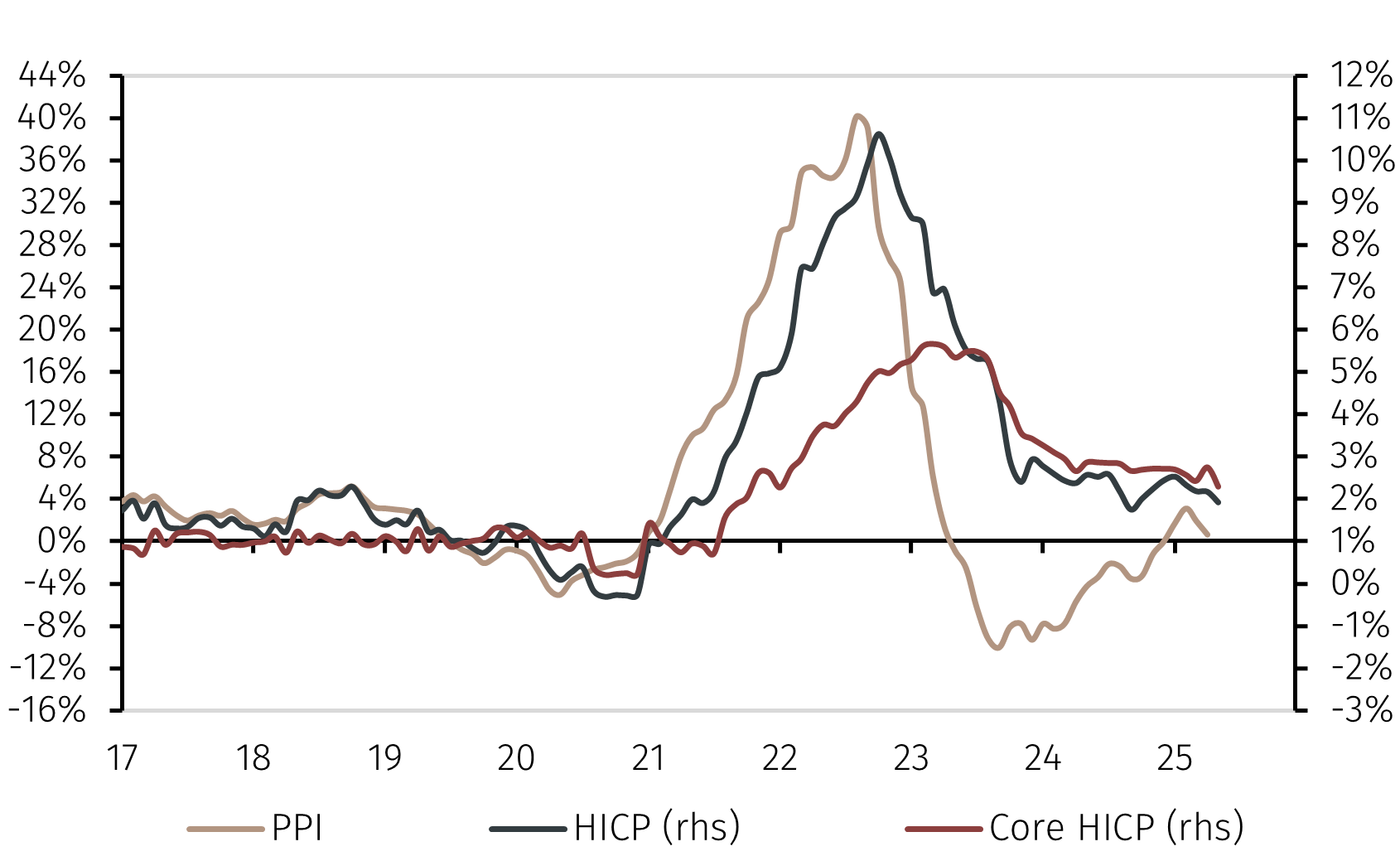

As widely expected, the ECB’s Governing Council (GC) decided to cut interest rates by 25 basis points at its 05 June meeting, bringing the deposit facility rate (DFR) to 2.00%. The move reflects the decline in May in headline inflation to 1.9% year-on-year (YoY) and core inflation, excluding energy and food, to 2.3% YoY, the lowest since late 2021 (see Chart 1).

What if Trump fires Chairman Powell?

Investment Insights • Macro

2 min read

Data dependency does not mean ECB rates have bottomed

On 05 June, the European Central Bank (ECB) cut interest rates by 25 basis points as expected. In contrast to the recent past, President Lagarde’s comments do not offer guidance on the central bank’s next moves. In this Macro Flash Note, Senior Economist GianLuigi Mandruzzato looks at the factors that could influence the ECB’s future monetary policy.

