Unlike most central banks, the Fed has a dual mandate: to ensure price stability and to promote maximum employment. While many central banks also consider both inflation and economic activity, the Fed is unusual in that it assigns these goals equal importance.

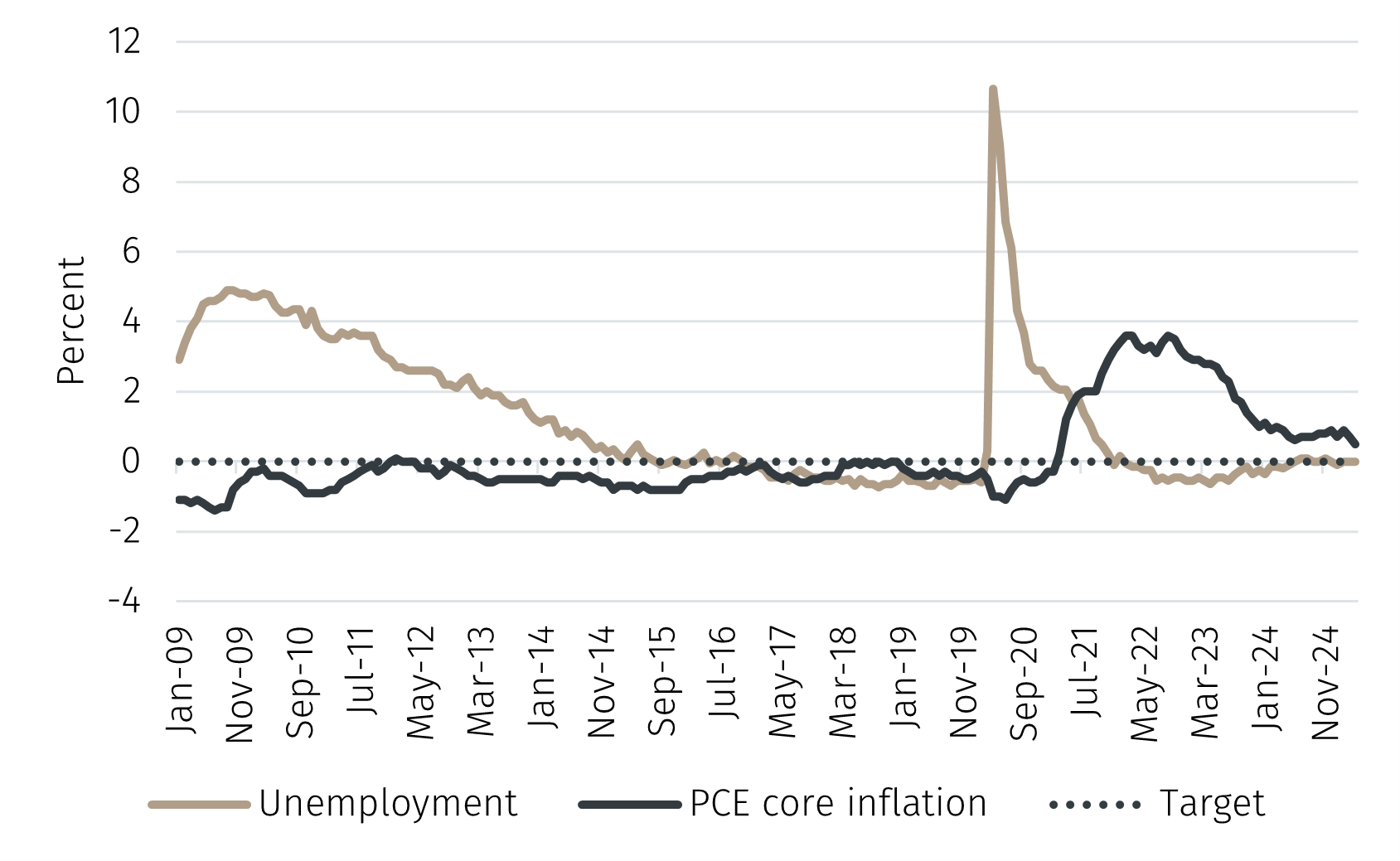

In practice, the Fed is often interpreted as seeking to minimise the squared deviation of core personal consumption expenditure (PCE) inflation from a 2% target and the squared deviation of unemployment from a “normal” level. This benchmark is typically taken to be the median of Federal Open Market Committee participants’ longer-run projections, most recently 4.2%. This “target” varies over time and is available quarterly since 2009Q1.1

