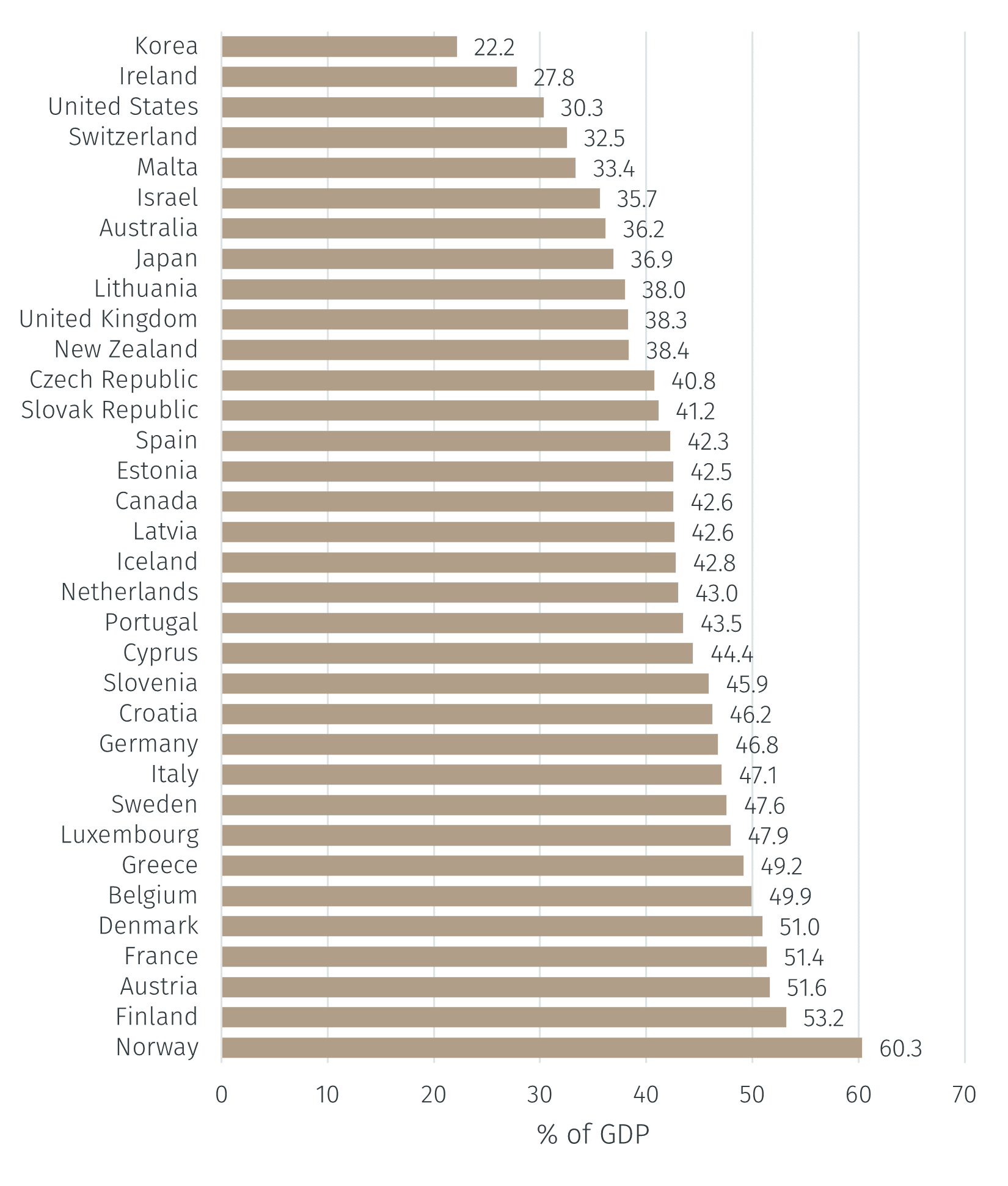

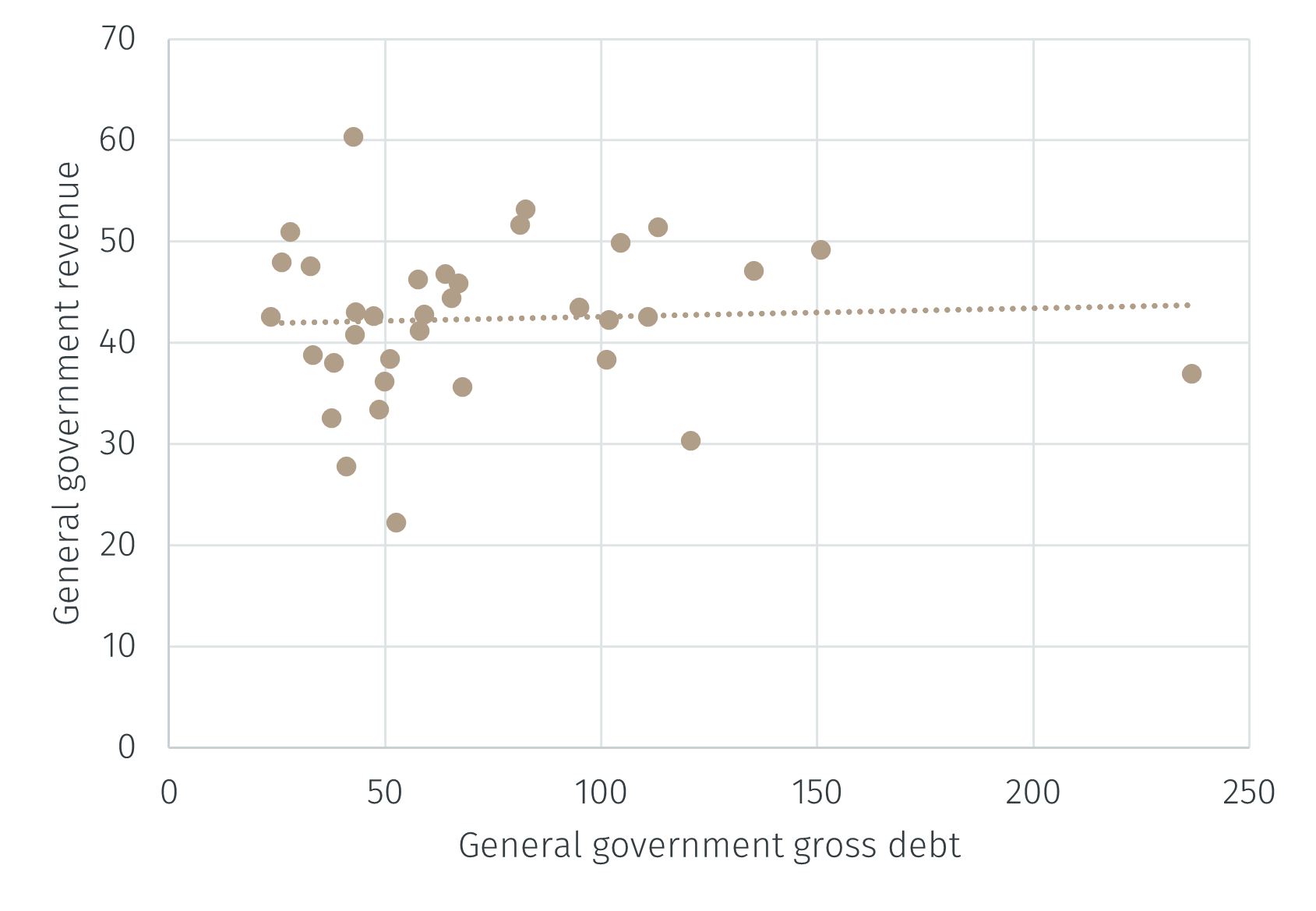

Concerns about public debt and fiscal sustainability are mounting across many advanced economies. In part, this reflects the fact that debt levels are already high relative to GDP, limiting fiscal space and raising questions about long-term debt dynamics.

In the US, these concerns are exacerbated by the economic policies pursued under the Trump administration. The so-called “Big Beautiful Bill” is widely expected to drive a significant increase in the federal deficit and, over time, in public debt. The combination of tax cuts and increased spending may set the US on a fiscal trajectory that is difficult to reverse without politically costly tax increases or expenditure cuts.

In Europe, the fiscal outlook is similarly under pressure, though for different reasons. In response to heightened geopolitical risks and NATO commitments, many European governments are planning substantial increases in defence spending. Projections suggest that military expenditure could rise to around 5% of GDP in some countries, a level not seen in decades. This raises questions about whether already cash-strapped governments will be able to finance these commitments without incurring additional debt.