Chart 1. Eurozone producer price index (PPI) and harmonised index of consumer prices (HICP) inflation (YoY)

Source: LSEG Data & Analytics and EFGAM calculations. Data as at 05 June 2025.

However, President Lagarde’s comments on the new macroeconomic projections were more hawkish than markets expected. Despite the downward revision of the inflation and growth estimates for 2025 and 2026, Lagarde emphasised that in 2027 inflation is estimated to return to the 2% target.

Lagarde reiterated that the ECB does not commit to any specific path of interest rates and that the next decisions will be data dependent. The President’s words suggest that, in the absence of new shocks, the GC views the current level of interest rates as appropriate to achieve price stability in the medium term. In response, market expectations for the level of the DFR rose and now see it bottoming out at 1.75% in late 2025.

The ECB’s wait-and-see approach is appropriate given the high level of uncertainty on the economic outlook, starting with the outcome of the trade negotiations with the US. However, several factors point to downside risks to inflation that could shift the GC towards interest rate cuts that are larger than the markets price in.

The fall in the PPI suggests that downward pressures on consumer goods prices remain strong. If the relationship between PPI and HICP that prevailed before the pandemic were to re-stablish itself, it would not be surprising if eurozone inflation converged towards 1% YoY (see Chart 1).

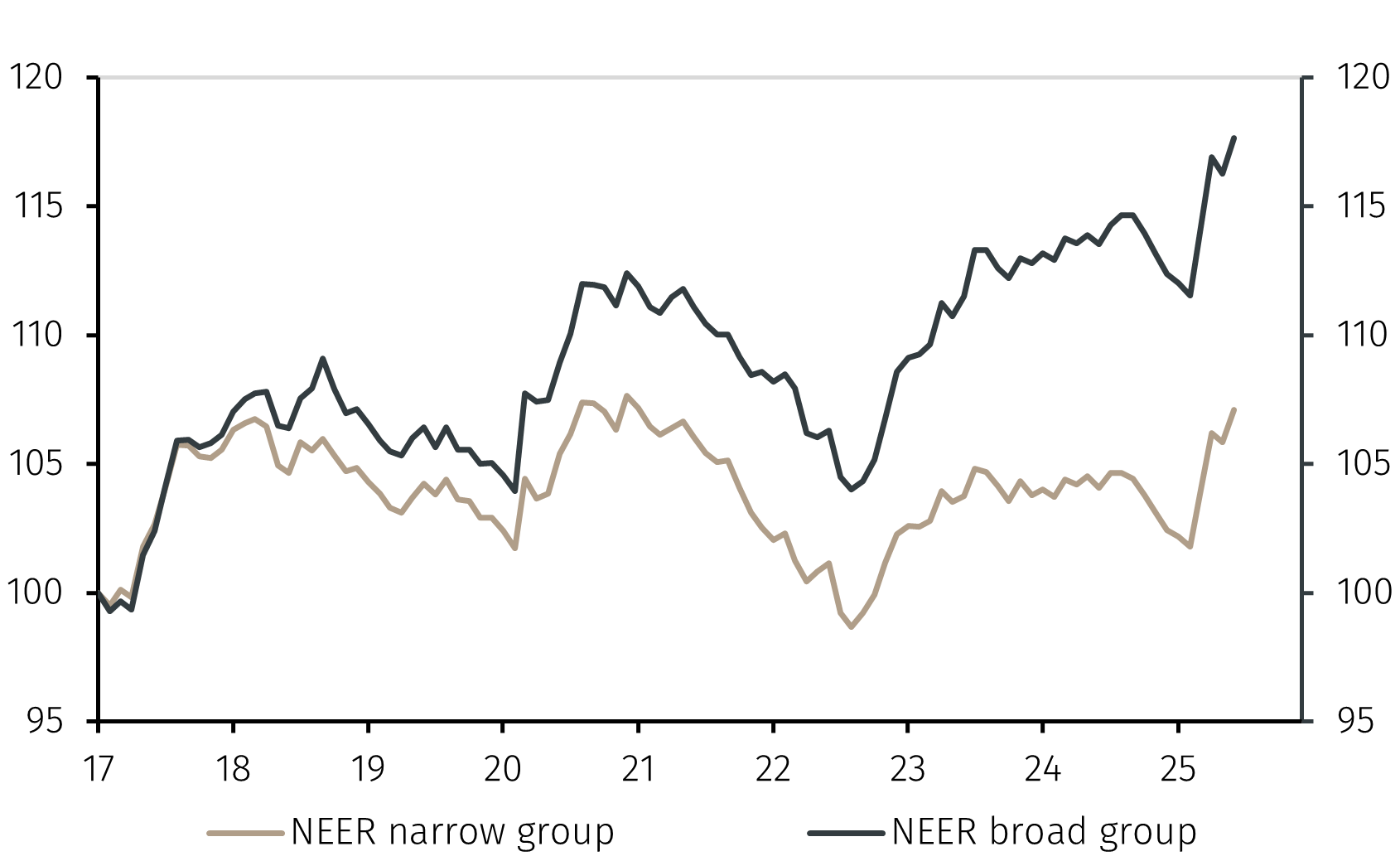

The rise of the euro since the beginning of the year will also help to reduce import prices, including those of energy goods, but it will only be fully reflected in consumer prices in the coming months (see Chart 2). If, as many commentators expect, the euro continues to strengthen, the impact on eurozone inflation will be even more pronounced.

