Recent developments in US trade policy — particularly the announcement of sweeping new tariffs by the Trump administration on what has been referred to as “Liberation Day” — raise questions about the likely response of the Federal Reserve. The effects on inflation and economic activity are unclear, as they will also depend on whether and how foreign countries choose to retaliate. To analyse the Fed’s potential policy choices, one ideally needs a fully articulated macroeconomic model. In the absence of that, this note uses a simple Taylor Rule to offer a first rough assessment of how the central bank might react.

The Taylor Rule Framework

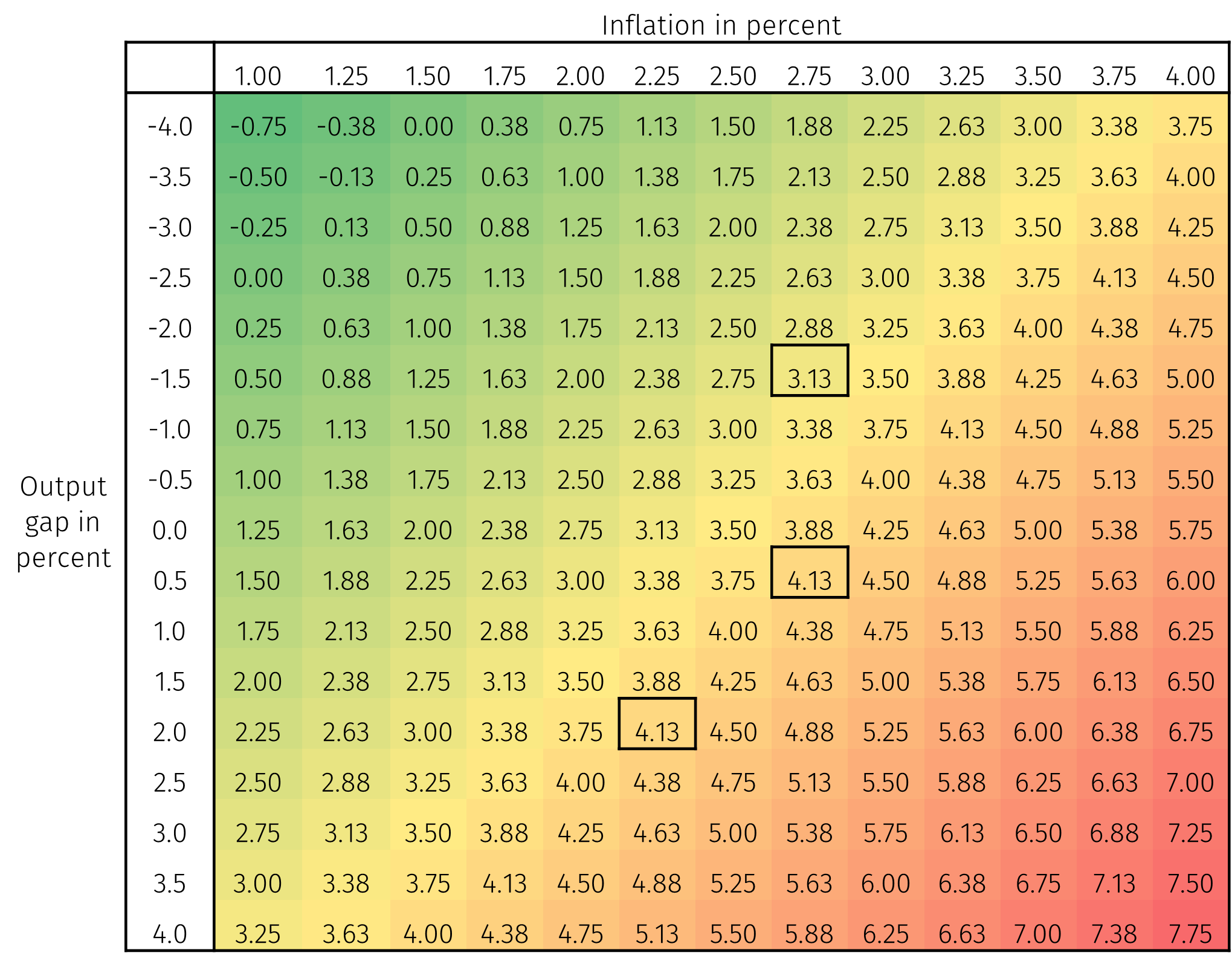

Originally proposed by John Taylor in 1993, the rule was merely intended to summarise how the Federal Reserve had set interest rates in the late 1980s and early 1990s.1 It has since become a standard reference in monetary policy analysis. According to the original specification, the interest rate is determined by four main elements:

- The Equilibrium Real Interest Rate: Taylor assumed this rate to be 2%. More recent estimates suggest it may be lower. For the purposes of this exercise, a value of 0.75% is used, which is consistent with recent estimates from staff economists at the Federal Reserve Bank of New York.2

- Inflation: The rule uses the four-quarter change in the GDP deflator, a measure of the prices of domestically produced goods and services. This is relevant because it excludes all imported goods and services and may therefore be less sensitive to tariff-induced price changes than the consumer price index.

