The release of the February data on the personal consumption expenditures (PCE) deflator provided little reassurance that price pressures in the US are meaningfully subsiding. While headline inflation was steady and in line with expectations, core and supercore measures of inflation came in slightly firmer, pointing to persistent price pressures, especially in services.

PCE inflation remains stubborn

Investment Insights • Macro

2 min read

PCE inflation remains stubborn

In this Macro Flash Note, Chief Economist Stefan Gerlach looks at the latest US inflation data and what it could mean for monetary policy.

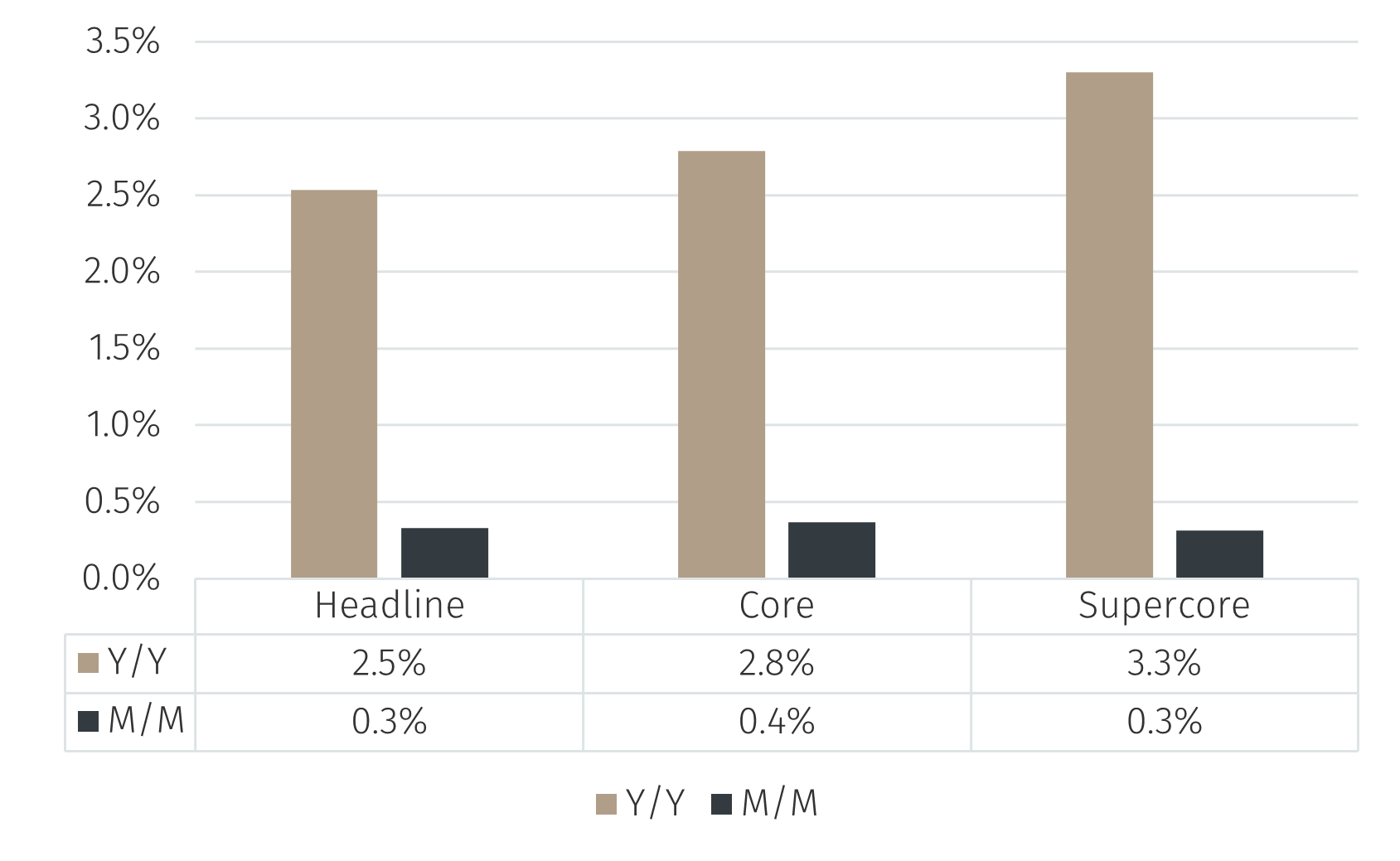

Chart 1. PCE Inflation

Source: Bureau of Labor Statistics. Data as at 28 March 2025.

The headline PCE price index rose 0.3% month-on-month in February, identical to January. On a year-over-year basis, it increased by 2.5%, also unchanged from January. These figures were in line with both the Fed’s projections and market forecasts.

Core PCE inflation—inflation excluding volatile food and energy prices—was less benign. It rose by 0.4% in February, a little higher than the 0.3% in January. On a year-over-year basis, core inflation rose to 2.8%, slightly above the 2.7% reported in January and above the 2.7% expected by markets.

