The end of exceptional tightness

The December Job Openings and Labor Turnover Survey (JOLTS) report adds to the growing body of evidence that the US labour market is losing momentum. While the monthly data are volatile, the broader message across job openings, hiring, and worker turnover is increasingly consistent. Labour demand is easing, and the exceptional tightness seen in 2021–22 has largely unwound.

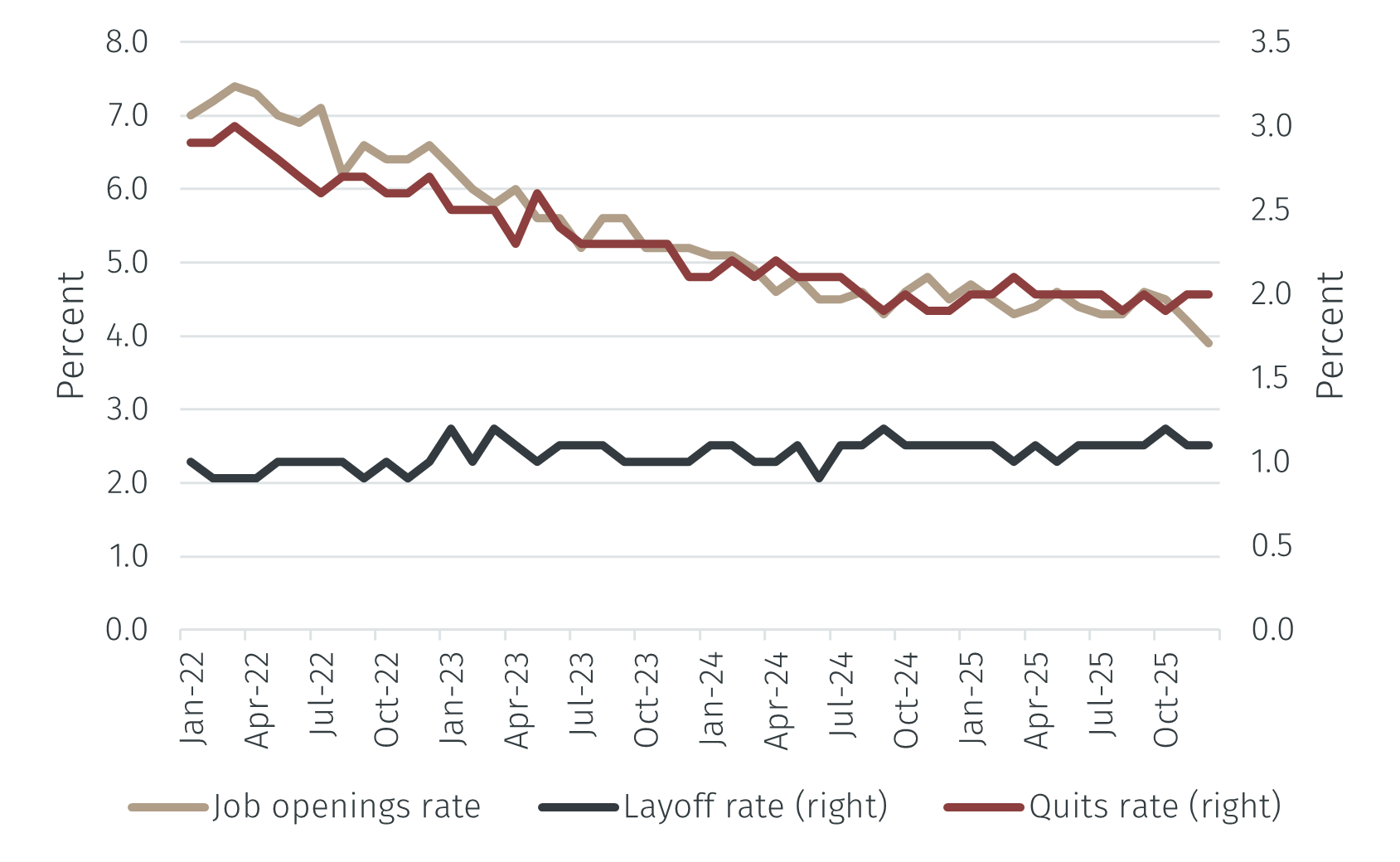

The headline surprise was the further decline in job openings. Vacancies fell by 386,000 in December to 6.5 million, well below market expectations. At 3.9%, the job openings rate is now close to pre-pandemic norms and far below the peak of 4.6% reached last autumn.

Subdued hiring and low quits rates

Other components of the report reinforce this picture. Hiring remains subdued at 5.3 million, with the hiring rate stuck at 3.3%, a level last seen during the slow recovery following the global financial crisis. That firms are neither hiring aggressively nor shedding workers points to a labour market that is cooling primarily through weaker labour demand rather than outright job losses.

The quits rate provides further confirmation. Quits, which are best seen as an indicator of worker confidence and bargaining power, were unchanged at 2.0% in December. This is well below the roughly 3% rates seen in early 2022, when workers were rapidly switching jobs amid strong wage growth. Today, there are fewer than one job openings per unemployed worker, compared with around two at the peak. This shift is consistent with easing wage pressures and suggests that nominal wage growth is likely to slow further over the course of the year.