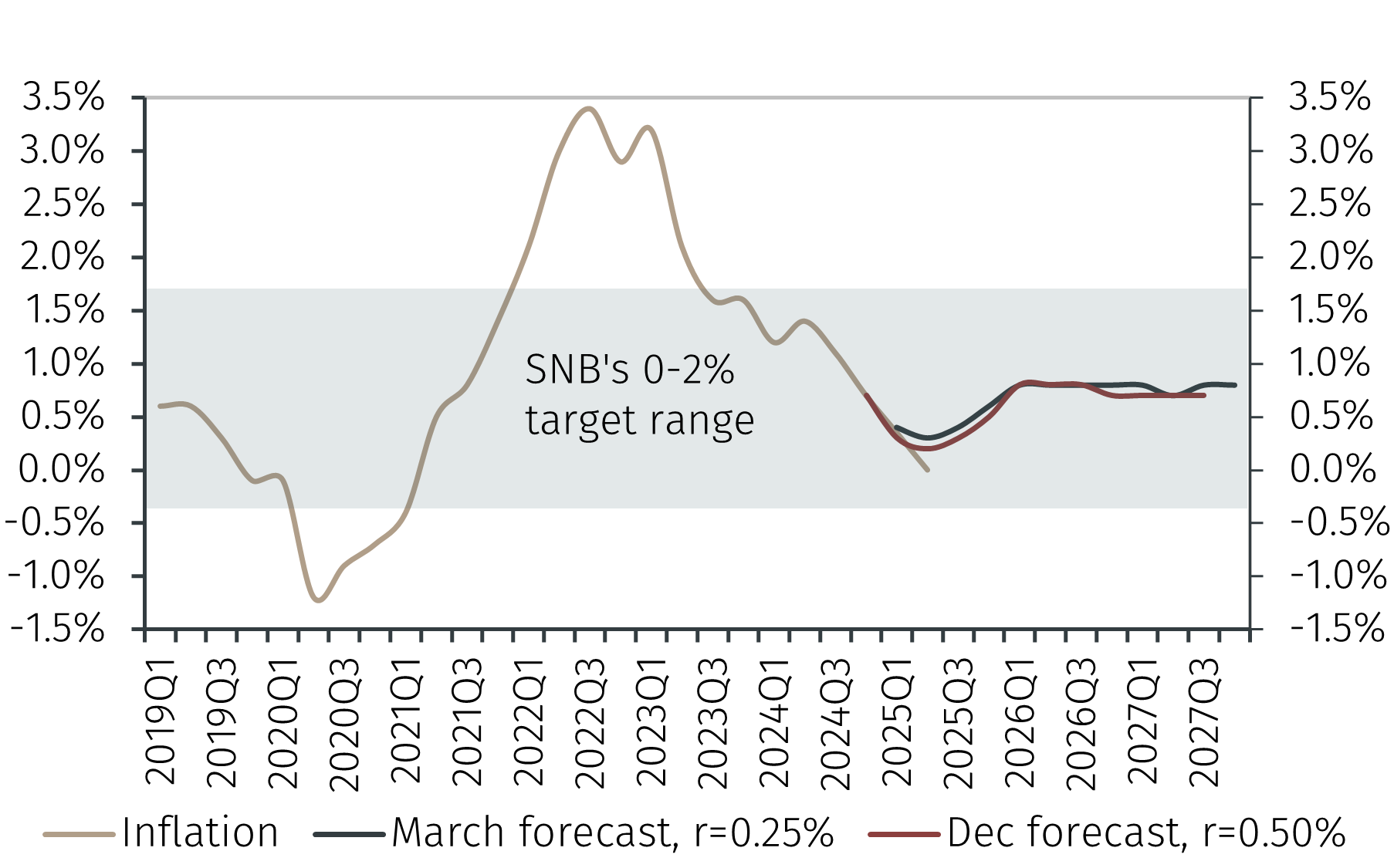

Market participants fully anticipate the SNB to cut the policy rate by 25 basis points to 0.00% on June 19. Furthermore, the prices of futures contracts on the Swiss short-term interest rate point to a 25% probability that the policy rate will turn negative before year-end either following a 50 basis points cut in June or another 25 basis point reduction in the policy rate after the summer.

However, with the economy growing above expectations in early 2025 and showing resilience in Q2 there is no urgency for the central bank to return to negative interest rates, an unpopular policy among the Swiss public.

The market expectation of a rate cut in June reflects the recent decline in inflation. Headline CPI fell 0.1% year on year (yoy) in May and core CPI, as measured by the Federal Statistical Office, rose only 0.5% yoy. The data up to May points to another undershoot of March SNB’s conditional inflation forecast.