The ECB reviews its framework roughly every five years to ensure it stays effective. Unlike the 2021 review, which formalised the symmetric 2 percent inflation target and outlined a flexible approach, this year’s exercise was a pragmatic update - adapting the framework to a world few foresaw before the inflation surge of recent years.

What Pythagoras’ theorem can teach us about the Fed

Investment Insights • Macro

2 min read

The ECB’s strategy assessment: evolution, not revolution

In this Macro Flash Note, EFG Chief Economist Stefan Gerlach reviews the European Central Bank’s recent monetary policy strategy assessment. While its core framework remains unchanged, the ECB has introduced important adjustments reflecting new thinking on supply shocks, inflation volatility, scenario analysis, and the balance between forceful and persistent action.

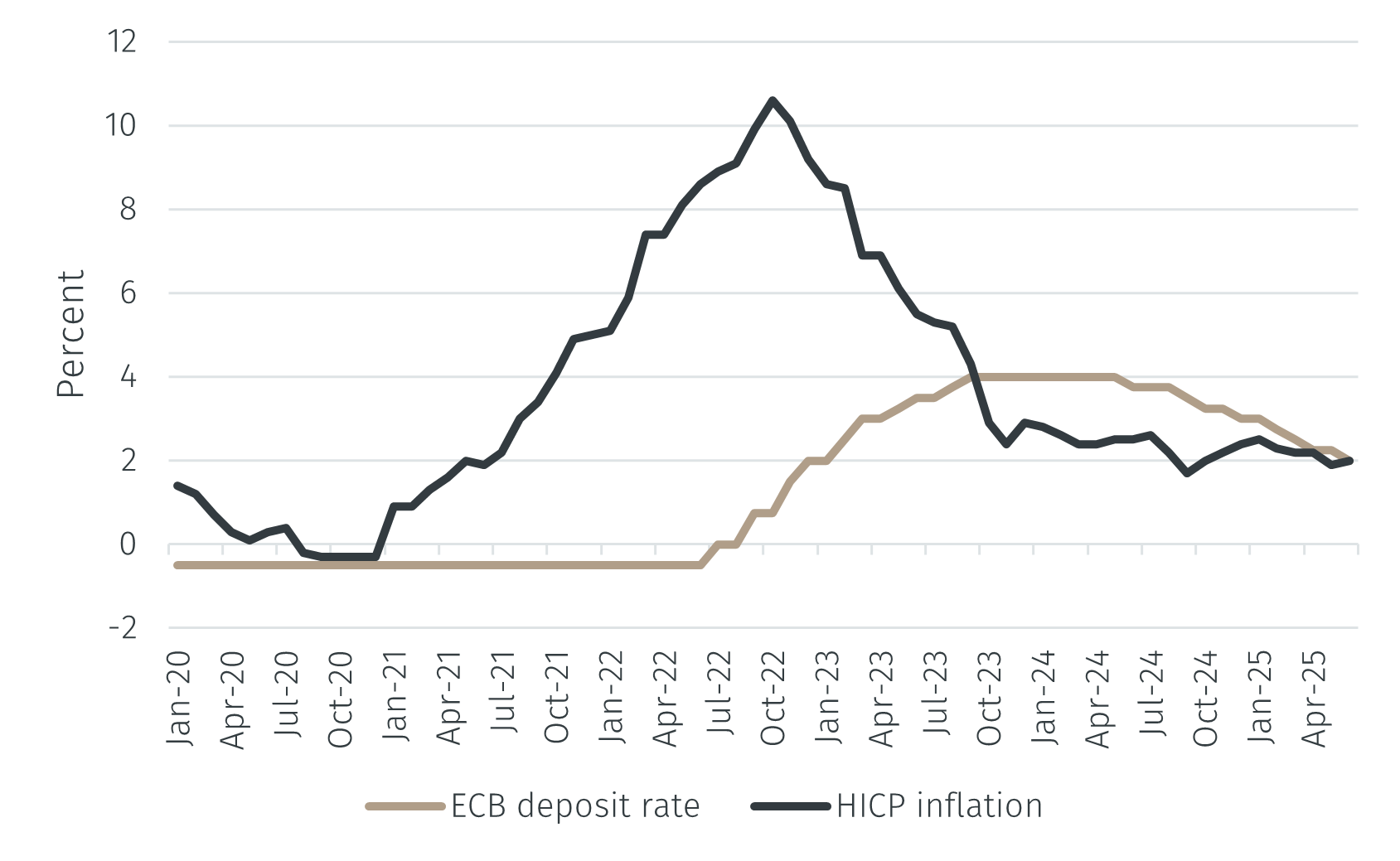

Figure 1. ECB policy rate and eurozone harmonised index of consumer prices (HICP) inflation

Source: FRED. Data as of 18 July 2025.

Three adjustments stand out.

First, the ECB now sees inflation as more uncertain and volatile, with supply-side forces playing a larger role. While supply shocks dominated in the 1970s, recent decades were shaped by weak demand and low inflation. Today, as firms adjust prices more often, inflation has become more sensitive to shocks, amplifying volatility. This raises the question: will the ECB feel tempted to act more resolutely to dampen these non-linear dynamics?

Second, the ECB will place more weight on scenario analysis. Rather than focusing only on the most likely outlook, it recognises that using and communicating alternative scenarios could have improved past decision-making. Going forward, this should enhance transparency and give a clearer sense of the uncertainty surrounding the inflation path.

