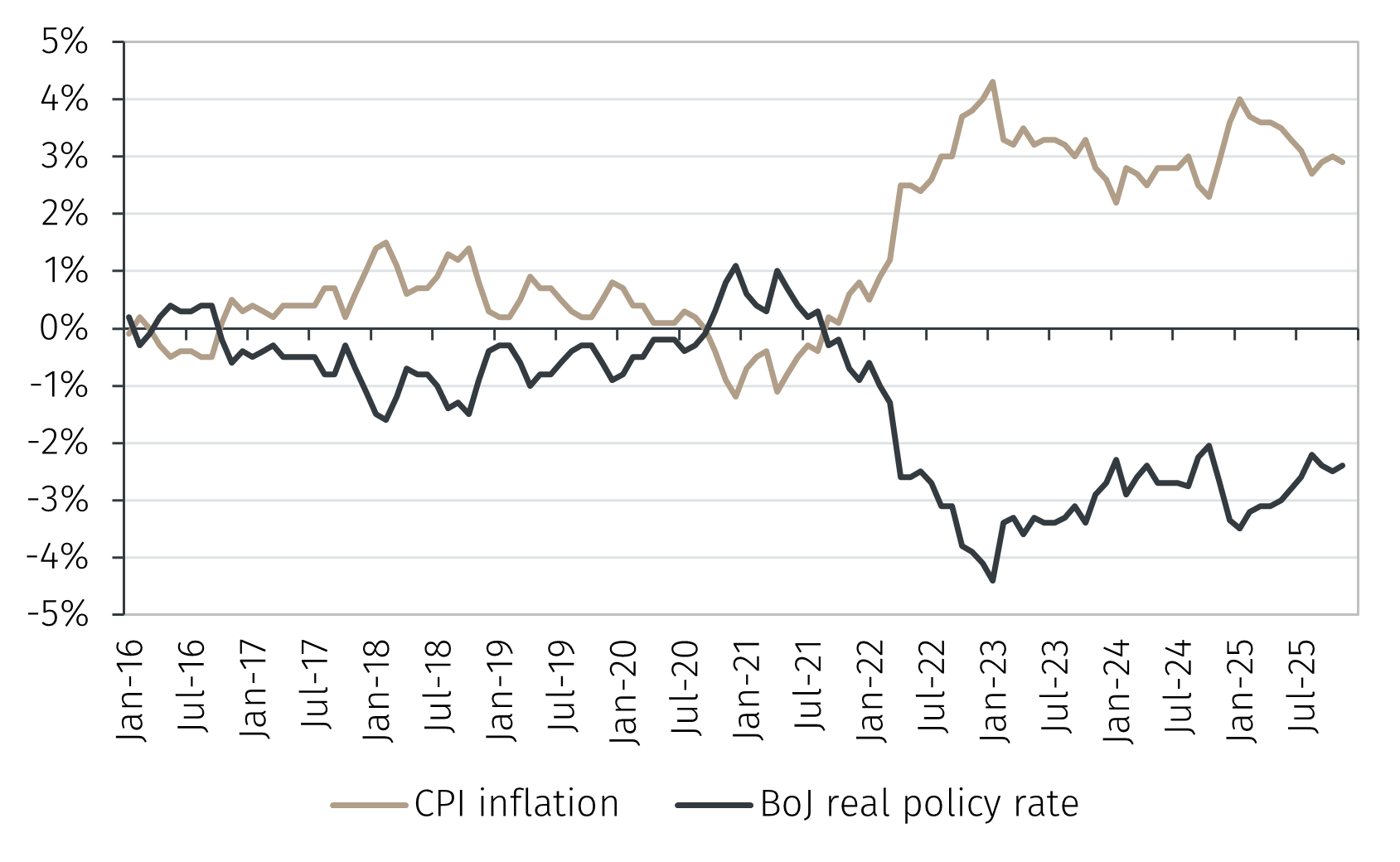

Even after the latest interest rate increase, the BoJ noted that real interest rates are expected to remain very low and that monetary policy remains accommodative. The decision in December can therefore be likened to the BoJ taking its foot off the accelerator rather than stepping on the brake.

With underlying inflation forecast to be at or above the 2% target over the BoJ’s entire forecast horizon, it is reasonable to expect further policy rate increases.2 The Bank of Japan has previously highlighted the importance of the spring wage negotiations, known as the Shunto, in realising this outlook. While the timing of the next rate hike is unclear, it is unlikely to come before there is more information available from the 2026 Shunto, making the June meeting the most likely date.

Determining the terminal rate

The key question at this point is what the terminal rate will be. The terminal rate is the peak interest rate the BoJ expects to reach in its monetary policy tightening cycle. Given the central bank forecasts inflation of 2% in fiscal year 2027, it is reasonable to expect the terminal rate to be consistent with the neutral rate. This is the interest rate which neither stimulates nor restricts the economy. The neutral rate must be estimated since it is unobservable, and the BoJ has estimated a range of 1.0-2.5%. This means that another rate hike would take the BoJ policy rate to the lower bound of its estimated neutral range.

