which had not been assessed by the independent Office for Budget Responsibility was announced and led to a sharp fall in sterling and the gilt market.

6 https://www.bbc.co.uk/news/articles/cjd9k852zdjo

7 Nikkei performance calculated in local currency terms as at close on 09 February 2026.

8 https://www.asahi.com/ajw/articles/16341387#:~:text=Japan%27s%20top%20currency%20diplomat%20Atsushi,to%20a%20historic%20election%20win

9 Yen appreciation since midnight on the previous day taken from LSEG Data & Analytics at 14:43 GMT on 09 February 2026.