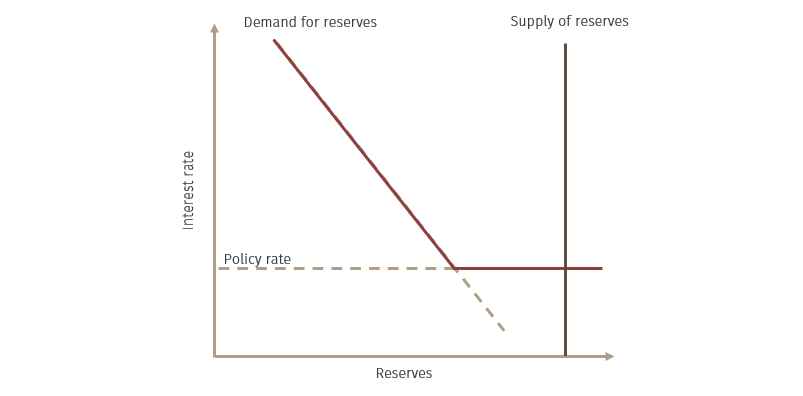

One possible operating regime is for the central bank to supply reserves in ample quantity so that money market rates are equal to the policy rate. From the perspective of interest rate control, this outcome appears attractive. However, when reserves are abundant, banks have little incentive to engage in interbank borrowing and lending. Instead, they transact primarily with the central bank.

SARON and the importance of interbank trading

This is problematic in Switzerland because the reference rate, SARON, is based on actual transactions in the secured interbank market. If trading volumes are very low, the information content of the rate deteriorates, making it harder for the SNB to assess liquidity conditions and weakening the signalling role of money market prices. An operational framework that delivers the “right” rate but eliminates trading is therefore not desirable.

To address this issue while continuing to operate with abundant reserves, the SNB uses a system of tiered remuneration. Each bank is assigned an exemption threshold. Sight deposits held at the SNB up to that threshold are remunerated at the policy rate, while deposits above the threshold earn a lower rate. For domestic banks, the threshold is linked to reserve requirements and is set as a multiple of average minimum reserve holdings.

How tiering supports market activity

This system creates incentives for banks to trade liquidity with one another. Banks are uncertain about their end of day reserve position and about whether they will end up above or below their exemption threshold. A bank that expects to exceed its threshold has an incentive to lend reserves in the interbank market, since excess balances would otherwise earn the lower rate. A bank that expects to fall short has an incentive to borrow reserves and deposit them at the SNB at the policy rate. Interbank trading therefore takes place at interest rates between the two remuneration levels.

Tiering alone does not determine where interbank rates settle. That depends on how abundant the supply of reserves is relative to banks’ demand for them. If reserves are too plentiful, a large share earns the lower rate, and interbank trading would push SARON towards that level rather than towards the policy rate. To avoid this, the SNB actively limits the supply of reserves through reverse repos and SNB Bills. This keeps SARON close to, though slightly below, the policy rate even when the policy rate is zero.

Design, not just implementation is central

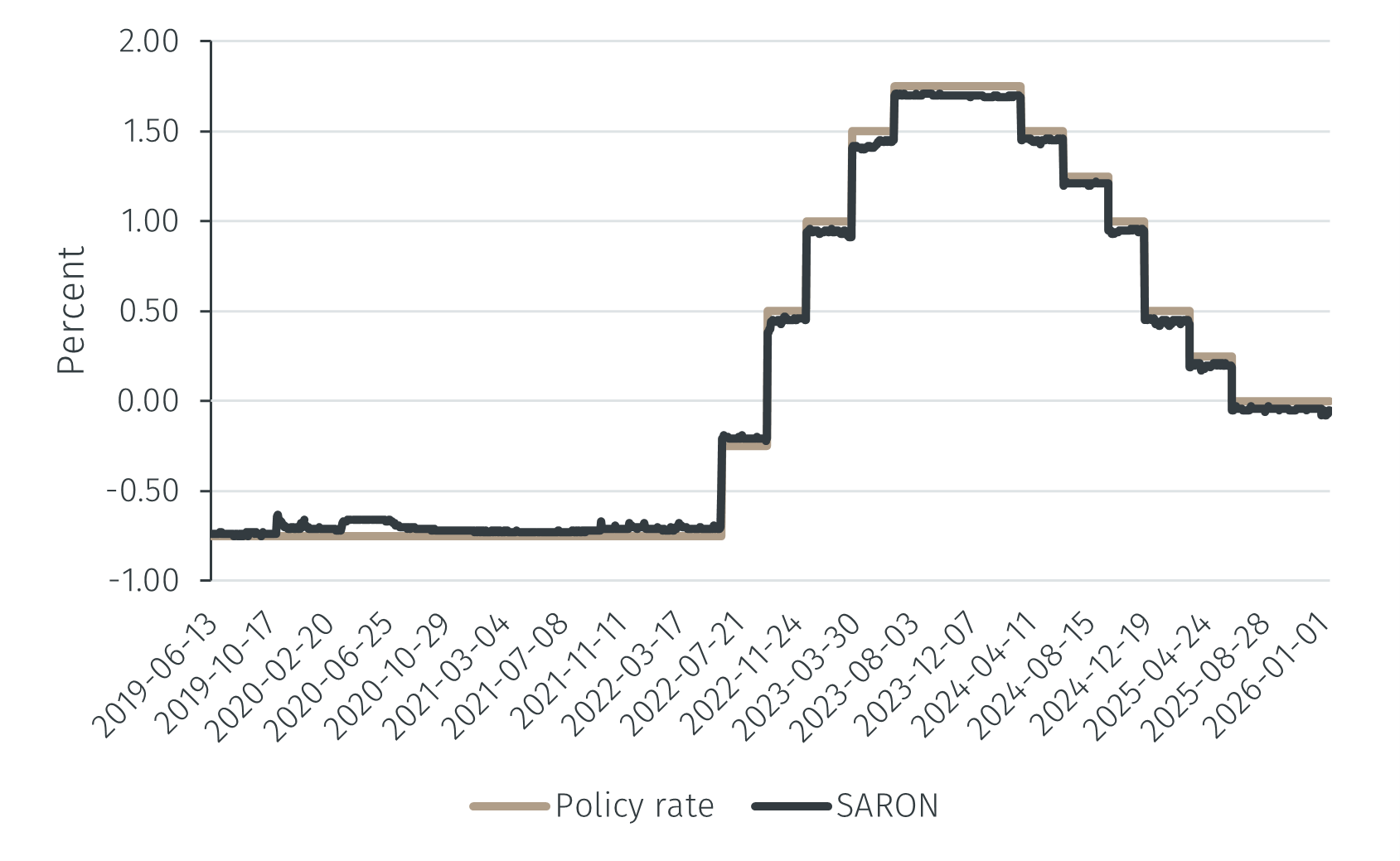

Overall, and as shown in the graph below, the SNB’s operating framework has kept SARON very close to the policy rate. Since 2019, the gap between the two rates has generally been around 4–5 basis points, even as the policy rate moved from deeply negative levels to positive territory and, more recently, back to zero. This consistency across very different interest rate settings illustrates how effectively the SNB translates its policy decisions into money market outcomes.

The broader point is that monetary policy affects the economy only through its transmission to market interest rates. In Switzerland, that transmission hinges on operational choices that are rarely discussed. Central banking is therefore not only about setting rates, but about designing the operational framework that makes those rates effective.