Chart 2. Euro trade-weighted exchange rates (Jan 2017 = 100)

Source: LSEG Data & Analytics and EFGAM calculations. Data as at 05 June 2025.

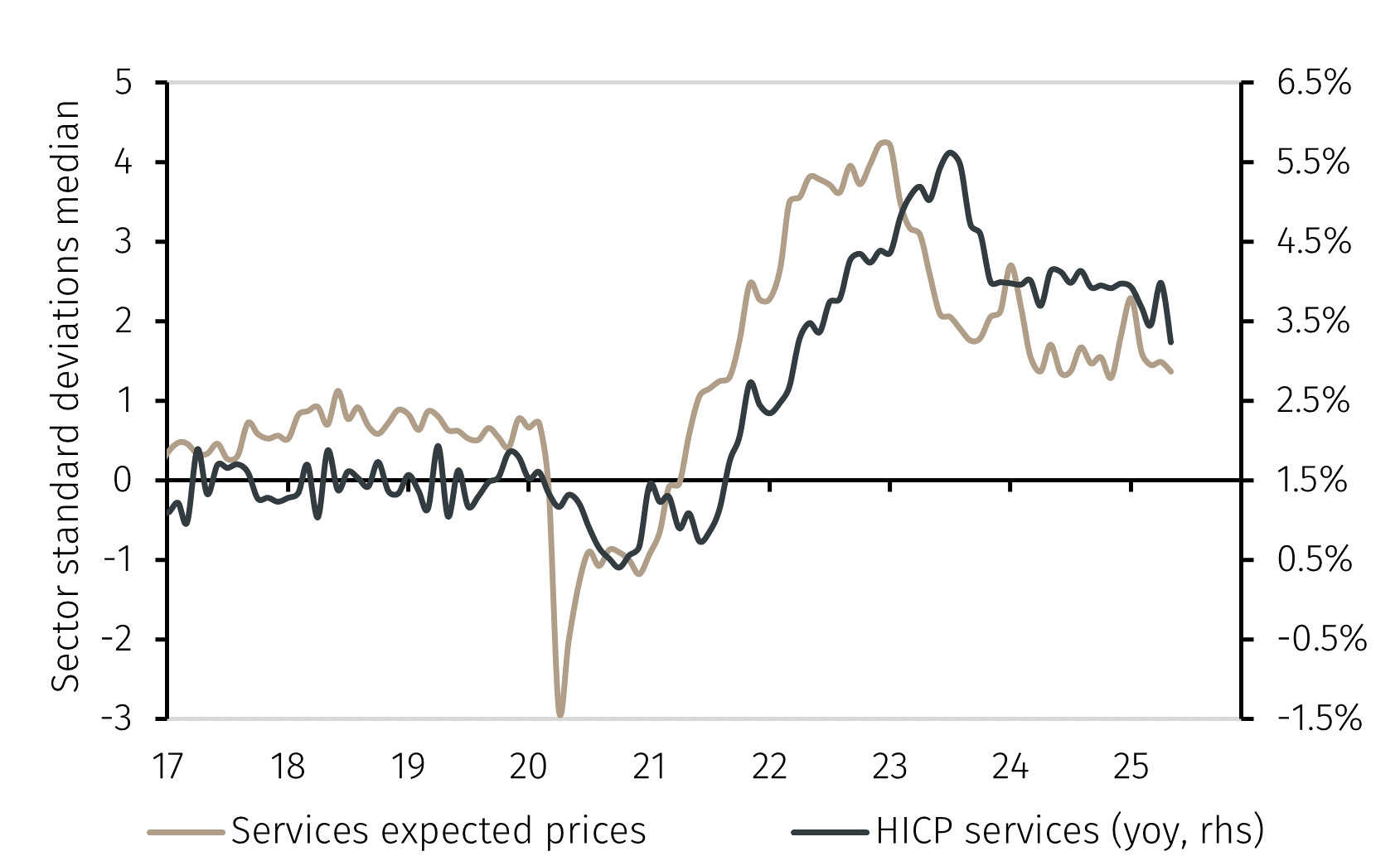

Furthermore, business surveys suggest that services sector inflation will decline further, adding to the downward pressure on core inflation (see Chart 3).

