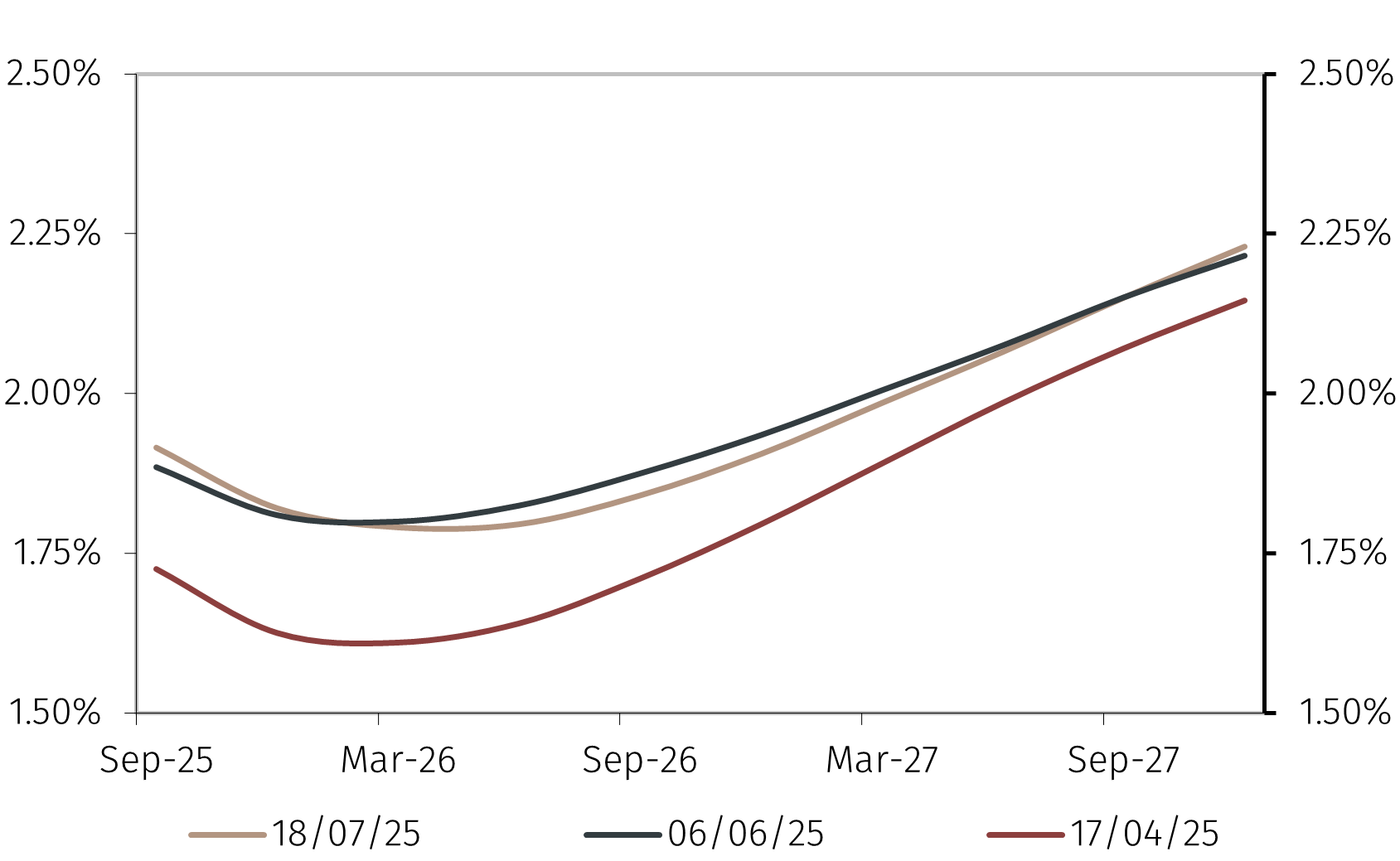

The ECB's Governing Council is expected to leave interest rates unchanged at 2% on 24 July, interrupting the series of seven rate cuts since last September and in line with market expectations (see Chart 1).

What Pythagoras’ theorem can teach us about the Fed

Investment Insights • Macro

2 min read

Which factors are the ECB watching closely?

On 24 July, the European Central Bank (ECB) is widely expected to leave interest rates unchanged. Inflation has returned to target and uncertainty is high due to trade negotiations. In this Macro Flash Note, Senior Economist GianLuigi Mandruzzato argues that the ECB will wait for more clarity before considering any change in interest rates.

Chart 1. Eurozone 3-month interbank rate implied in futures contracts

Source: LSEG Data & Analytics and EFGAM calculations. Data as of 18 July 2025.

