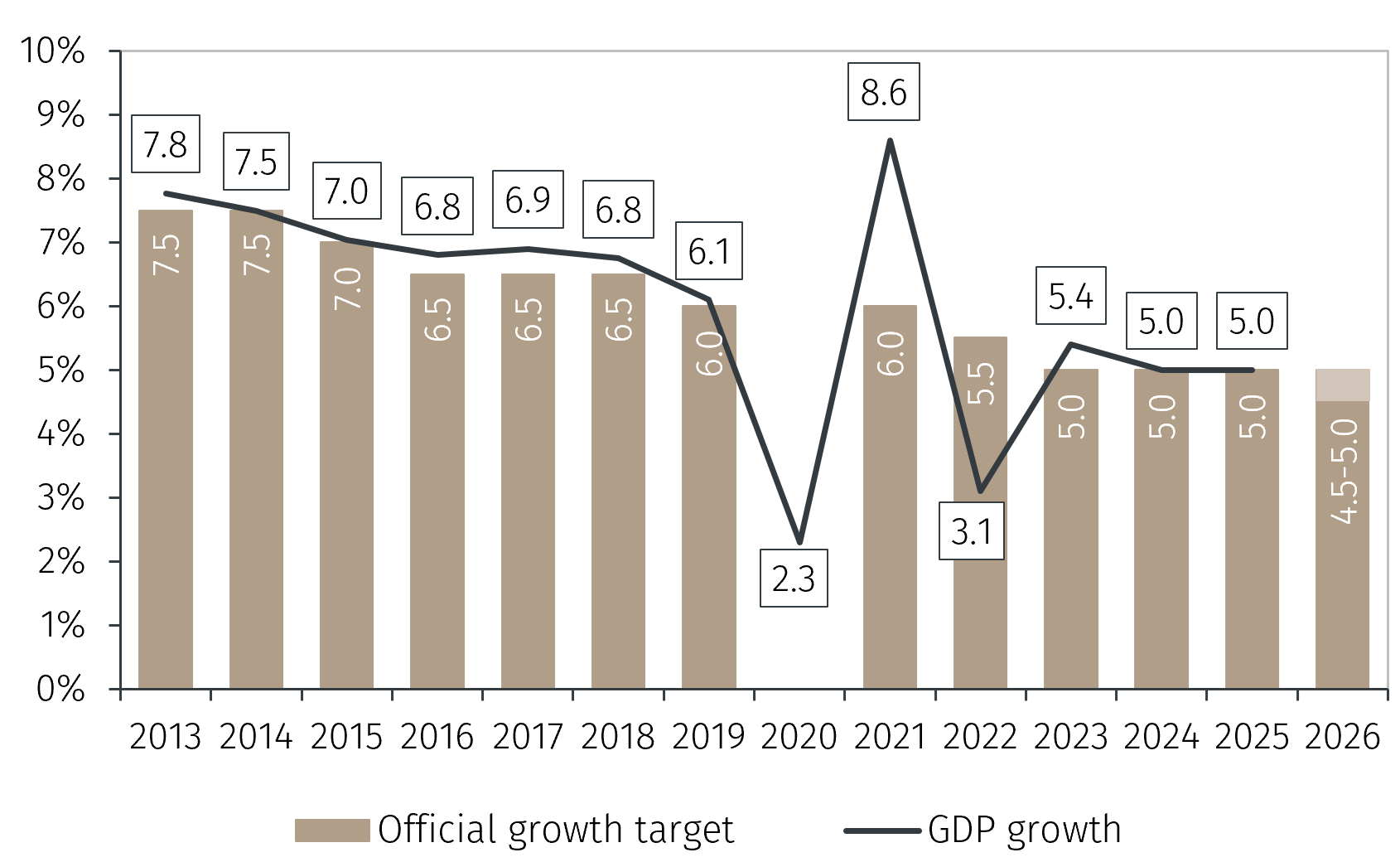

Nonetheless, the moderation in the growth target is marginal. What is more important is the signal that it provides. It highlights that Beijing is more focused on shoring up its balance sheet this year than pursuing short-term growth. This was evident by the fact the budget deficit target was set at 4% of GDP, unchanged from 2025.

Subdued stimulus measures

In addition, there will be RMB 1.3 trillion of ultra-long special treasury bonds and RMB 4.4 trillion of local government special bonds issued this year. These are bonds that the government issues “to consolidate growth momentum from a long-term perspective” and they are typically used to fund infrastructure projects.2 The level of issuance in 2026 is unchanged from 2025 in nominal terms, meaning that it is likely to represent a decline as a share of GDP.3

We previously wrote a Macro Flash Note discussing the drivers of GDP growth in China in 2025 and the outlook for 2026.4 The consumer trade-in program was outlined as an important tool in stimulating domestic demand last year. It is therefore underwhelming that RMB 250 billion of the RMB 1.3 trillion ultra-long special treasury bonds will be used to fund this scheme. This is below the RMB 300 billion that was used for the scheme in 2025 and implies there will be less support for consumer demand this year.

These announcements imply China’s government is focused on managing its balance sheet over stimulating domestic demand. Nonetheless, Beijing could announce a new round of stimulus later in the year. Typically this would happen in October or November. However, this is only likely if China’s economy is not on track to meet the growth target, which seems unlikely given that target is relatively unambitious.

All eyes on AI

In addition to the Government Work Report, the National People’s Congress also deliberated on the 2026-2030 Five-Year Plan. The most notable element of this was that the top priority was “Pursuing high-quality development”. In practice, this was all about artificial intelligence (AI), and was the first time AI had its own section in the Five-Year Plan. While no specific details were given in terms of government investment and policies, there were pledges to expand financing channels and build high-quality datasets to train AI models. This highlights the importance Beijing places on leveraging the potential of AI for China’s economy in the coming years, as discussed in EFG’s Outlook 2026.5

In summary, the National People’s Congress painted the picture of a subdued outlook for GDP growth in 2026 as China’s economy matures and the government prioritises sensible fiscal policy over short-term growth. The focus of the next five years for Beijing will undoubtedly be on how to harness AI’s potential and interweave it with the traditional drivers of growth. We have a positive view on China and Hong Kong equities but prefer to focus on Hong Kong given the relatively larger technology weight in the index and the subdued outlook for the domestic economy in China.