The budget came against a backdrop of controversy, in which the Office for Budget Responsibility (OBR), the UK’s fiscal watchdog, leaked its Economic and Fiscal Outlook ahead of the budget announcement. Despite this, Chancellor Reeves presented a more optimistic view of the UK economy than what was initially anticipated.

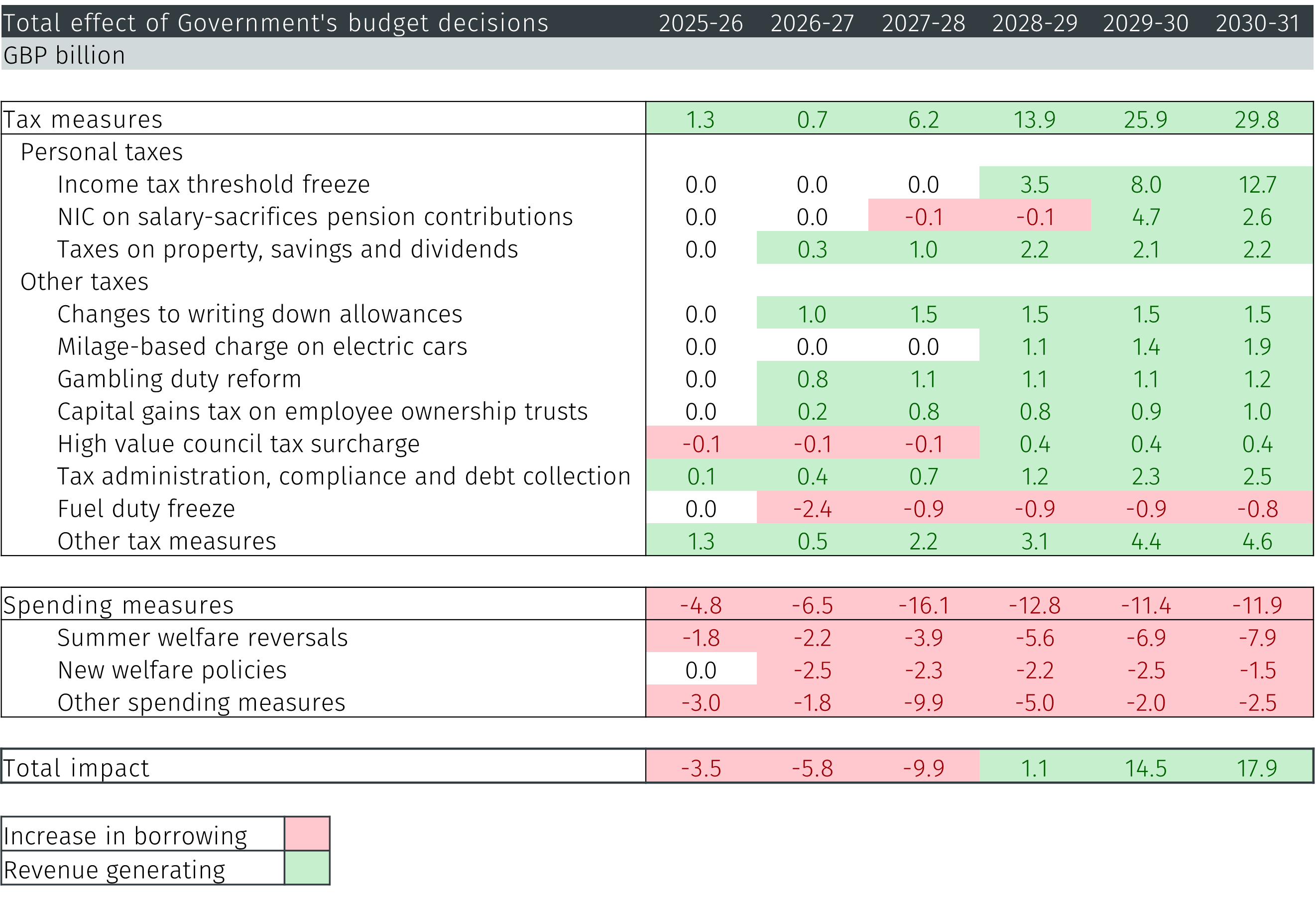

The Chancellor announced a series of tax increases aimed at raising revenues by £26bn by Fiscal Year (FY) 2029-30. These intend to keep one of Labour’s pledges not to change corporation tax nor income tax, national insurance or VAT. This is difficult as the latter three taxes represent over 60% of the UK’s total tax revenue.1 Additionally, Reeves’ spending measures focused on reversing changes to welfare policies, looking to benefit lower income households.

