IMF growth forecasts

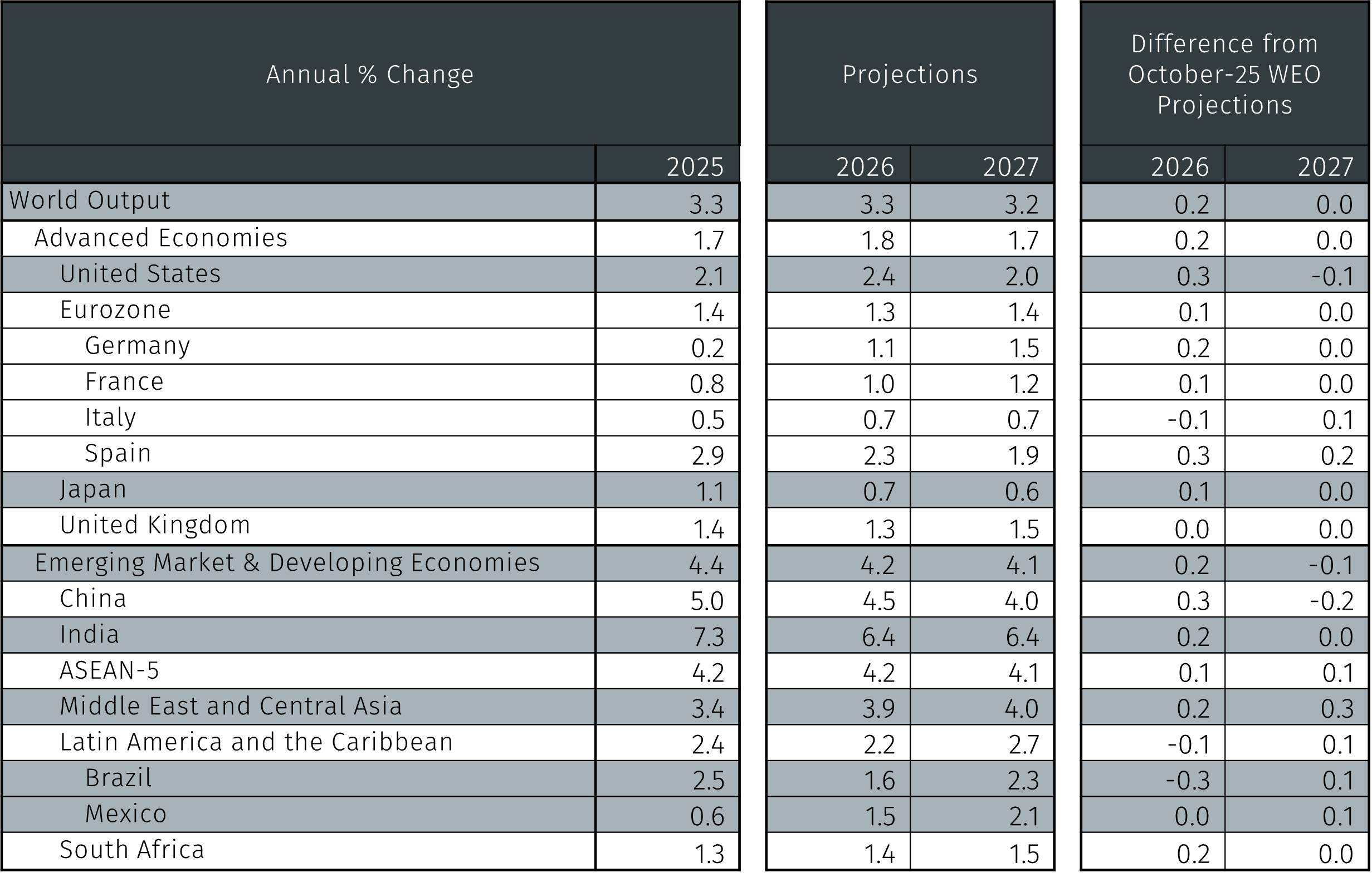

The IMF forecasts global real gross domestic product (GDP) growth of 3.3% and 3.2%, for 2026 and 2027 respectively. Compared to the October WEO, this marks a small upward revision of 0.2 percentage points for 2026 and no change for 2027. The revision reflects stronger than expected momentum in late 2025, particularly in economies benefiting from technology investment and fiscal support.

No need for negative SNB rates

Investment Insights • Macro

2 min read

IMF: Global Economy - Steady and Divergent Forces

The International Monetary Fund (IMF) recently released its January 2026 World Economic Outlook (WEO) Update*, highlighting continued resilience in global growth despite persistent policy uncertainty and geopolitical risks. Relative to the October 2025 WEO, the January update reflects modest improvement in the near-term outlook. In this Macro Flash Note, Haya Kamal summarises the key messages from the report.