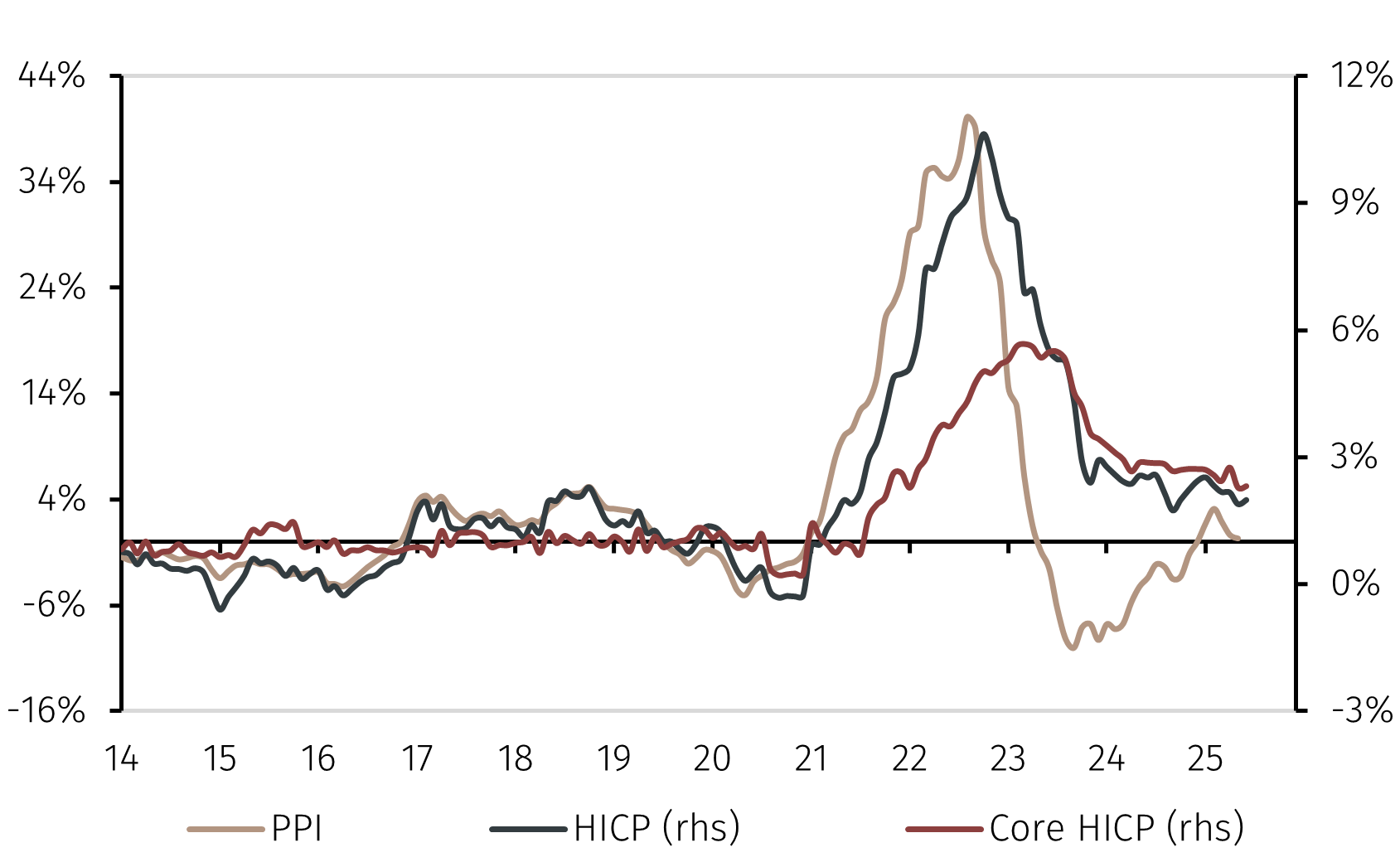

Maintaining the current policy stance seems appropriate. Headline inflation is at the 2% target and core inflation, excluding food and energy, is at its lowest level since early 2022 (see Chart 2). The fight against the high inflation of recent years can be considered concluded, and the deposit facility rate is in line with estimates of its neutral level.1

Chart 2. Eurozone HICP and PPI inflation (Year-on-Year)

Source: LSEG Data & Analytics and EFGAM calculations. Data as of 18 July 2025.

The ECB projects inflation to decline temporarily to 1.4% year-on-year by early 2026, following the decline in fuel prices and the appreciation of the euro in the first few months of the year. Given that the ECB's objective is to ensure price stability over the medium term, it has little reason to change its monetary policy stance in the short term.

What factors will influence the ECB's future monetary policy?

We think four main factors will determine the future course for ECB monetary policy.