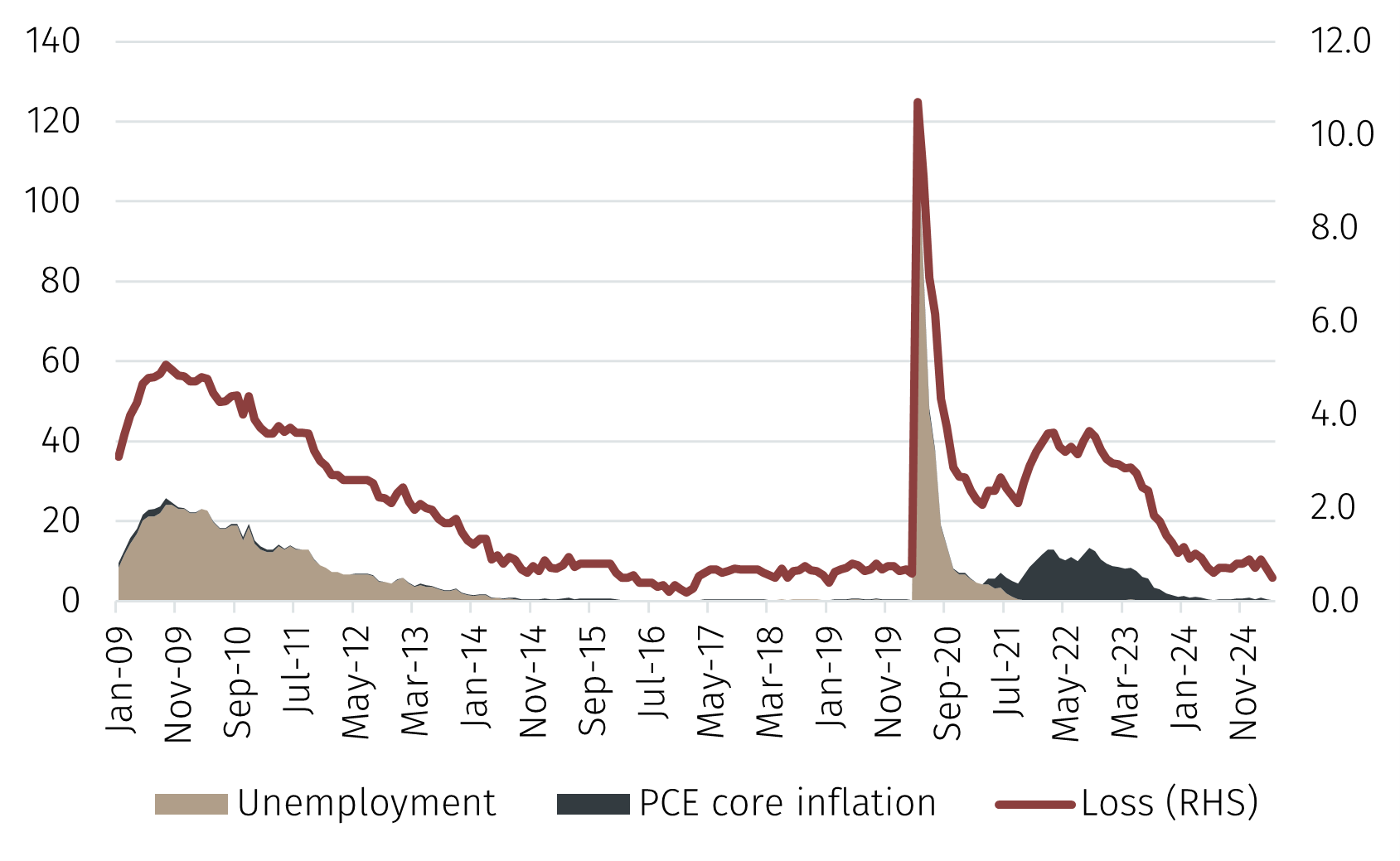

Formally, the Fed’s objective can be written as minimising a “loss function” of the form:

{(inflation rate – 2%)² + (unemployment rate – 4.2%)²} ¹ᐟ²

This loss function defines the hypotenuse of a “policy triangle,” which captures how far the Fed is from meeting its dual mandate. The smaller the hypotenuse, the better the Fed’s performance. Thus, this loss function provides a simple but powerful way to frame the trade-offs involved in monetary policy.

The graph below shows the deviations of unemployment target and core PCE inflation from 2% since 2009. Historically, the most important source of losses were spikes in unemployment — though these episodes have differed markedly in severity and duration.