Following the events of “Liberation Day” on 02 April, when the Trump administration imposed sweeping tariffs on many of its trading partners, the outlook for Japan’s economy appeared to deteriorate. The US announced it would impose a 24% tariff on imports of goods from Japan. This had the potential to prove a crippling blow to the Japanese economy, which sent more goods to the US in 2024 than to any other country.1

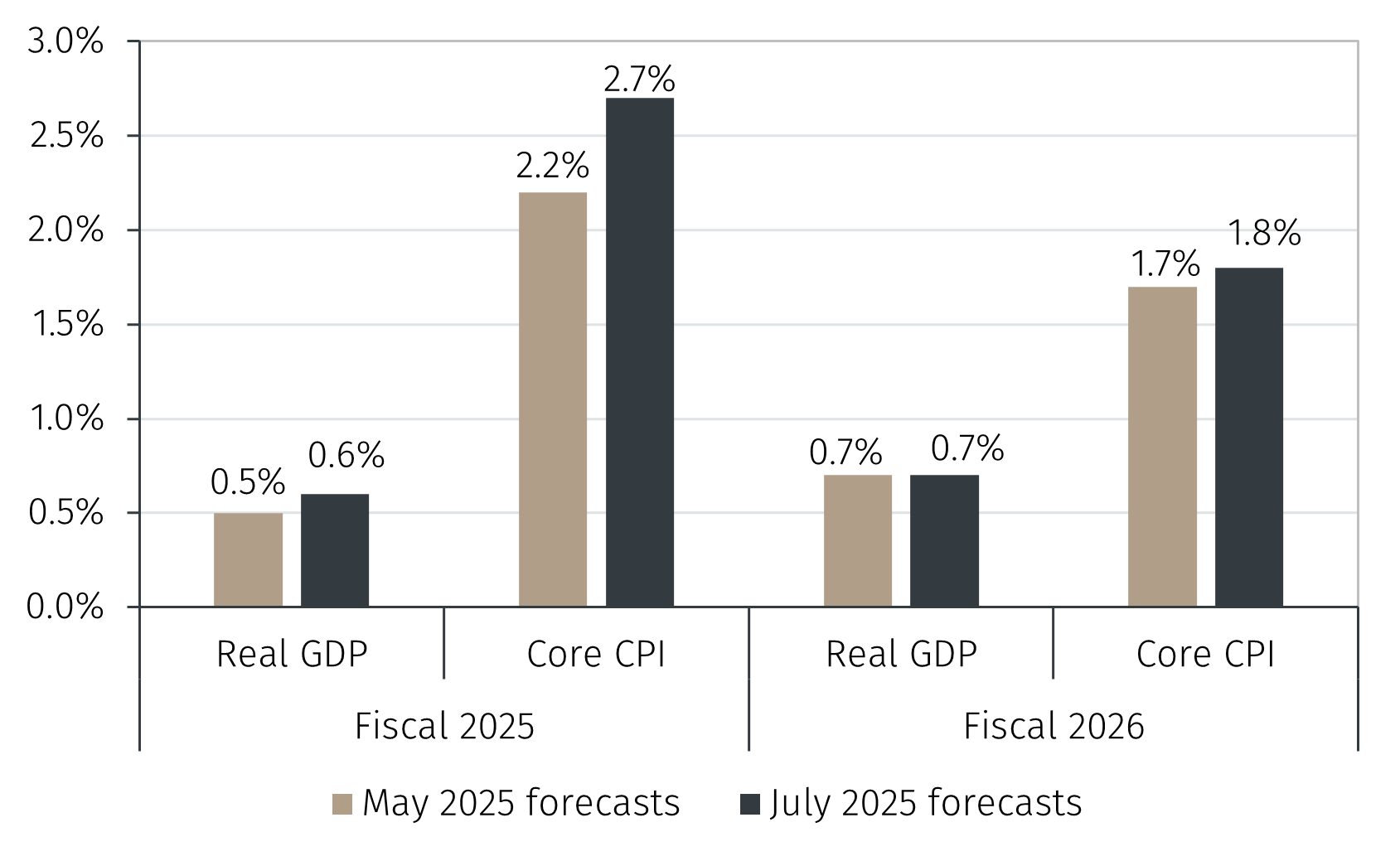

Despite an initial 90-day pause on US tariffs on 09 April, with a lower rate of 10% imposed during this period, Bank of Japan (BoJ) Policy Board members still revised their forecasts lower for real gross domestic product (GDP) growth in fiscal years 2025 and 2026.2 These revisions reflected the view that the Trump administration’s trade policies would result in lower exports and production both globally and domestically.

In July, Japan agreed a bilateral trade deal with the US, with its tariff rate set at 15% in exchange for a US-destined USD 550 billion Japanese investment package. The deal is not expected to lead to significantly higher GDP growth, with only a 0.1 percentage point upward revision to the forecast for fiscal year 2025 at the BoJ’s July meeting (see Chart 1).3