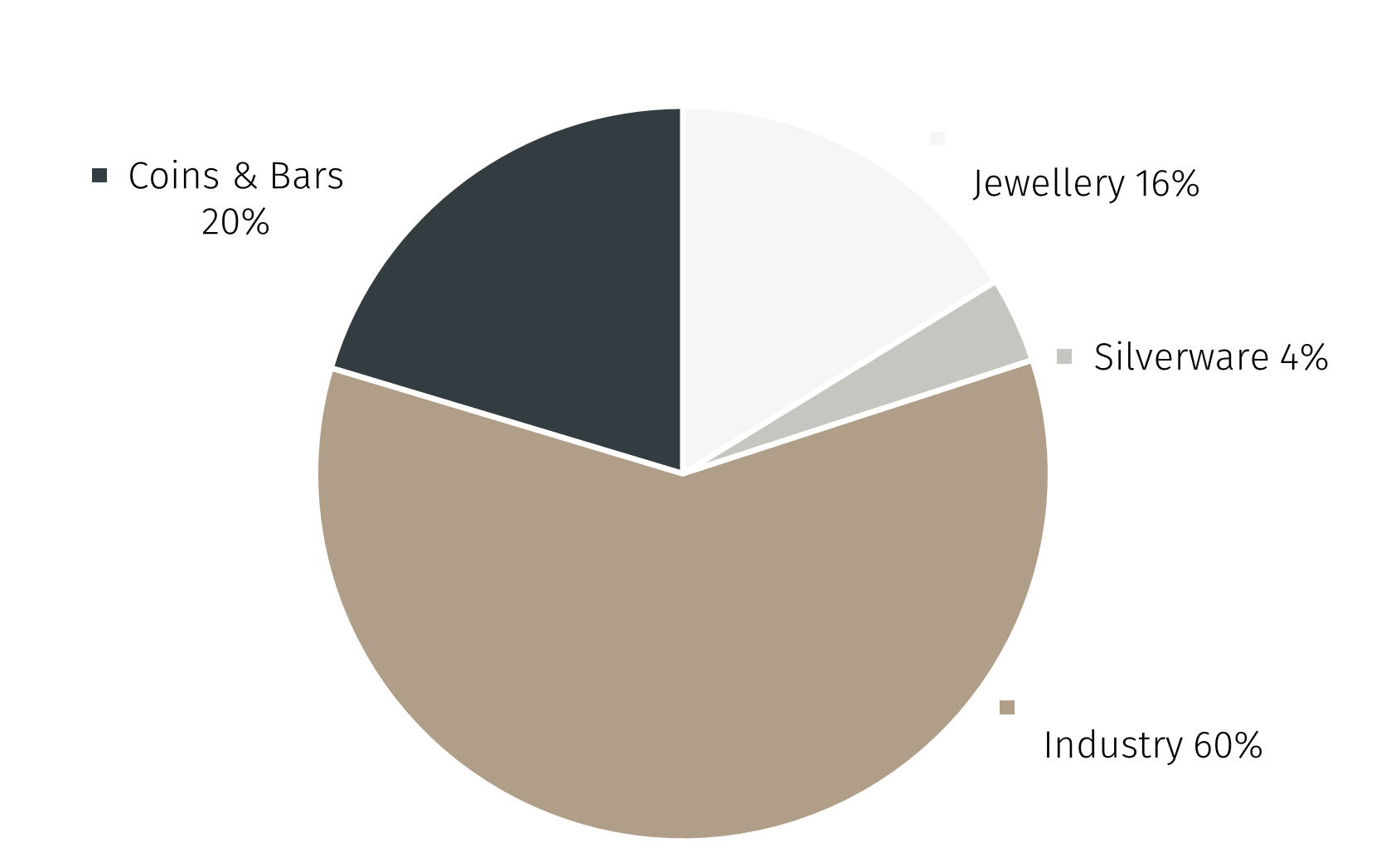

Physical supply, by contrast, has fallen since 2016. This reflects the fact that around 80% of mined silver is a byproduct of mining of other industrial metals. Thus, even a sharp rise in silver prices does not translate into higher output unless base metal production also increases.

Several studies suggest that, without targeted policy action, the shortage of silver will persist for the rest of the decade and possibly beyond.1

Geopolitics and trade restrictions

Geopolitics has added further support to silver prices. Amid renewed trade tensions, in late October China, which accounts for roughly 70% of global silver refining and is the largest exporter, announced strict export restrictions from 1 January 2026.2 The aim is to safeguard domestic technology supply chains and support leadership in solar and battery manufacturing.