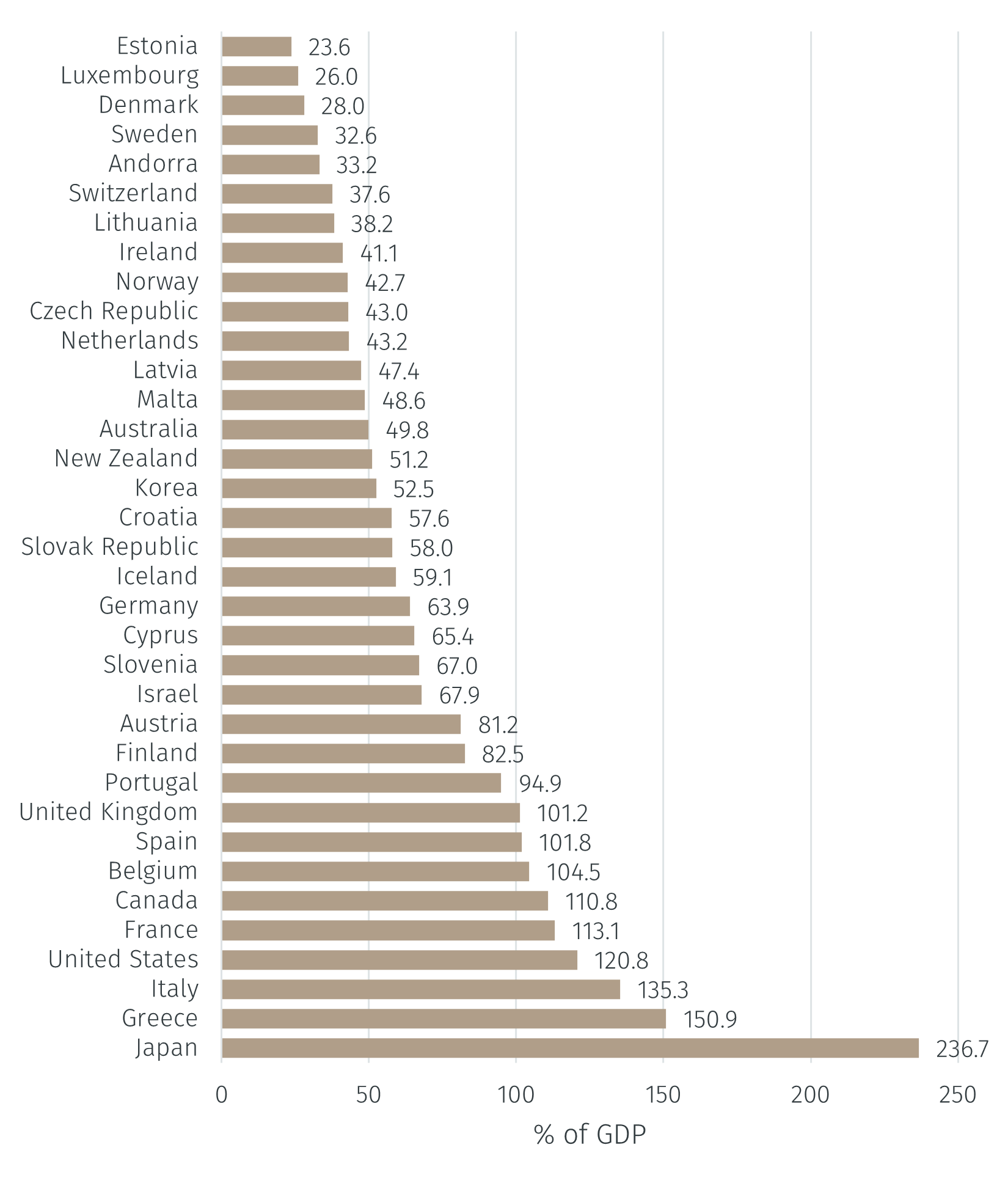

The chart below illustrates just how large public debt stocks are in some economies - and how small they are in others. For instance, public debt in Estonia stands at just 24% of GDP. In contrast, in Japan it exceeds 240%.