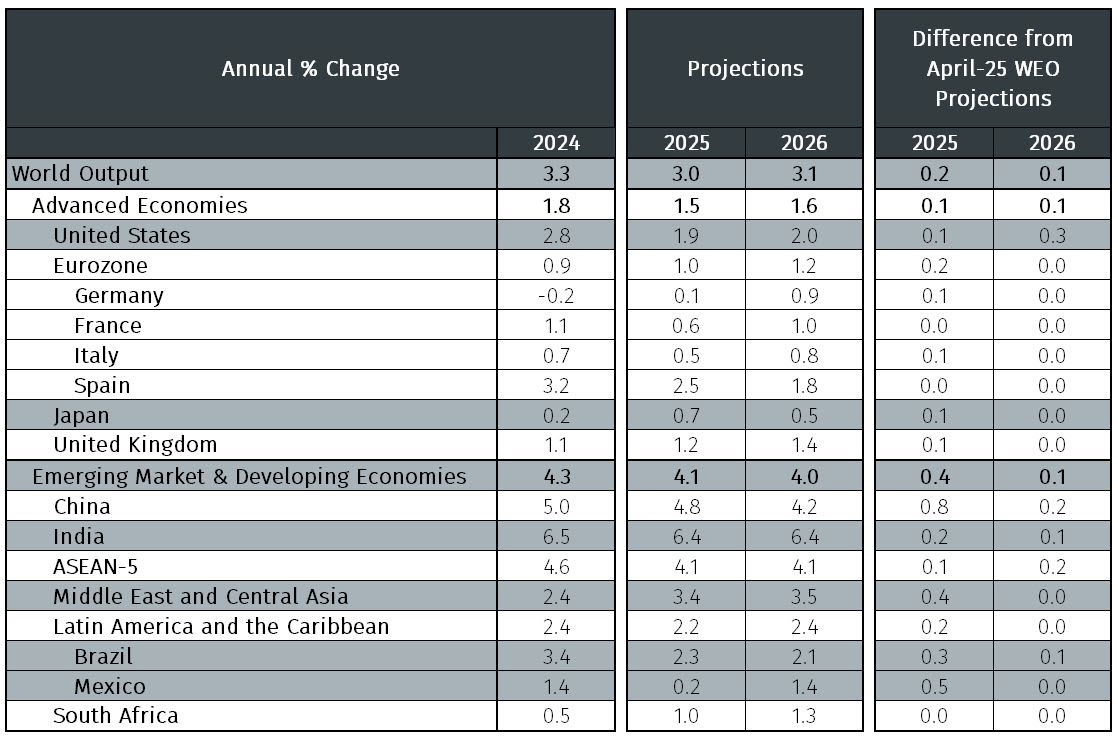

Looking ahead, the IMF expects global growth to slow. Despite the upward revisions to global growth projections in relation to April, the forecasts for 2025 and 2026 remain below the 3.3% achieved in 2024 and the pre-pandemic historical average of 3.7%.

In advanced economies, growth is forecast at 1.5% in 2025 and 1.6% in 2026. In the euro area, growth was revised upward to 1.0% in 2025 and 1.2% in 2026. Although it represents less than 5% of total euro area GDP, this revision was driven by Ireland’s strong GDP outturn in the first quarter. The IMF increased its 2025 growth forecast for EM economies from 3.7% to 4.1%. This is mostly due to China, which saw the largest upward revision in the July WEO update, increasing by 0.8 percentage points to 4.8% in 2025.

Moreover, the IMF’s projection for world trade volume has been revised upward by 0.9 percentage points for 2025, but 0.6 percentage points downward for 2026. This further reflects front-loading impacts that are expected to slow down in the medium term.

Risks to the outlook

The IMF views risks to the outlook as tilted downwards, as was the case in the April WEO. Tariffs, front-loading, escalation of geopolitical tensions and fiscal vulnerabilities are highlighted.

The WEO highlights that a rebound in effective tariff rates could lead to weaker global growth. A situation where negotiations breakdown and tariff rates are much higher than they are today could result in an escalation of protectionist measures. Correspondingly, increased levels of uncertainty could weigh more heavily on economic activity, especially if deadlines for additional tariffs expire without substantial or permanent agreements.

The IMF also views the potential inflationary impact of additional tariffs or other non-tariff measures as a downside risk to growth. Here, non-tariff measures targeting critical inputs could lead to dislocations in global supply chains. To defuse trade tensions, the IMF notes that bilateral trade negotiations should address the root cause of trade imbalances that motivated the introduction of tariffs in the first place.

Front-loading has supported economic activity throughout the first half of 2025. However, the IMF points out that this raises the potential for negative shocks to be amplified. For example, firms may face increased holding costs and potential losses from obsolescence.

Furthermore, the IMF notes that if geopolitical tensions escalate, particularly in the Middle East or Ukraine, this will introduce further supply shocks and would likely disrupt global supply chains, pushing commodity prices up. This could also create complex trade-offs for central banks, in an environment where trade is already serving as an underlying challenge.

Lastly, as part of its revised WEO, the IMF highlights risks related to fiscal vulnerabilities in both EM and advanced economies. Several countries, including France and the US, are projected to run large fiscal deficits. This could result in higher term premiums and, in some cases, tighten global financial conditions, leading to lower growth.

On the upside, positive trade negotiations tied with predictable frameworks and tariff declines could support global growth in the view of the IMF. If agreements as such are reached, uncertainty would significantly reduce and foster policy predictability, facilitating investment and other business decisions.

Conclusion

To conclude, the importance of restoring confidence, predictability and sustainability remains a key priority according to the IMF. Pierre-Olivier Gourinchas, Chief Economist at the IMF, noted that “the world economy is still hurting and it’s going to continue hurting with tariffs at that level, even though it’s not as bad as it could have been”.3 Even with slight upward revisions to growth projections, the IMF makes clear that downside risks continue to dominate the outlook.