In November 2025, the US had designated silver a strategic and critical mineral under the USGS Critical Minerals List.3 This status enables federal subsidies for domestic production and the creation of strategic stockpiles.

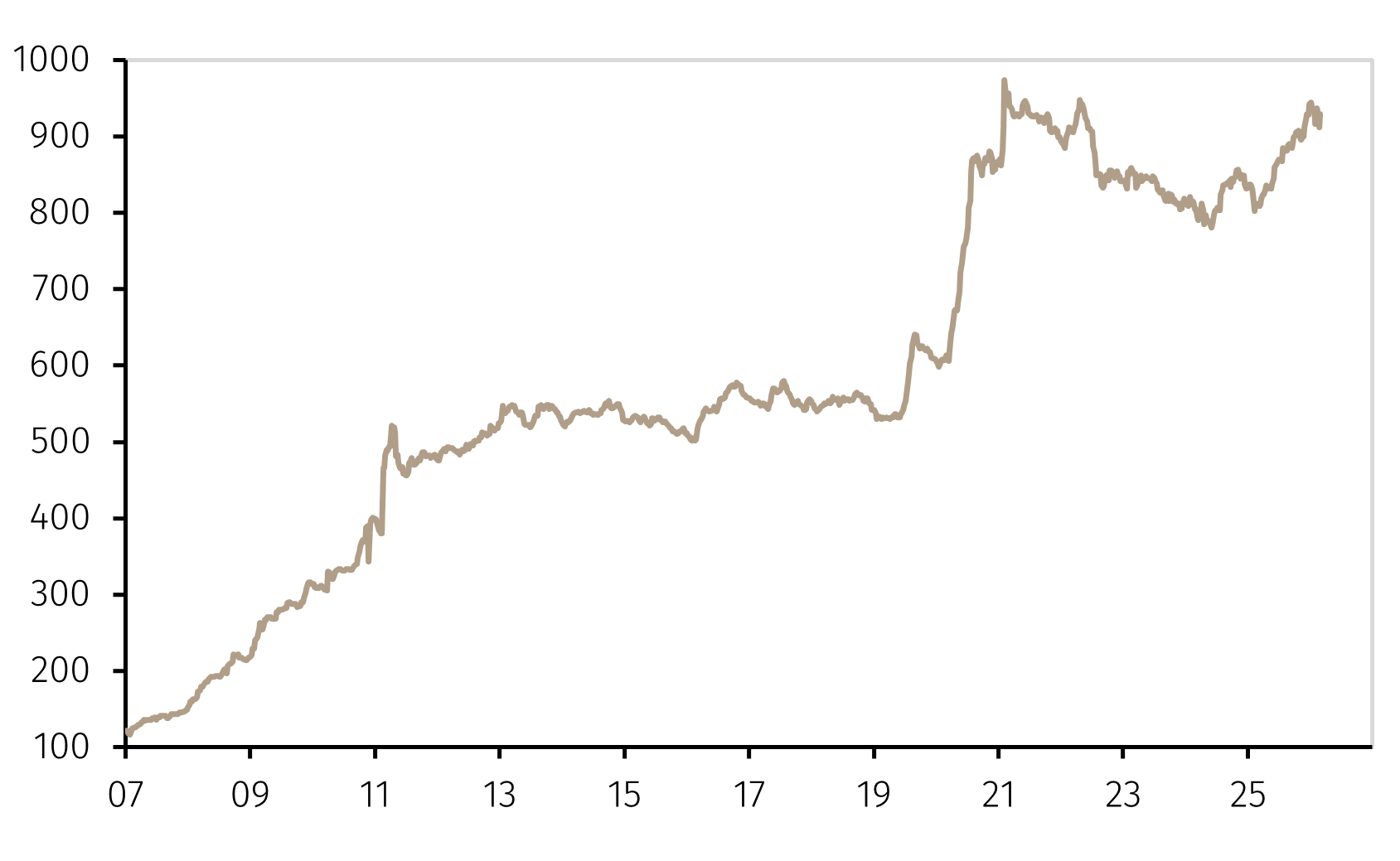

Rising investor interest

Central banks have traditionally focused on gold, largely ignoring silver. That changed between 2025 and 2026, when some emerging market central banks, including Russia, India and Saudi Arabia, began adding silver to their official reserves.4 This shift reflects both a desire to diversify away from the US dollar and silver’s hybrid character: a precious metal and a strategic industrial input.