- The Inflation Gap: The difference between actual inflation and the inflation target, assumed to be 2%, is assigned a response coefficient of 0.5. A one percentage point increase in inflation thus has two effects on interest rates: it raises interest rates one-for-one as mentioned above, and by an additional 0.5% as inflation rises relative to target.

- The Output Gap: The deviation of real GDP from potential GDP is also given a coefficient of 0.5. A one percentage point shortfall in output relative to potential leads to a 0.5 percentage point reduction in the interest rate.

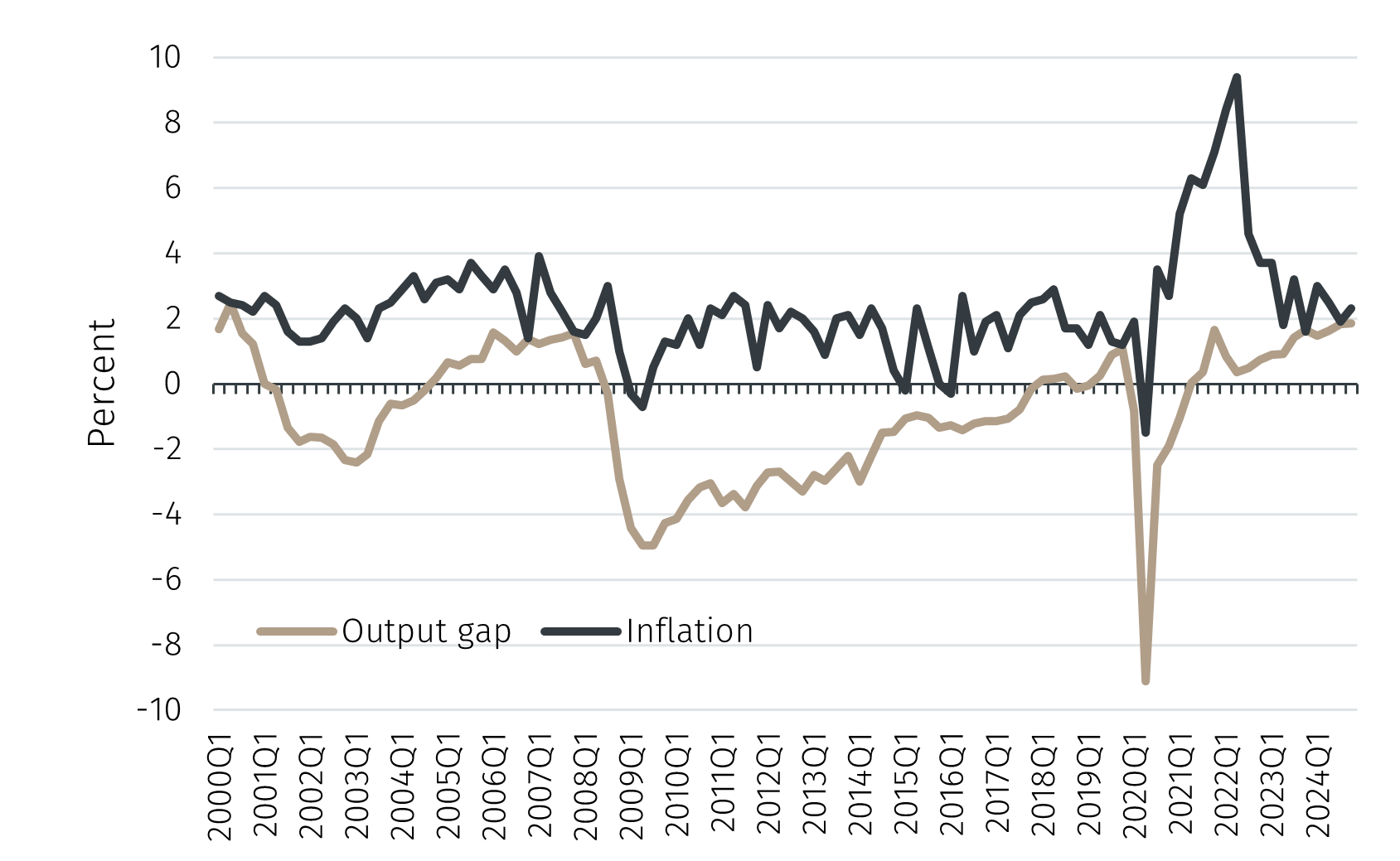

Current Conditions

Based on recent data, the output gap in the fourth quarter of 2024 was approximately 1.9%, and the four-quarter change in the GDP deflator was 2.3%. Since these data series used in the rule may not be familiar to all readers, they are shown in the chart below.