Haya Kamal

Table 1. IMF’s WEO real GDP growth projections (% change, year-on-year)

Source: IMF, World Economic Outlook Update, January 2026.

Global growth

Generally, global growth is expected to remain steady, as high-technology sectors are projected to lose some momentum, but to continue partly offsetting weaknesses in other areas2. There have been significant revisions for certain countries, with the changes occurring in different directions. Growth in advanced economies for 2026 has been revised upwards compared with that in the October 2025 WEO. This is supported by accommodative financial conditions, easing monetary policy in some jurisdictions, and near-term fiscal stimulus. However, underlying momentum remains subdued due to structural constraints, energy-related pressures, and weaker productivity outside technology-intensive sectors.

The 0.3 percentage point upward revision to the United States’ growth outlook reflects a stronger-than-expected outturn in late 2025, an end to the federal government shutdown, and continued fiscal support. Technology investment has played a central role, helping to offset the drag from lower immigration and moderating consumption. The IMF expects growth in 2027 to remain at 2.0%, with a near-term fiscal boost from tax incentives for corporate investment under the One Big Beautiful Bill Act (OBBBA) of 2025.3

The eurozone outlook is broadly unchanged, with modest growth reflecting unresolved structural headwinds and limited benefits from the global technology investment boom. Increased public spending, particularly in Germany, supports activity. Ongoing high energy prices following Russia’s invasion of Ukraine, will continue to weigh on manufacturing, with further pressure from the euro’s appreciation relative to currencies of countries exporting similar goods. Japan’s outlook has been revised slightly upward, mainly due to the recently announced fiscal stimulus.

The IMF expects growth in emerging markets (EM) to remain just above recent averages, supported by easing trade tensions and resilient domestic demand in some regions. However, growth forecasts remain uneven across various countries. For example, China’s upward revisions reflect additional stimulus measures, increased policy bank lending, and lower effective US tariffs. These factors help offset weak domestic demand, particularly in the housing sector.

In the Middle East and Central Asia, growth is projected to rise from 3.7% in 2025 to 3.9% in 2026, and further to 4.0% in 2027. This growth is supported by higher oil output, resilient domestic demand, and ongoing reform efforts4. Conversely, Latin America’s 2026 forecast was downgraded by 0.1 percentage points, as countries in the region face different cyclical headwinds. Of all the regions seen in Table 1, Brazil saw the largest downgrade of 0.3 percentage points.

Furthermore, the IMF projects global headline inflation to decline from 4.1% in 2025, to 3.8% in 2026 and further to 3.4% in 2027. This is supported by easing energy prices, softening demand, and improving supply conditions. While inflation dynamics differ across regions, the overall disinflation trend remains intact and broadly unchanged from October.

Risks to the outlook

Risks to the outlook remain as tilted to the downside. The IMF highlights the vulnerability created by the narrow base of growth drivers, particularly heavy reliance on artificial intelligence (AI)-related investment. A reassessment of AI productivity expectations could trigger investment pullbacks, equity market corrections, and tighter financial conditions.

Further risks emerge from fragile trade policy dynamics, potential escalation of geopolitical tensions, and high public debt levels in major economies. While trade tensions have eased since October, they remain susceptible to renewed flare-ups, reinforcing the IMF’s emphasis on policies that reduce uncertainty and rebuild fiscal buffers.

With that said, the IMF highlights upside potential if rapid AI adoption translates into durable productivity gains and if trade tensions continue to ease. The balance of risks reflects the economy’s increasing reliance on a limited number of growth drivers.

Conclusion

The views from the IMF’s report are in line with the EFG Outlook 2026, where we expect the US to lead economic growth among developed economies.5 This is supported by the resilience of the US economy, their leadership in terms of its technology investment and the clear growth plan set by the Trump administration. Additionally, as noted by the IMF, there are cyclical factors such as the fiscal stimulus from the OBBBA, the lower interest rate environment, and the effects from lower energy prices, which will also help US growth in 2026. Elsewhere, we expect China to lead GDP growth among emerging economies, based on the dynamism of its economy and the rapid adoption of new technologies.

* https://www.imf.org/en/publications/weo/issues/2026/01/19/world-economic-outlook-update-january-2026 2 https://www.imf.org/-/media/files/publications/weo/2026/january/english/text.pdf

3 https://www.imf.org/-/media/files/publications/weo/2026/january/english/text.pdf

4 https://www.imf.org/-/media/files/publications/weo/2026/january/english/text.pdf

5 https://www.efginternational.com/uk/insights/outlook-2026.html