Global economic and policy trends

1. The global economy remains resilient despite headwinds – Correct

We anticipated that the global economy would remain resilient in 2025 despite three headwinds. Two of these headwinds are structural in nature and remain prevalent: continued problems in China (the housing market, high private and public debt levels) and high government debt and deficits.

Attention in H1 has been firmly on the third headwind: trade disruption. It has manifested itself in a somewhat chaotic fashion. US tariffs have been announced, imposed, extended and suspended before being judged unlawful. The final outcome is still uncertain and such uncertainty, in itself, is a drag on growth.

The brief period of extremely high tariffs on China (145%) effectively brought US-China trade to a temporary halt. This will have an adverse effect – because of lags in deliveries by sea – on US growth in the second and third quarters. Even so, we expect a recession to be avoided.

The upside of the US tariff disruption is that it has galvanised global action to strike broader trade deals. The trade deals the UK has struck with the US, Europe and India are key examples.

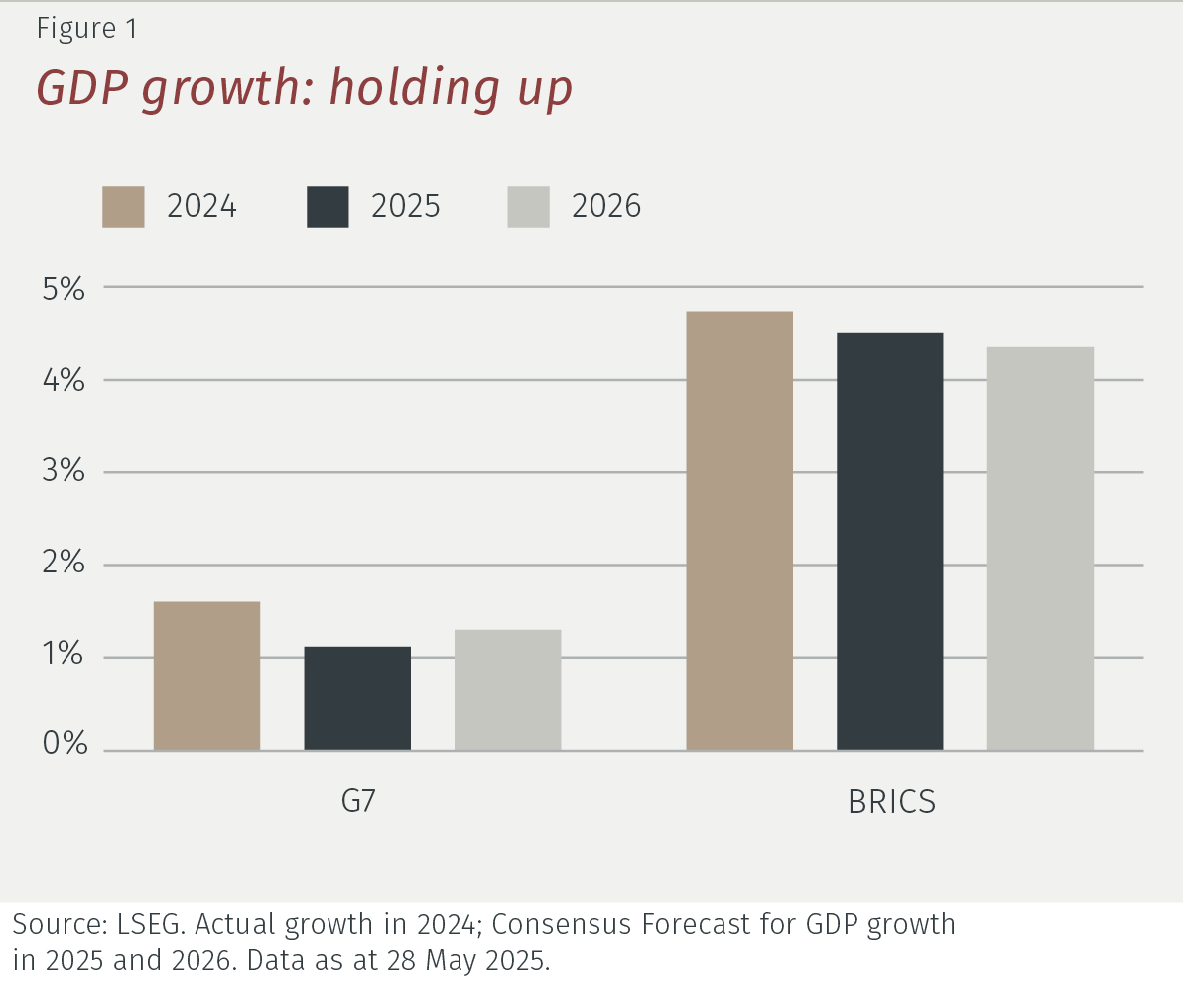

As these new trade deals are negotiated, we see uncertainties around growth easing in the second half of the year and into 2026. Overall global growth will, we think, remain positive and only slightly more subdued than in 2024 (see Figure 1).