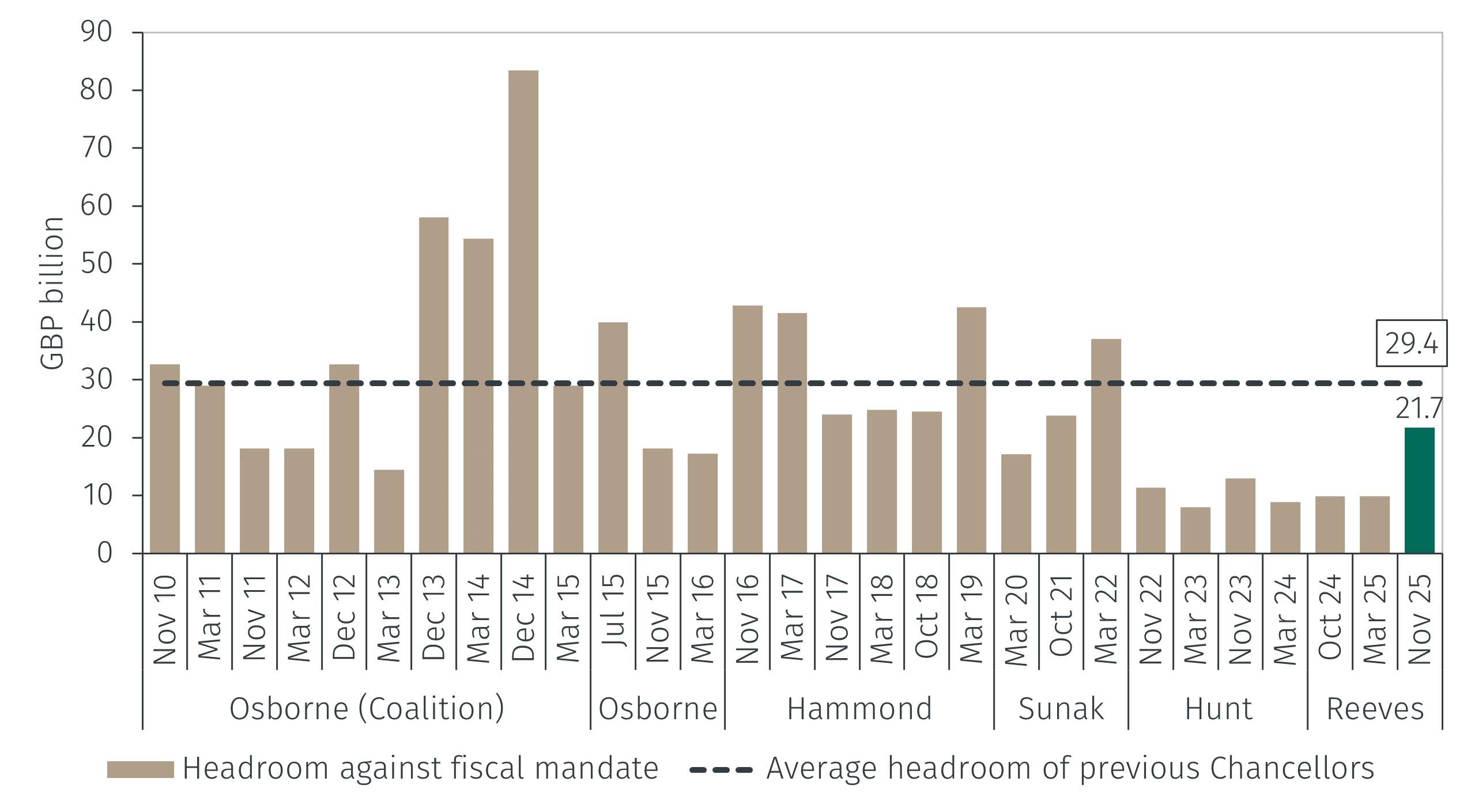

Despite the lack of direct measures to reduce the UK’s fiscal deficit, markets welcomed these announcements. However, officials acknowledged the fiscal situation remains challenging and long-term debt sustainability remains a concern. For that, the government chose the path of tax increases and short-term increase in spending to generate conditions for the private sector to drive economic growth.

Budget details

The government plans to make a series of back-loaded changes to personal taxes that are only expected to take effect from FY 2028-29. These include freezing the income tax thresholds and lowering the tax incentives for salary sacrifice programs. It plans to increase income tax rates on property, savings and dividends, which are expected to take effect FY 2026-27.

Additionally, it expects to make a number of other changes including writing down allowances, introducing milage-based charges on electric cars, changing gambling duties, and introducing a surcharge on high-value council taxes. The estimated effects of these measures are summarised in Table 1.