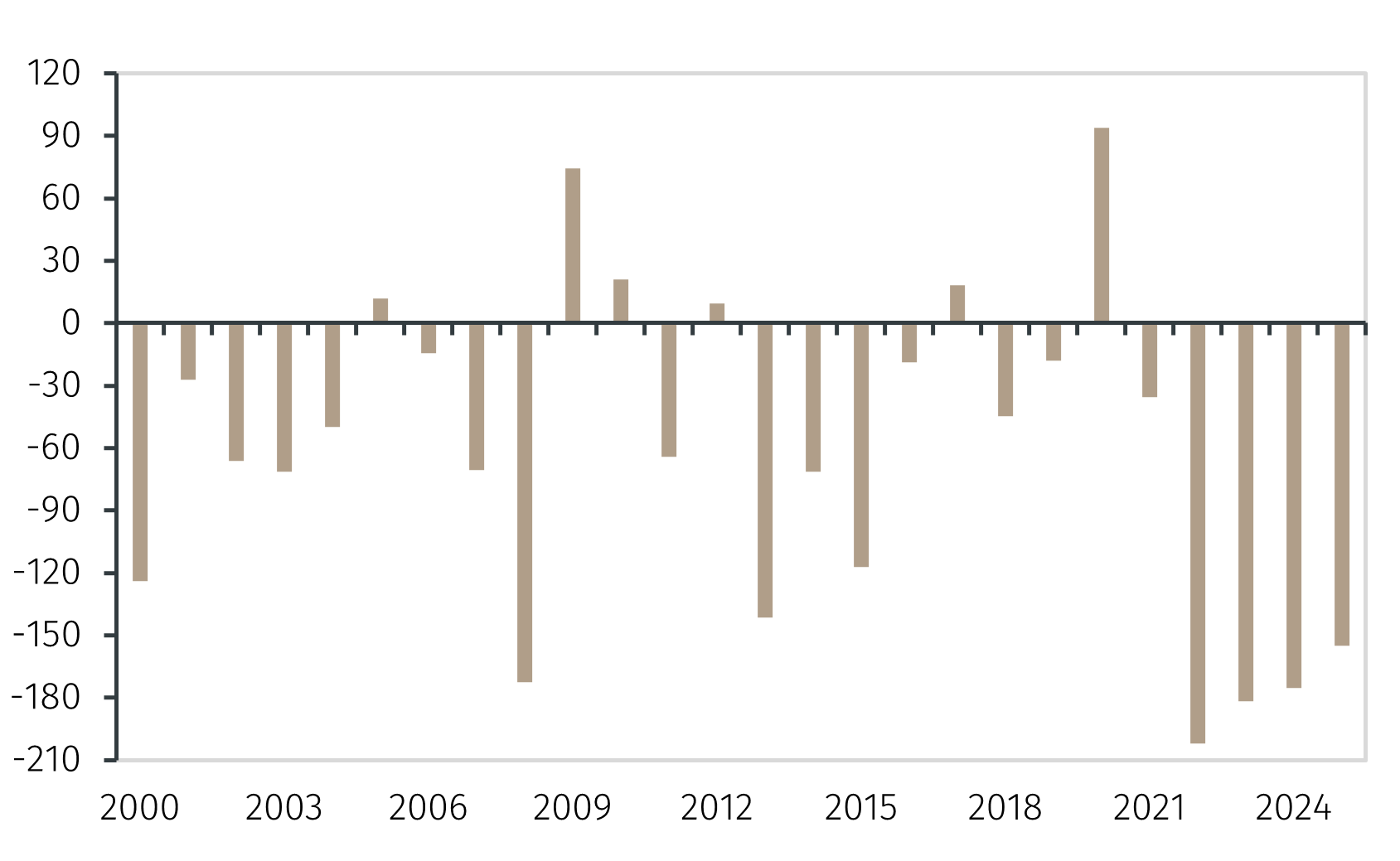

Finally, private investors’ interest in silver has increased further, as shown by the rise in total ETF holdings (see Chart 5). Absorbing additional supply, institutional and private investors’ demand reinforced the upward pressure on prices.