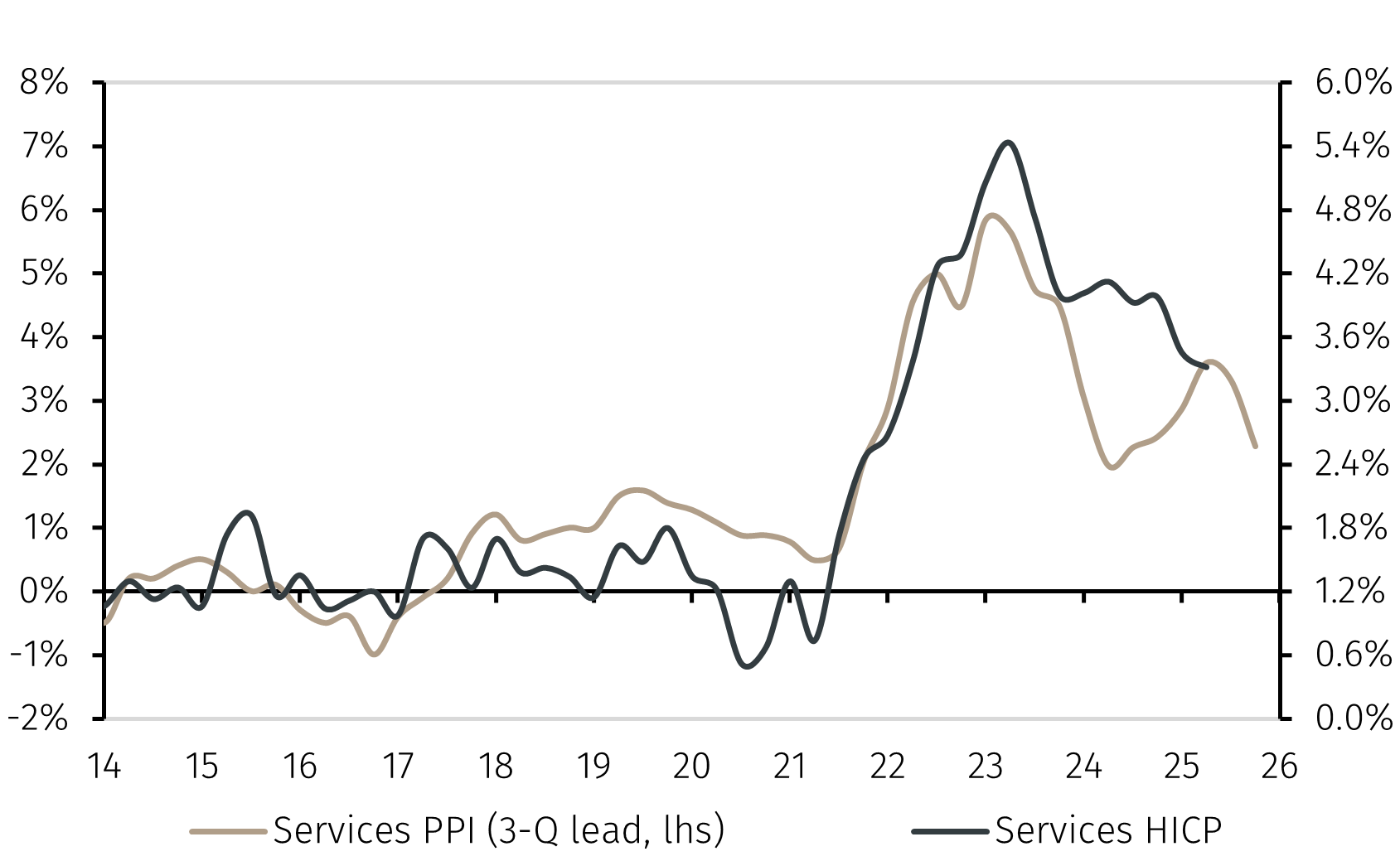

The first is moderate producer prices for goods and services (see Charts 2 and 3). If the producer price index (PPI)- harmonised index of consumer prices (HICP) pass-through is similar to history, that would mean that inflation would be lower than the ECB projects.

Chart 3. Services PPI and HICP (Year-on-Year)

Source: LSEG Data & Analytics and EFGAM calculations. Data as of 18 July 2025.

