Central bank independence

The BCB had gained independence from the Government by law in February 2021, under former Governor Roberto Campos Neto. This set the primary objective of price stability and granted technical, operational and financial independence to the BCB, aimed at separating monetary policy from political pressures.

That is why, when Gabriel Galipolo was announced as the next BCB Governor in August 2024, markets feared that an appointment of someone close to President Lula Da Silva would have hindered the central bank’s recently obtained independence. Lula had openly criticized former governor Campos Neto, accusing him of strangling economic growth and interfering with the government’s agenda by keeping interest rates too high.1 Therefore, markets were concerned that Lula had appointed seven out of the nine Copom members, including the governor, with the aim of influencing policy decisions.

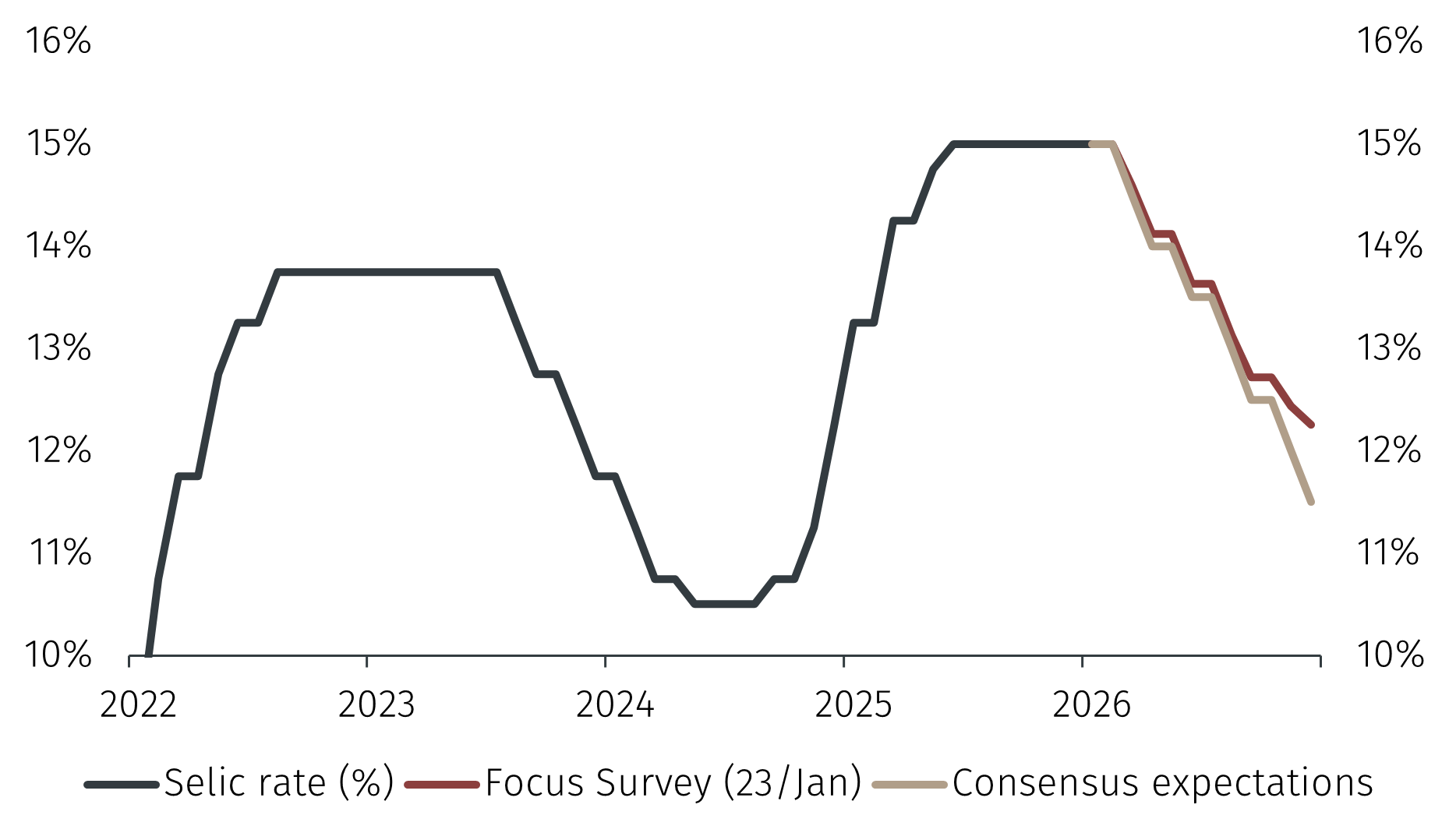

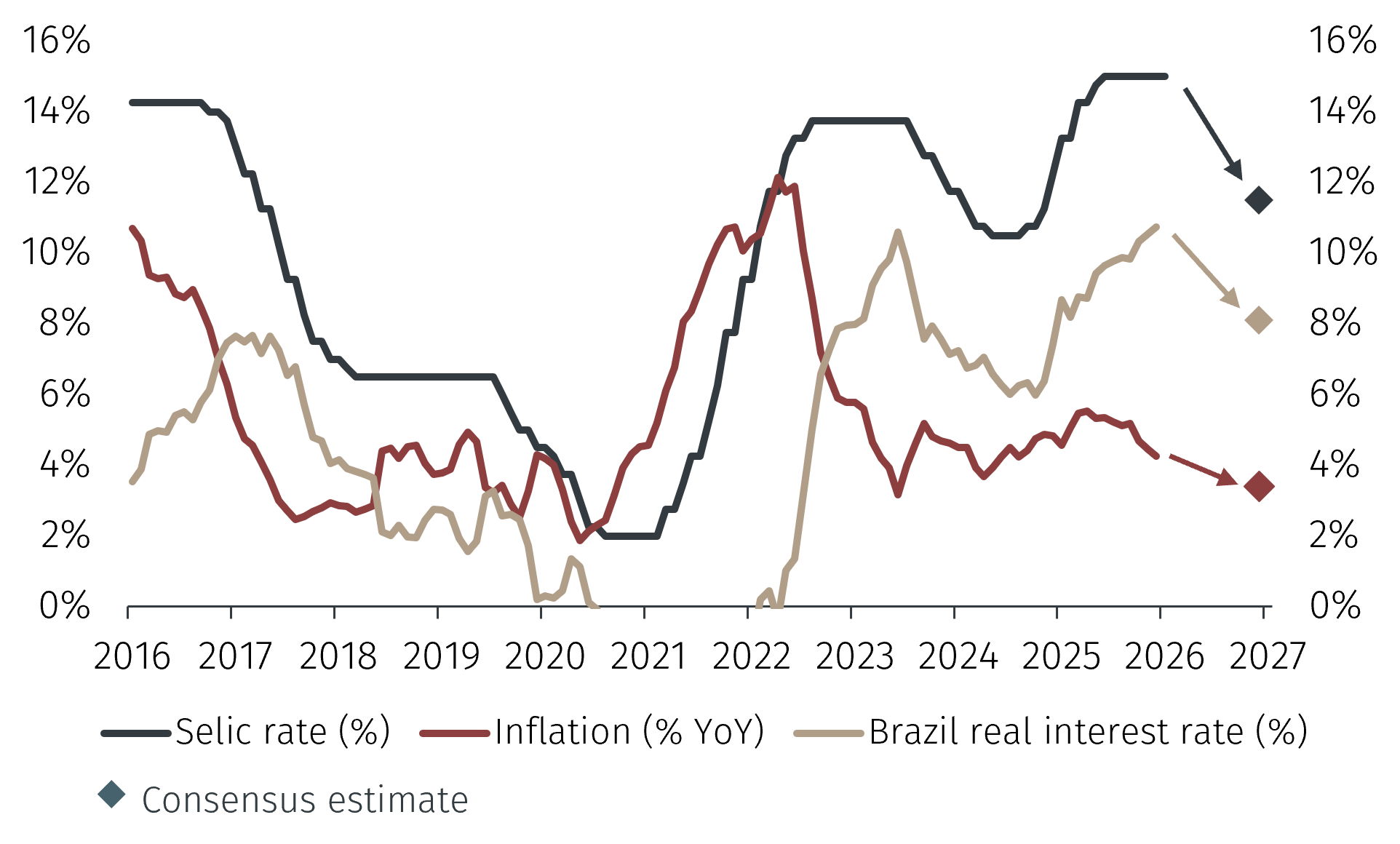

However, Galipolo and the rest of the Copom have operated with total independence. When he took over as governor in January 2025, the Selic rate was 13.25% and inflation was in an upward trend, reaching 5.5% in April. Under his leadership, the Copom voted to raise the monetary policy rate four times by a cumulative 275 basis points, to the current level of 15%. His hawkish stance made it clear that the committee was willing to do “whatever was necessary to fulfill its mandate”.2 This was positively received by markets.

One year after his appointment, Governor Galipolo announced the BCB is likely to start cutting rates from the next meeting in March as economic conditions and lower inflation do not warrant such a restrictive stance of monetary policy. This will be welcomed by the government which will aim to remain in power at the October elections.

Political uncertainty ahead

Although political uncertainty has increased with polls currently not suggesting a clear election winner, the Brazilian real will remain subject to headline risks. The fiscal side seems to be under control following the approval of an electoral law limiting fiscal spending, which will now require two-thirds of support in both upper and lower houses in Congress. Therefore, it is expected that uncertainty will continue at least until nominations of presidential candidates become official in late July. Additionally, after a year where the Brazilian real strengthened by 16% against the US dollar, the expected rate cuts could contribute to weaken the currency in 2026.

Overall, actions from the BCB and its success at bringing down inflation are evidence of the merits of having independence from the government. In times when central banks independence has been called into question, the example of Brazil is one to follow by other emerging economies. In the near term, the reduction in the Selic rate could contribute to weaken the real but will maintain an attractive real interest rate for investors. Political risks will remain until there is clarity in the nominations, but this will add some volatility to domestic assets in 2026.