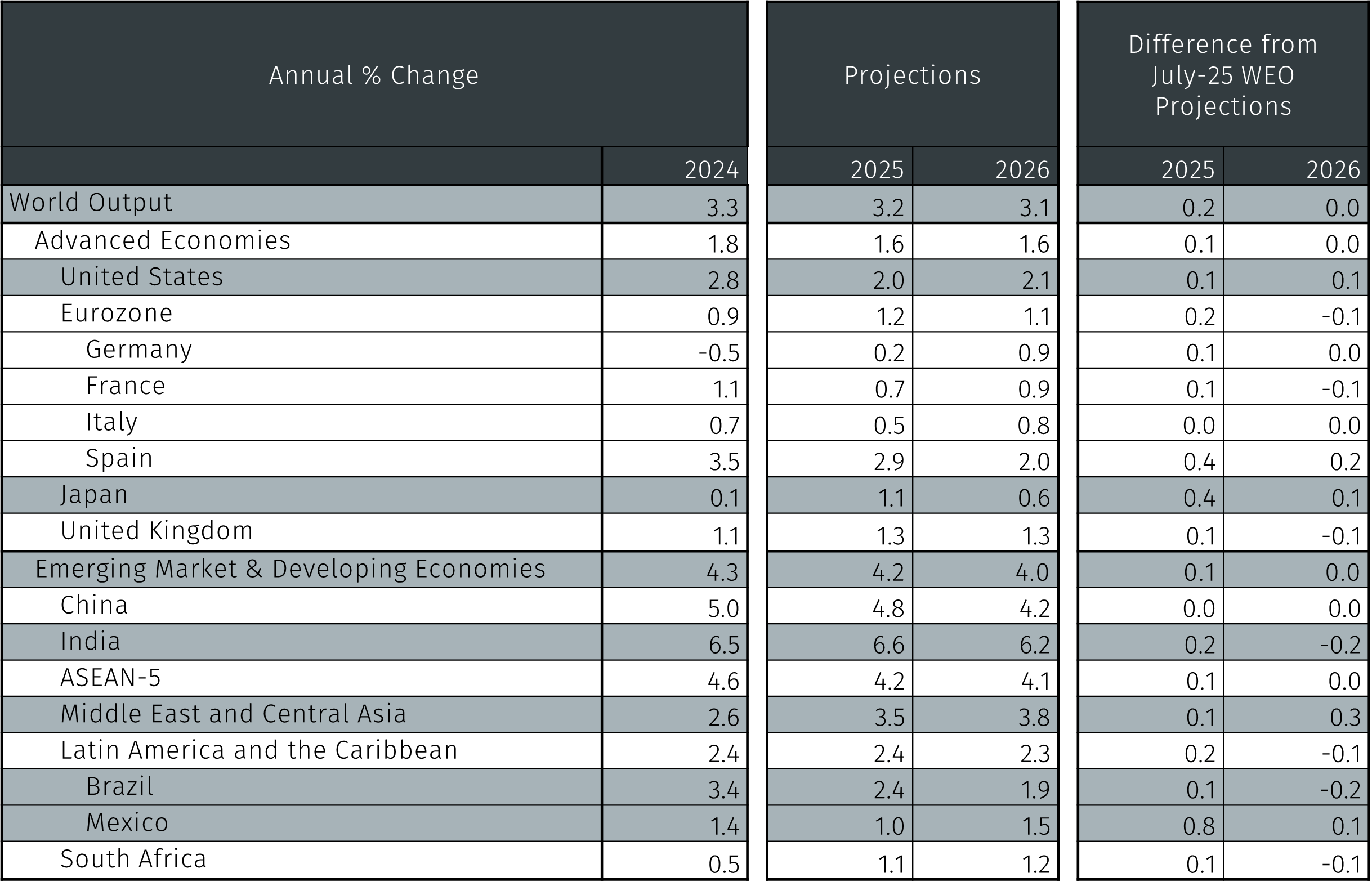

For advanced economies, the IMF expects GDP growth to reach 1.6% in 2025 and 2026. In the United States, growth is expected to slow from 2.8% in 2024 to 2.0% in 2025, before marginally accelerating to 2.1% in 2026. This reflects improvements in the outlook due to lower effective tariff rates, fiscal stimulus from the OBBBA, and easing financial conditions.2 In the eurozone, growth is projected to pick up modestly to 1.2% in 2025, but forecasts for 2026 were slightly downgraded to 1.1%.

In emerging market and developing economies (EM), the IMF expects growth to moderate from 4.3% in 2024 to 4.2% in 2025 and 4.0% in 2026, remaining nearly unchanged from the July WEO. Within EM, growth in China is projected at 4.8% in 2025, reflecting front-loading in trade and robust domestic consumption supported by fiscal expansion, which offset the headwinds from the trade uncertainty.

In Latin America and the Caribbean, the 2025 forecast was revised upward by 0.2 percentage points relative to the July WEO, driven by lower tariff rates and stronger-than-expected economic data, with Mexico's growth forecast for 2025 upgraded by 0.8 percentage points. Growth in the Middle East and Central Asia is projected to recover in 2025 and 2026, as the effects of oil production disruptions and regional conflicts abate.

Risks to the outlook

The IMF continues to view risks to the outlook as tilted to the downside, echoing themes of repricing of new technologies, shocks to labour supply, fiscal challenges, and pressures on central banks.

The IMF views the current “artificial intelligence boom” as similar to the dot-com boom of the late 1990s, with market optimism around transformative technology driving up stock valuations, spurring tech-focused investment, and supporting consumption through capital gains. The report argues that this trend could raise the neutral interest rate, and if demand pressures intensify further, it may necessitate tighter monetary policies to maintain economic and financial stability.

According to the report, shocks to labour supply caused by stricter immigration policies in advanced economies could hinder firms' investment and hiring decisions, particularly in sectors reliant on immigration to address skill shortages. This could create a negative supply-side shock, reducing the economy's potential output. Additionally, labour market tightness could drive up services and core inflation.

The IMF further notes that countries face mounting fiscal challenges due to lower growth prospects, higher real interest rates, elevated debt levels, and increased spending needs, such as on defence and national security. These pressures heighten vulnerability to external shocks.

Lastly, the report emphasises that central banks are facing growing pressures that risk undermining decades of “hard-won credibility” in policymaking. Maintaining trust in their ability to ensure price stability is crucial, as it allows inflation expectations to remain anchored against economic shocks.

While downside risks persist, the IMF notes that continued progress on trade agreements and subsequently, the lowering of tariffs, are creating opportunities to boost global output. Additionally, beyond its effects on investment, advancements in AI could improve productivity and support economic growth. Which as a result, could foster business dynamism by enabling high-productivity firms to reallocate resources efficiently, provided supportive policies are in place.

Conclusion

The global growth outlook remains little changed from the IMF’s previous projections, with only slight upward revisions for 2025 and 2026. While recent policy adjustments, such as tariff reductions, have provided some relief, uncertainty continues to weigh on investment and consumption. The IMF notes that the global economy is navigating a challenging landscape of heightened protectionism, fragmentation, and dim medium-term growth prospects. It stresses that policymakers must prioritise fiscal sustainability and institutional independence to address these challenges and restore confidence.