There were no surprises at the last meeting of the Bank of England (BoE)’s Monetary Policy Committee (MPC) where two main decisions were taken. The first decision related to the level of the Bank rate, the BoE’s main monetary policy tool, which was maintained at 4.0%. This was priced-in by markets given the evolution of data on activity, the labor market and inflationary pressures.

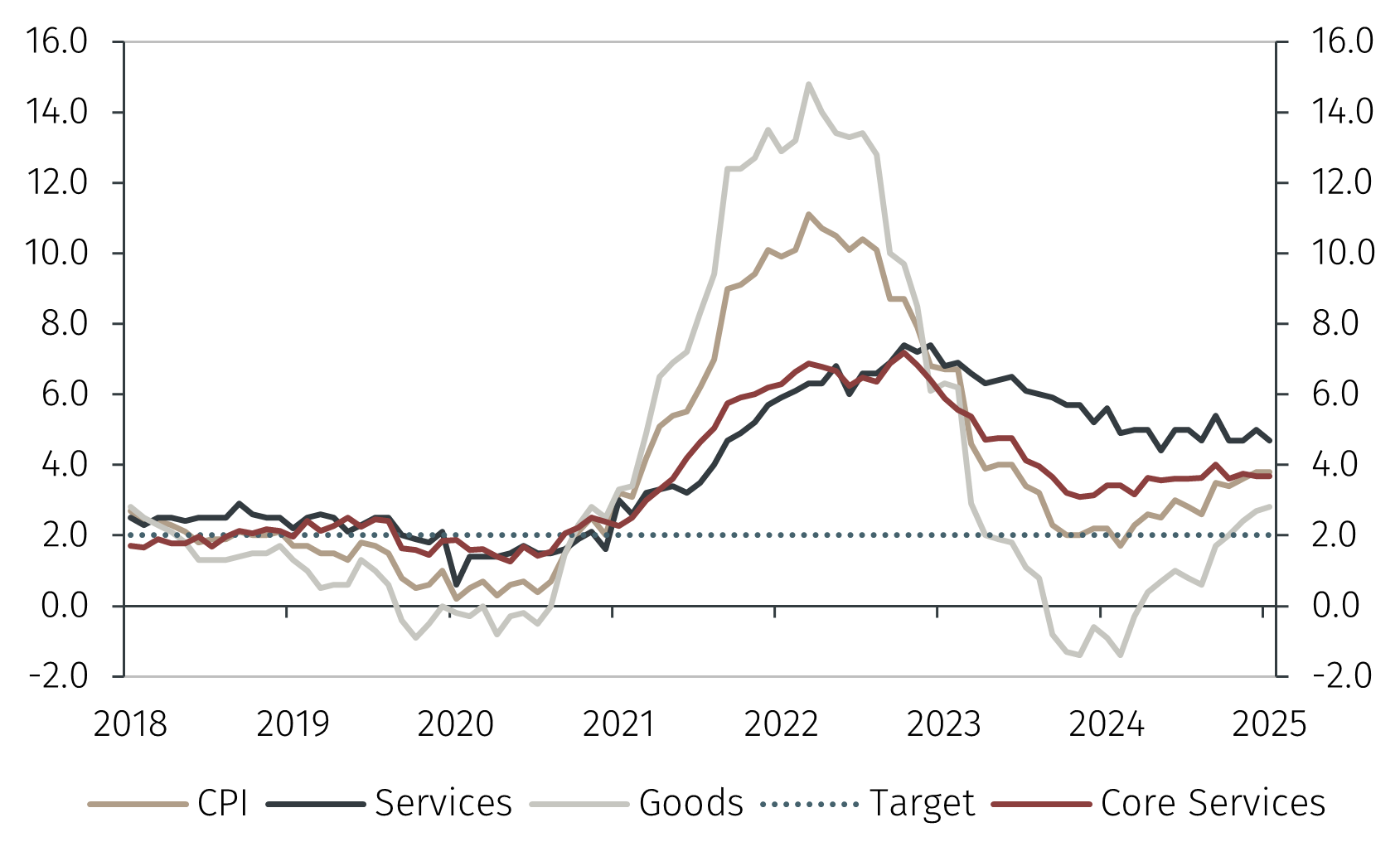

UK inflation remained elevated in August at 3.8% year-on-year (YoY). The BoE estimates inflation to peak close to 4.0% in September before gradually converging to the 2.0% target in 2027. Services prices, which have been a key driver of domestic price pressures, decelerated marginally last month to 4.7% YoY, while goods prices picked-up to 2.8% YoY.

Our estimates show that a measure of core services inflation, excluding volatile components, administered prices, rents and packaged holidays, has stabilised at 3.7% YoY in August (see Chart 1). BoE Governor Andrew Bailey said that government policies related to payroll taxes and increases in the minimum wage added to inflationary pressures.