Third, the ECB has refined its reaction function. It says it will respond with “appropriately forceful or persistent” action to large and sustained deviations from target, whether above or below. Persistence - keeping policy settings in place longer - is seen as a substitute for sharper moves, both at the lower bound and when tightening. Recent experience suggests that holding rates restrictive for longer, but at a lower level, can restore price stability at less economic cost than repeated hikes.

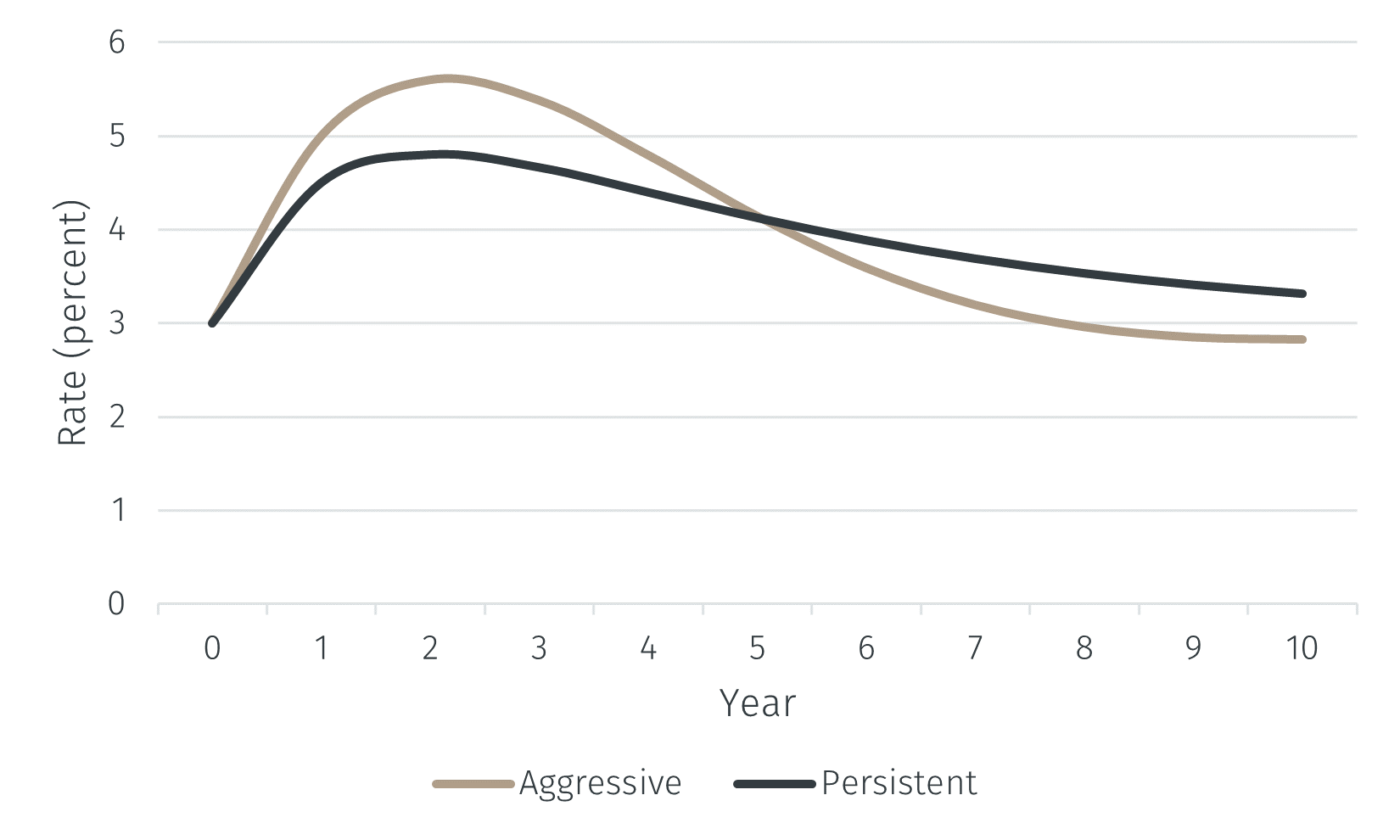

The distinction between aggressive and persistent policy is illustrated in an example where, after a shock, the ECB raises rates. In the aggressive case, rates rise from 3 to 5.8 percent before returning promptly to 3 percent; in the persistent case, they rise to 4.8 percent but are reduced more slowly. 10-year bond yields rise similarly in both cases, assuming markets understand the policy approach and ignoring term premiums.

Figure 2. Agressive versus persistent policy

Source: EFG calculations. Data as of 18 July 2025.

There adjustments reflect a reassessment of recent lessons. The inflation surge and energy shock after the Ukraine war exposed the limits of focusing on demand-driven inflation and underestimating supply factors. Meanwhile, faster and more frequent price adjustments by firms have added volatility and asymmetry, as prices tend to rise faster than they fall, complicating policy calibration.

Anchoring inflation expectations has also become more challenging. Previously, the ECB mainly worried about expectations drifting downward; now, upside risks matter too. Its approach is more explicitly symmetric, aiming to keep expectations anchored against both positive and negative shocks.

Finally, the ECB acknowledges the need for clearer communication. A stronger focus on scenario analysis should improve its interaction with markets and the public and reduce the risk of conveying a false sense of precision.

In short, this strategy assessment marks a shift in emphasis, not direction. The ECB’s framework remains broadly fit for purpose, but the world has changed - and so must the way policy is assessed and implemented. Whether these changes will prove sufficient will depend, as always, on the shocks that lie ahead.