Supercore inflation, which excludes housing and energy services, increased 0.3% on the month as in January. Year-on-year it was 3.3%, up from 3.1% in January. This measure continues to indicate persistent pressures in the service sector.

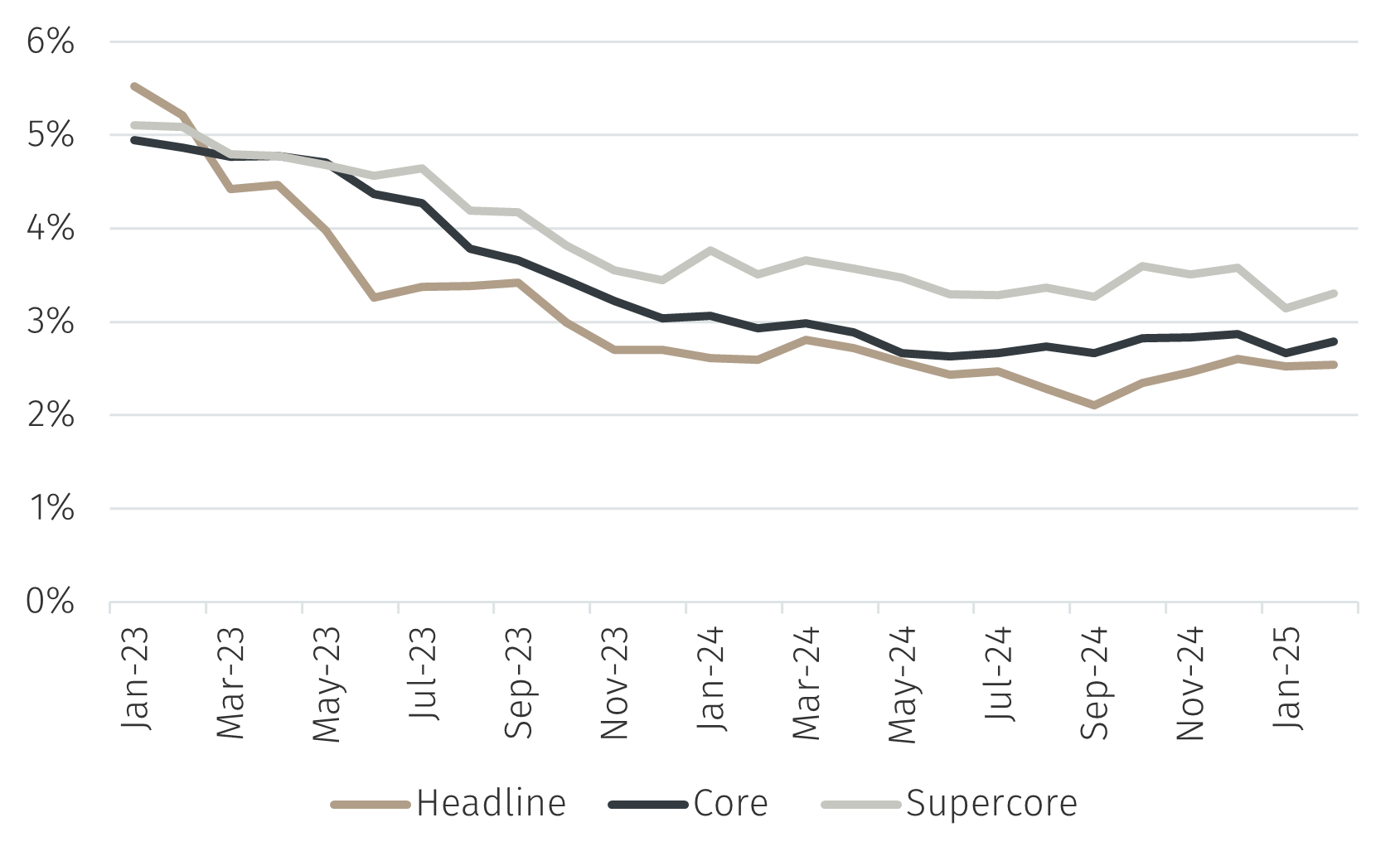

Chart 2. Inflation over 12 months

Source: Bureau of Labor Statistics. Data as at 28 March 2025.

Assessment and Fed Implications

The data suggest the disinflation process is continuing but slowing. While headline inflation is stable and broadly on track, the persistence in core and supercore measures indicates that underlying inflationary pressures—particularly in services—remain elevated. The 0.4% monthly rise in the core PCE measure, the highest since March 2024, shows that progress toward the 2% target is likely to be gradual.

The Federal Reserve finds itself caught between two opposing forces. This latest inflation report supports a cautious policy stance. And with tariffs reemerging as a potential inflationary force, the Federal Open Market Committee has solid grounds to remain patient and wait for clearer evidence that inflation is on a sustained downward path before resuming an easing cycle.

At the same time, the recent deterioration in consumer sentiment suggests that rate cuts may soon be warranted – particularly if the newly announced tariffs begin to weigh on economic activity. Although tariffs will likely push prices higher in the short term, any resulting slowdown could exert significant downward pressure on inflation over the medium term, thereby justifying lower interest rates.