The Reserve Bank of Australia (RBA) enters its November meeting with a more complex policy environment than earlier in the year. The cash rate has been reduced by 80 basis points to 3.6% since February. While inflation has declined markedly from its 2022 peak, the remaining disinflation is proving slower than expected. And forward-looking indicators now show a clearer softening in labour demand.

Inflation: progress, but not yet complete

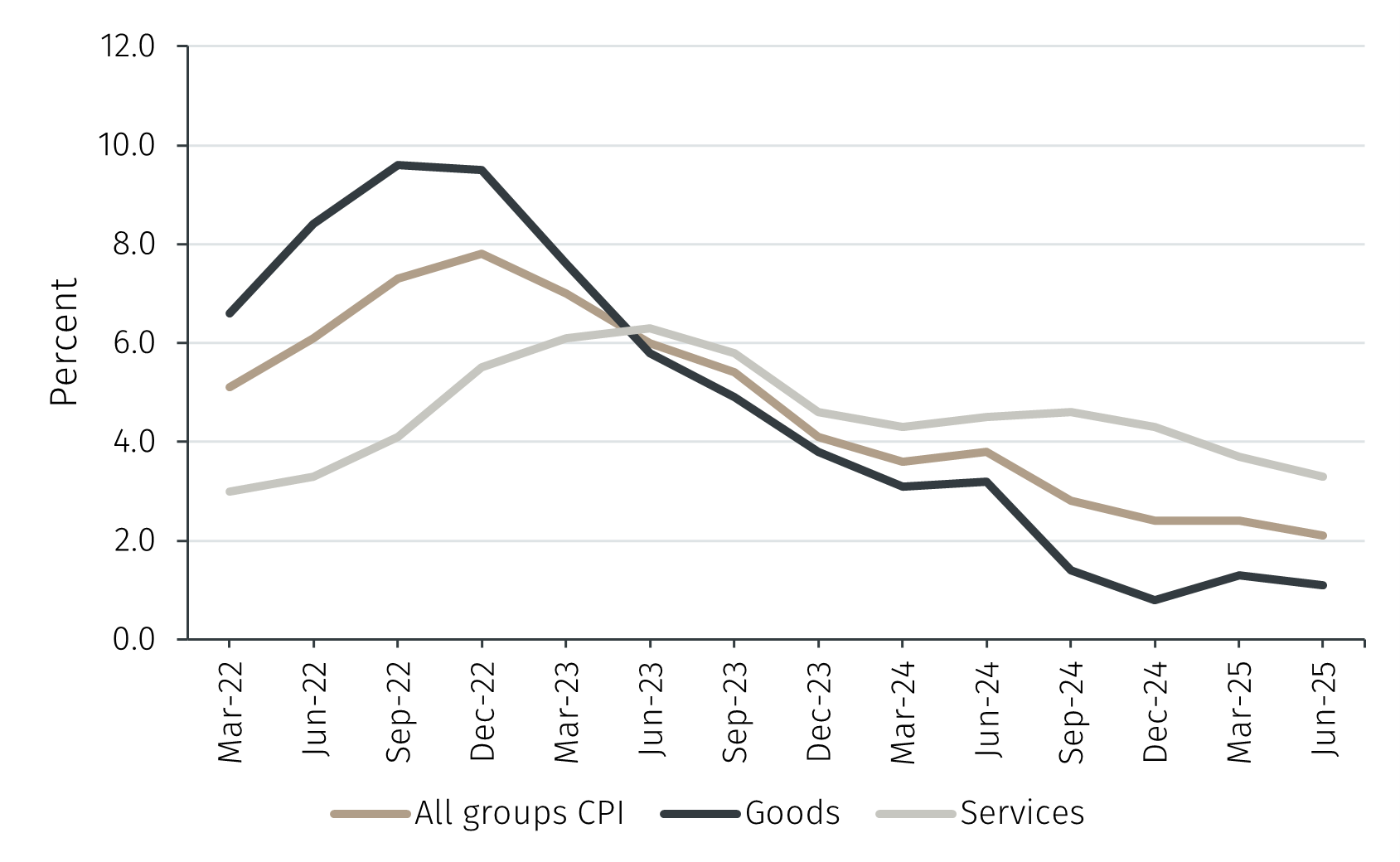

Goods price inflation has eased decisively, reflecting the normalisation of supply chains and weaker tradables inflation. Services inflation, by contrast, has remained relatively sticky. This matters because services prices are less sensitive to global conditions and more closely tied to domestic wage growth and productivity. When productivity is weak, as it has been in Australia, wage growth tends to feed through more directly into prices.