Prior to the recent US-Israel attack on Iran, disinflation in the UK continued. This reflected partly the restrictive stance of monetary policy, which was reflected in weakening economic growth and labour market softness. Data from the Office for National Statistics showed that GDP growth was flat in January, and the labour market showed signs of deterioration. Inflation had slowed from 3.4% year-on-year (YoY) in December 2025 to 3.0% YoY in January 2026, and the BoE expected inflation would reach the 2% target in April following the changes to the cap in energy bills announced by the Government in the 2025 Budget.

Brazil on the rise: what to know in 2026

Investment Insights • Macro

2 min read

BoE unanimously on hold, but where next amid Middle East uncertainty?

On 19 March the Bank of England (BoE)’s Monetary Policy Committee (MPC) voted unanimously to keep Bank rate on hold at 3.75% as markets expected. However, the MPC has left the door open for further changes to its monetary policy in either direction. In this Macro Flash Note, Economist and Strategist Joaquin Thul discusses what lies ahead for the BoE.

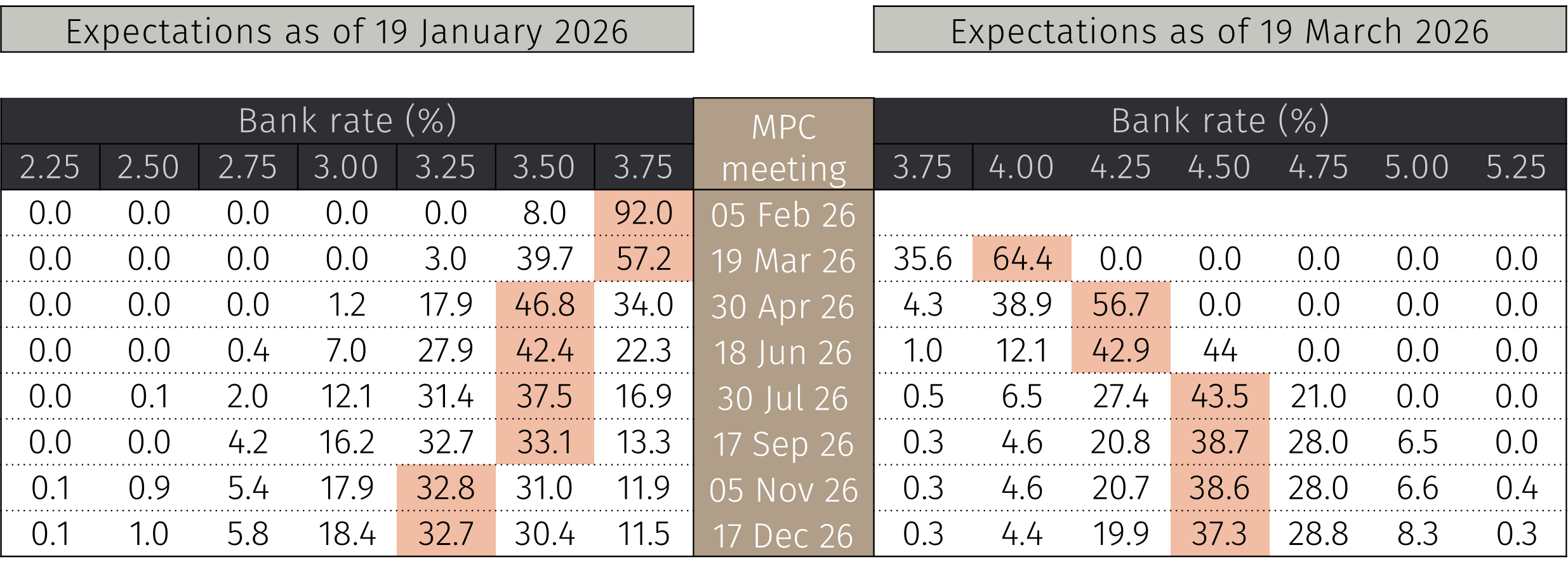

Chart 1. Market expectations have shifted from two rate cuts in 2026 to three rate hikes (Probabilities %)

Source: LSEG Data & Analytics and EFG. Data as of 19 March 2026.

However, the situation changed following the escalation of the conflict in Middle East and the rise in energy prices following the closure of the Strait of Hormuz. This constituted an important supply shock to the UK economy.

Following this, the MPC has increased its short-term outlook for inflation to 3.0%-3.5% between Q2 and Q3. These calculations are based on the price of crude oil remaining around USD 90-100 per barrel and the cost of European wholesale gas around EUR 50 per MWh.

While oil prices would directly spill-over to supply chains across the economy, higher wholesale gas prices are expected to have a small impact on household utility bills. This is because the latest energy price cap from April to June has already been set by the Government. However, if rising prices persist, then these could feed through into a higher energy price cap from July1. Overall, the BoE projects that the direct contribution to annual inflation from rising oil and gas prices would be 0.75% in Q3-2026.

The MPC is clearly on a wait-and-see mode until the next MPC meeting. The uncertainty over the resolution of this conflict meant that they have left the door open for further policy adjustments in either direction.

- If the conflict were to drag on for many months, then the risks of second-round effects in prices and wages would be higher and require an even more restrictive policy stance. Markets are currently pricing between two to three rate hikes in that scenario (see Chart 1).

