As expected, the ECB's Governing Council (GC) left the deposit facility rate (DFR) unchanged at 2%. President Lagarde stated that the GC will evaluate the data "meeting-by-meeting" and does not "pre-commit" to a rate path, which can be characterised as a wait-and-see mode.1 However, the new macroeconomic projections highlight a reduction in downside risks to price stability, limiting the scope for lower interest rates in the coming months.

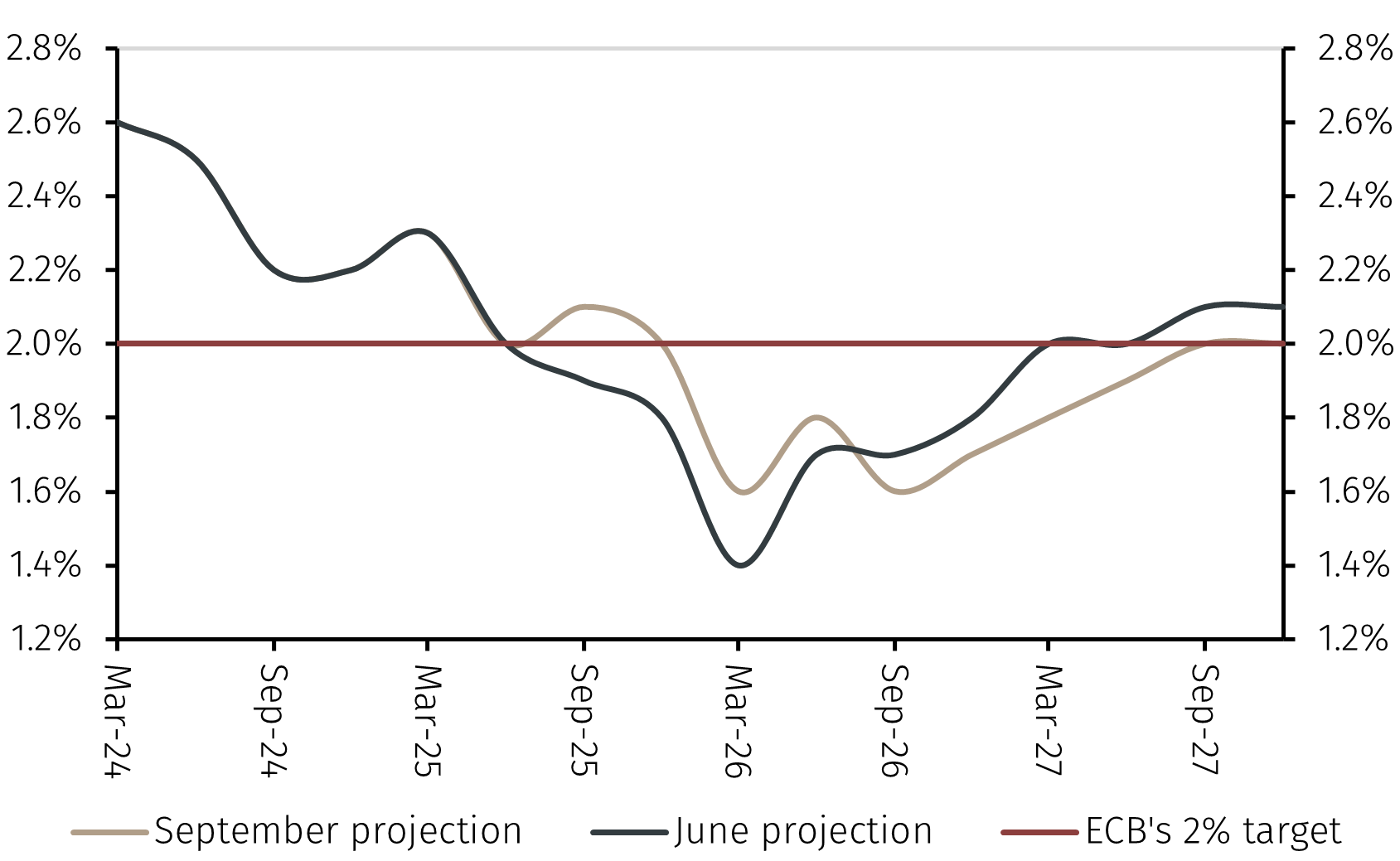

The new ECB staff projection for inflation sees a less pronounced decline the coming quarters despite low energy prices and a strong euro (see Chart 1). However, these factors are expected to lower inflation in the final part of the projection that now sees it returning to the ECB’s 2% target only in late 2027.