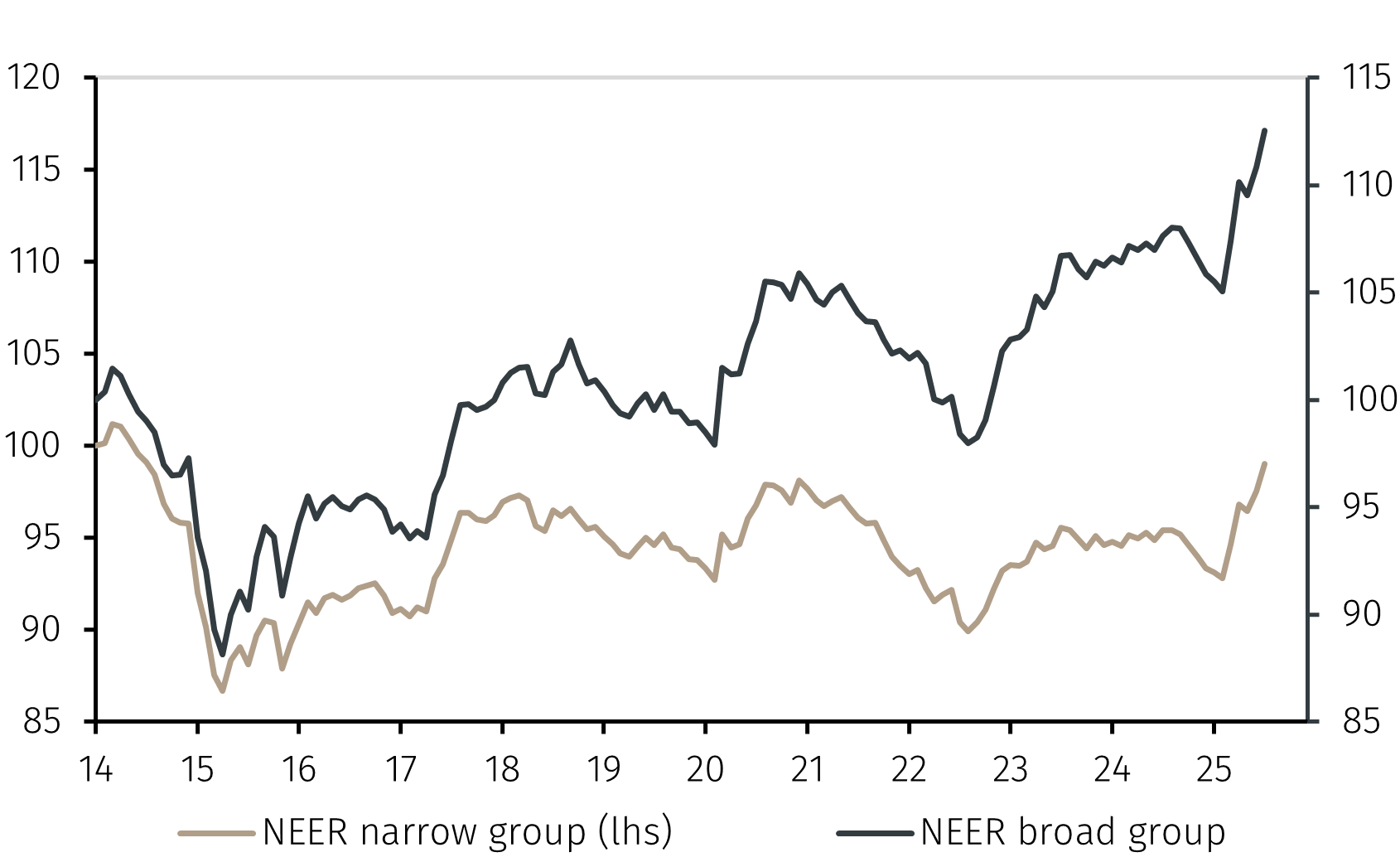

The second is the appreciation of the euro. The euro's nominal effective exchange rate (NEER) is about 3.5% higher than assumed in the ECB’s June projections. If sustained, such a development would cut inflation by 0.1% or 0.2% after a year, according to ECB estimates.2

Chart 4. Euro trade-weighted exchange rates

Source: LSEG Data & Analytics and EFGAM calculations. Data as of 18 July 2025.

The third, and possibly the highest source of uncertainty, is the outcome of the trade negotiations with the US. The terms of both the EU-US bilateral agreement and those between the US and other major economies, including China and Japan, will matter. Beyond the impact on growth, the outcome of the trade negotiations could cause an inflow of low-cost intermediate and consumer goods into the European market, putting downward pressure on eurozone inflation.

The fourth and final factor is the speed of implementation and effectiveness of European fiscal plans, including in Germany, which focus on defence and infrastructure spending. If the fiscal stimulus leads to stronger-than-expected growth, the risk of an undershoot of the ECB’s inflation target would diminish.

Conclusions

The ECB is expected to leave interest rates unchanged on 24 July. Inflation has returned to 2% year-on-year and uncertainty around the outlook remains high. The ECB will wait for more clarity about the trade negotiations with the US before considering any change in interest rates.

The bar for an interest rate cut in the coming months seems high. However, several factors point to the risk of lower-than-expected inflation. If confirmed by the data, the chances of further rate cuts in the remainder of 2025 and early 2026 would rise strongly.

1 The neutral level of interest rate is that which neither stimulates nor constrains the economy.

2 See “Exchange rate pass-through in the euro area and EU countries», ECB Occasional Paper, April 2020.