- If, on the other hand, the conflict were to be resolved in the coming weeks, or at least a solution is found to allow a more normal flow of trade through the Strait of Hormuz, then policy might need to be less restrictive, opening the possibility for rate cuts in the second half of the year.

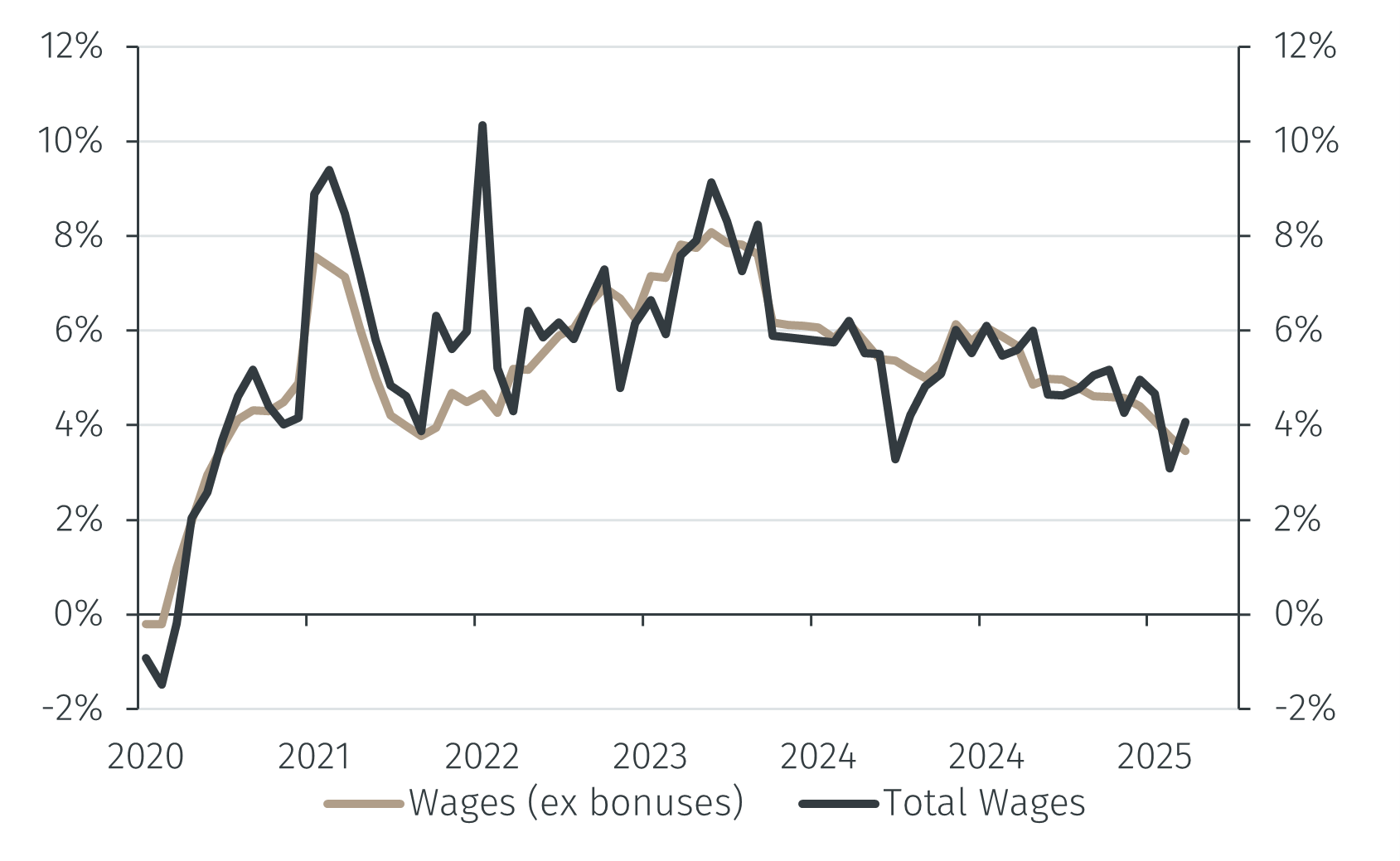

Chart 2. Wage growth % year-on-year

Source: LSEG Data & Analytics and EFG. Data as of 19 March 2026.

Recent labour market data raises the threshold for interest rate hikes. Wage growth has softened from 3.8% YoY in December to 3.4% YoY in January, excluding bonuses (see Chart 2). Together with a low vacancy rate and an unemployment rate above 5%, the decision to raise Bank rate in the coming months will require a much larger impact of energy prices on inflation.

Conclusion

The decision from the MPC to keep rates on hold, given the uncertainty created by the conflict in Middle East was correct in our view. In an attempt to avoid repeating past policy mistakes, this cautious approach allows policymakers to assess the developments in the coming weeks before either continuing the easing process or hiking rates.

Recent weakness in the labour market and the decline in wage growth will set a higher threshold for the BoE to hike interest rates in the near term. Market expectations are particularly hawkish, with two or three rate hikes expected in 2026.

Policy will remain highly dependent on external factors and on whether the war eases pressure on commodity prices by May, when the next energy price cap will be announced by the government.

1 The new energy price caps for the period between July and September will be announced on 27 May 2026.