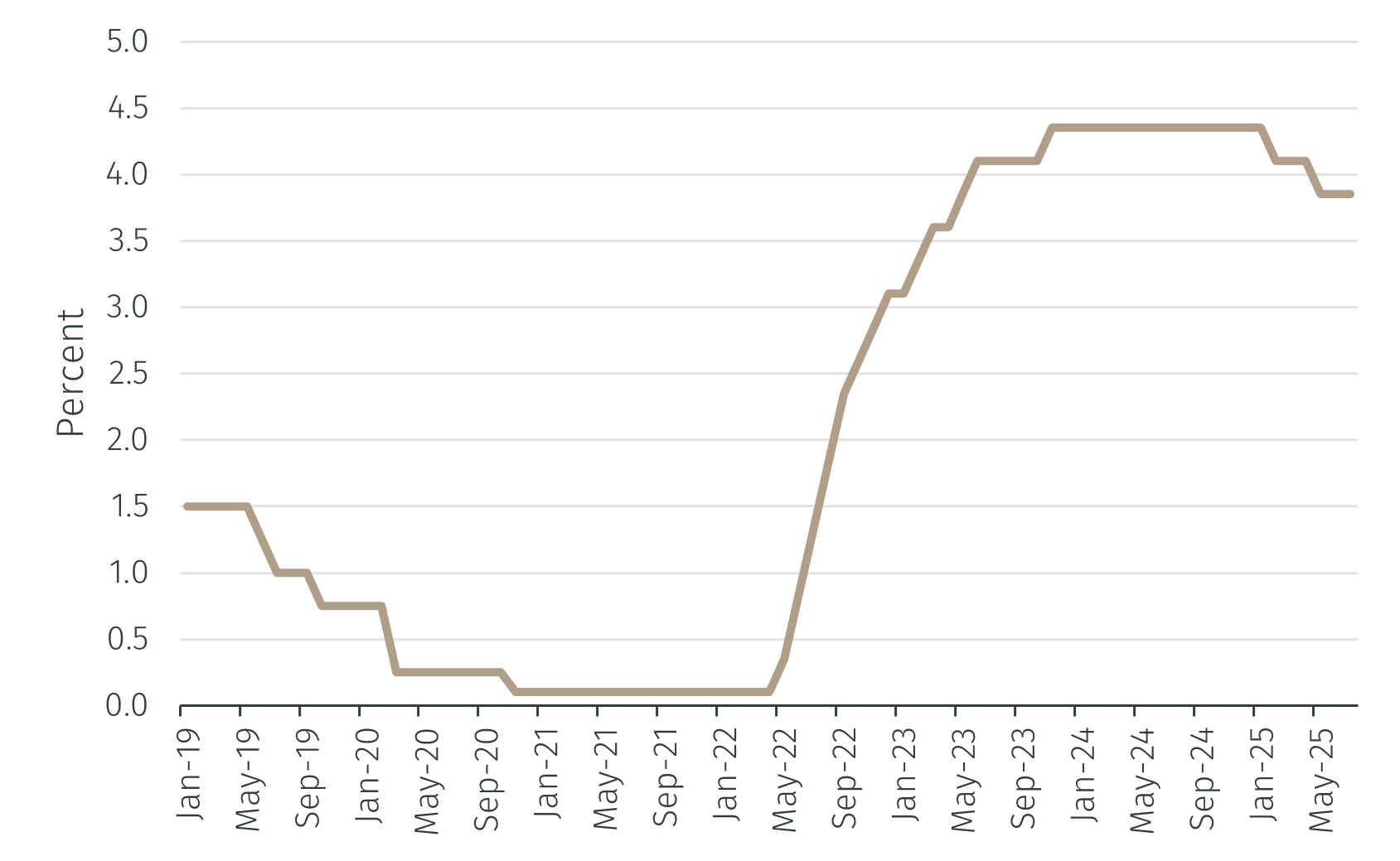

At its July meeting, the Reserve Bank of Australia (RBA) surprised financial markets by leaving interest rates unchanged. This decision has turned attention to the next meeting of the Monetary Policy Board, scheduled for 11–12 August.

The pattern of inflation and monetary policy in Australia has broadly mirrored that in other advanced economies. Inflation pressures eased in the early months of the pandemic in 2020. From 2021, inflation began to rise, peaking in late 2022, and has since declined. In response, many central banks, including the RBA, have turned cautiously from tightening to easing their policy stance.

Australia’s headline consumer price index (CPI) inflation peaked at 7.8% year-over-year (YoY) in the last quarter of 2022 and fell to 2.1% YoY in the second quarter of 2025. More importantly, the quarterly trimmed mean inflation rate, the RBA’s preferred measure of price pressures, dropped from 6.8% YoY to 2.7% YoY over the same period. Monthly data tell a similar story, with annual inflation falling from 8.4% YoY in December 2022 to 1.9% YoY in June 2025.