Chart 3. Services expected prices and HICP

Source: LSEG Data & Analytics and EFGAM calculations. Data as at 5 June 2025.

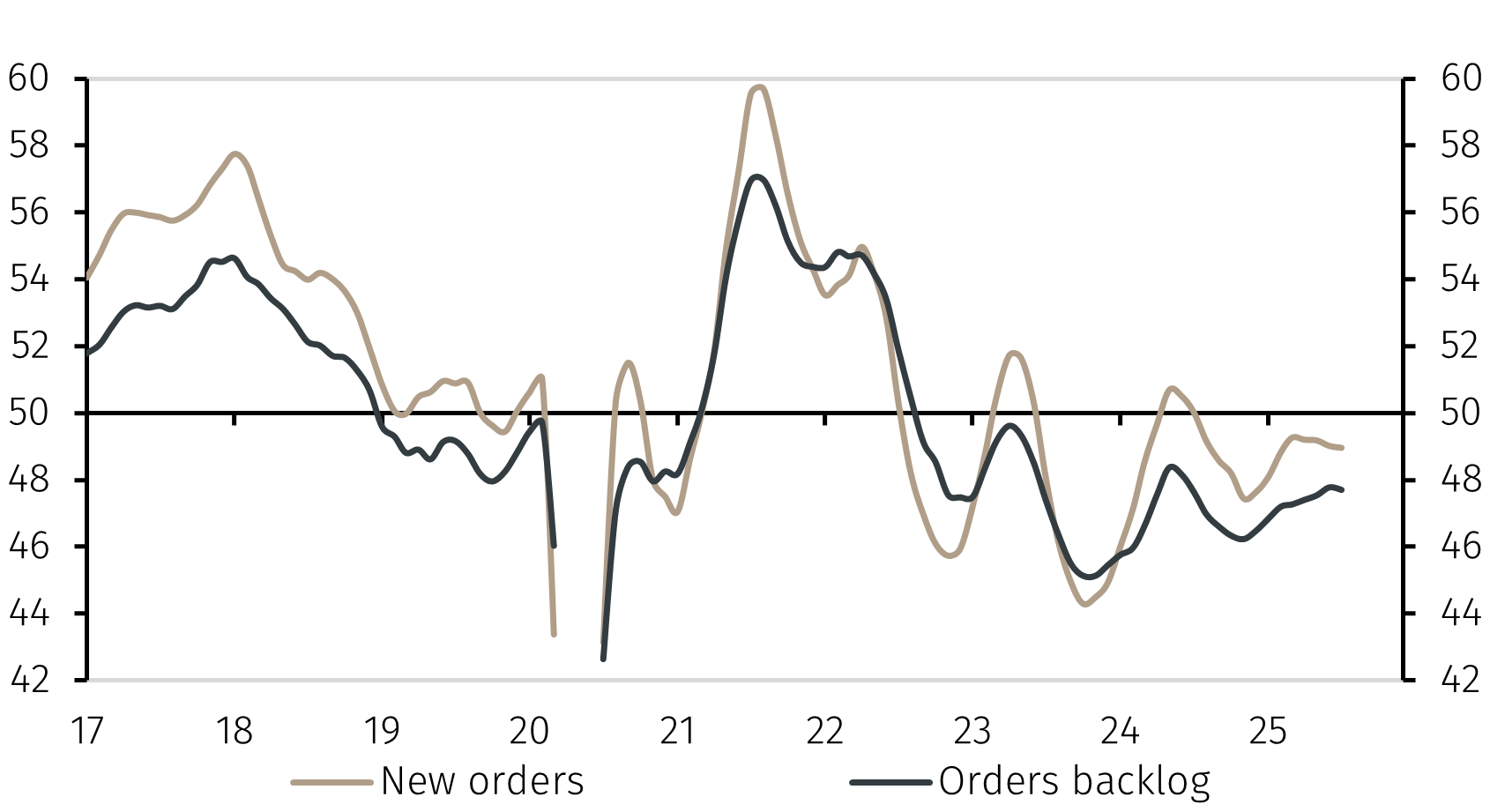

Finally, GDP growth looks set to remain weak in coming quarters. The purchasing managers’ index (PMI) orders components point to below-potential growth, extending a phase that has lasted since late 2022 and contributed to the decline in inflation (see Chart 4).

Chart 4. Eurozone composite PMI new and backlog orders

Source: LSEG Data & Analytics and EFGAM calculations. Data as at 05 June 2025.

In conclusion, it was sensible for the ECB to avoid giving forward guidance in the face of an uncertain outlook. Although markets interpreted this as a hawkish signal, its data-dependent approach leaves the door open to further rate cuts — perhaps larger than markets expect — should downside risks to inflation from falling producer prices, a strong euro, and weak GDP growth materialise.