However, given the BoJ noted real interest rates are “at significantly low levels” even after the latest rate increase, it is reasonable to expect rates to be increased by more than 25 basis points before the terminal rate is reached.3 Thus, a range of 1.25-1.75% appears more appropriate for the terminal rate. Taking an average pace of one rate hike every six months, this could be achieved either by the end of 2026 or the end of 2027.

Market reaction

The BoJ’s decision was well anticipated and the market reaction was relatively muted. At the time of writing, the Japanese yen has depreciated 1.1% against the US dollar, reversing the 1.0% increase it experienced against the dollar in the month leading up to the BoJ decision.

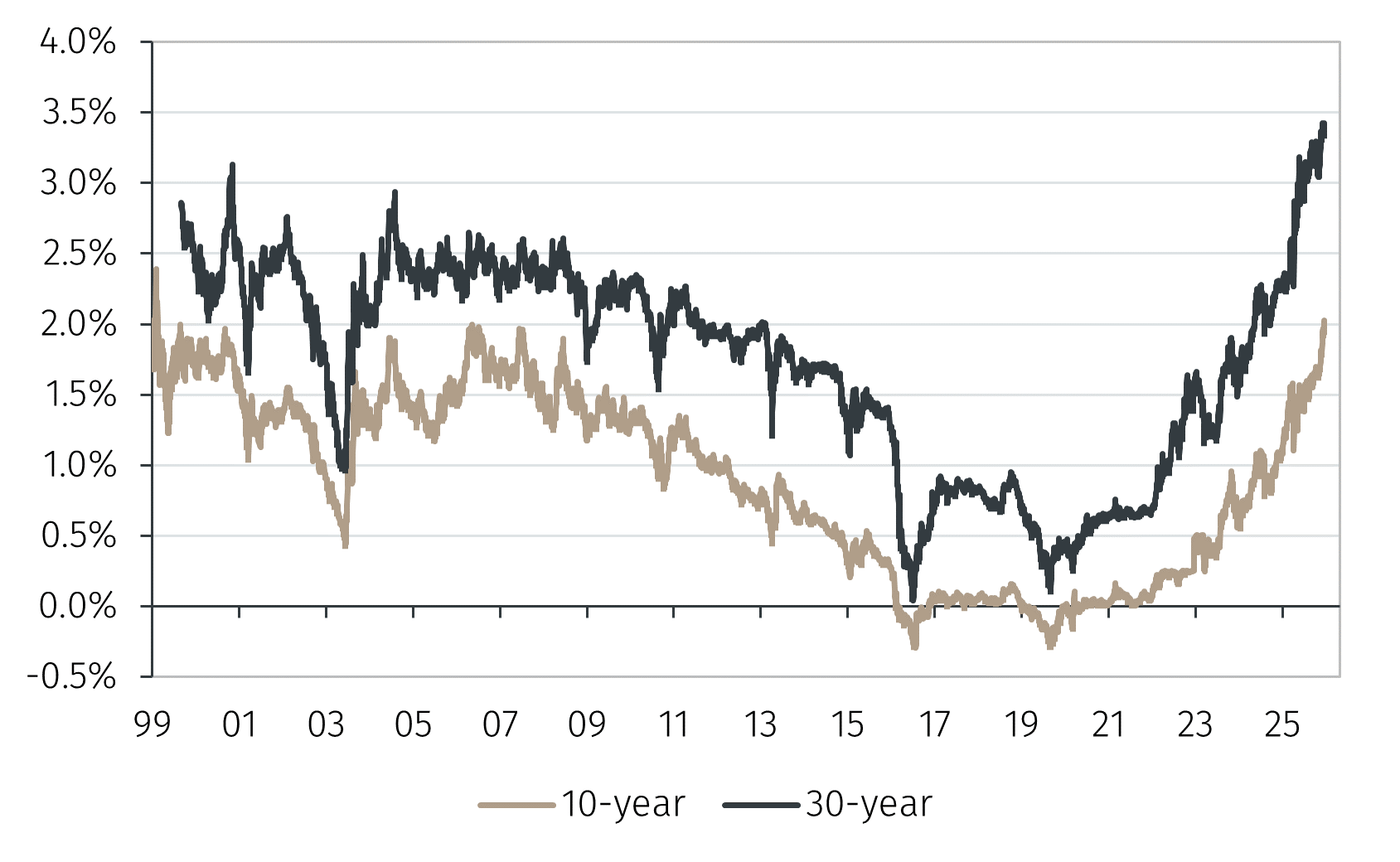

After the BoJ announcement, Japanese government bond (JGB) yields rose across the term structure. For the shorter maturity JGBs, this reflects a mixture of the higher policy rate and expectations of further interest rate increases. For the longer dated JGBs, the rise in bond yields also reflects the looser fiscal policy under Prime Minister Takaichi.4 Notably, the 10-year yield and the 30-year yield are at their highest level since 1999. (see Chart 2).5