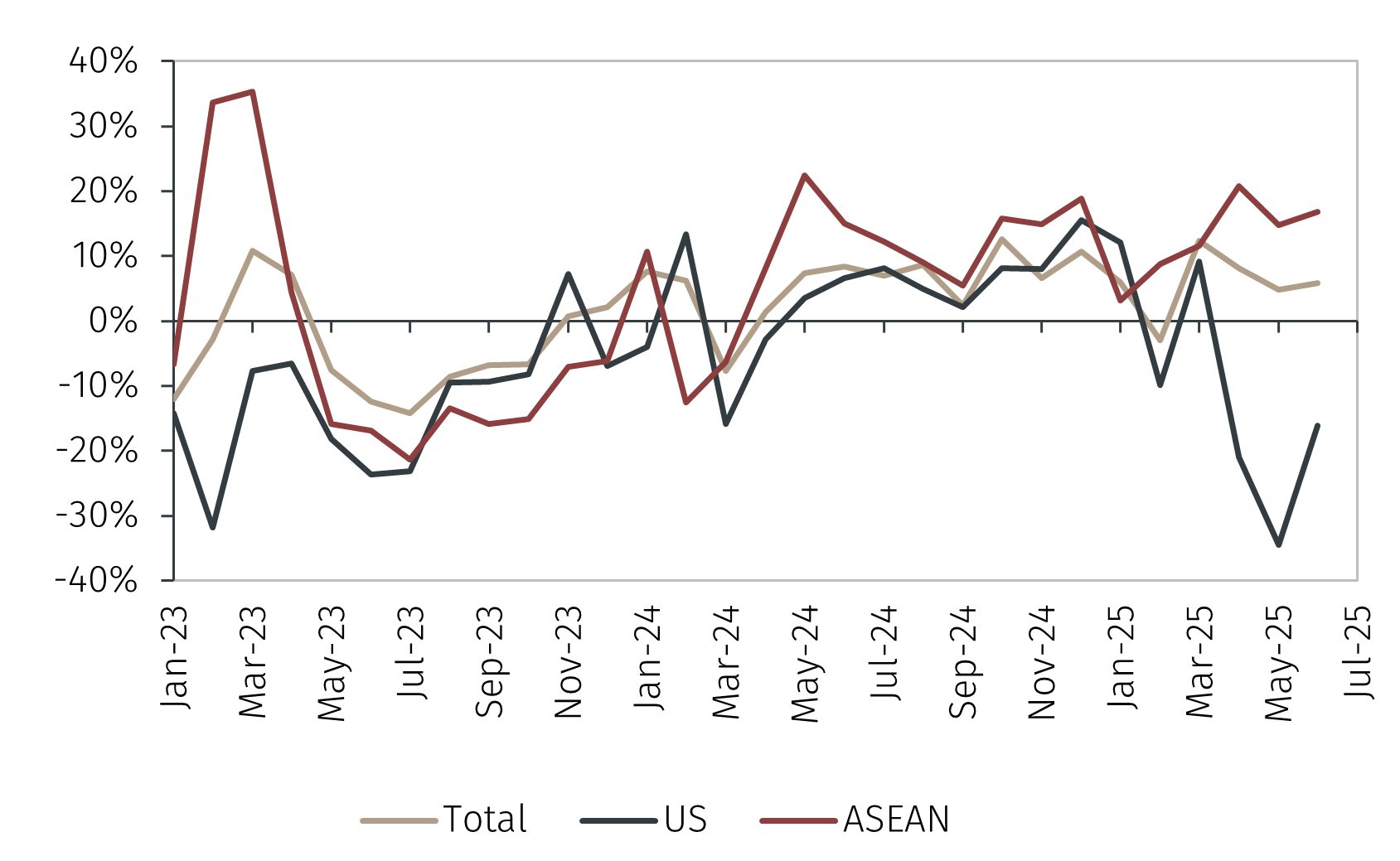

As the higher tariff rate materialised, exports to the US collapsed. However, overall exports remained robust, supported by an increase in exports to Association of Southeast Asian Nations (ASEAN) countries. This could reflect transshipment of Chinese goods via ASEAN countries to the US to avoid higher tariff rates.

However, as was the case with retail sales, this calls into question the sustainability of export growth at the levels seen in H1. This is due to the fact that the US is implementing measures to prevent transshipment of Chinese goods via ASEAN countries. The most prominent piece of evidence to date is the US’s trade agreement with Vietnam on 02 July. The US agreed to impose 20% tariffs on Vietnamese goods imported to the US but will impose a higher rate of 40% on goods that pass through Vietnam but originate in a different country.

It will be important to watch for similar terms in any trade deals agreed between the US and other ASEAN countries. If such terms are agreed, China may find it difficult to maintain the growth rate of exports seen in H1.

While consumption and exports are likely to slow in H2, they are unlikely to do so to an extent that means the government’s self-imposed GDP growth target is not achieved. If GDP rose 4.8% in 2025, the government could feasibly claim its target has been met. As such, China’s average growth rate could slow to 4.3% year-on-year in H2 and still be viewed as acceptable by Beijing.

To some extent, this is a double-edged sword. Beijing has been reticent to stimulate the economy more than it deems necessary to ensure the growth target is achieved. Thus, with a target that appears to be easily attainable, there is a lower probability of significant government stimulus in H2.

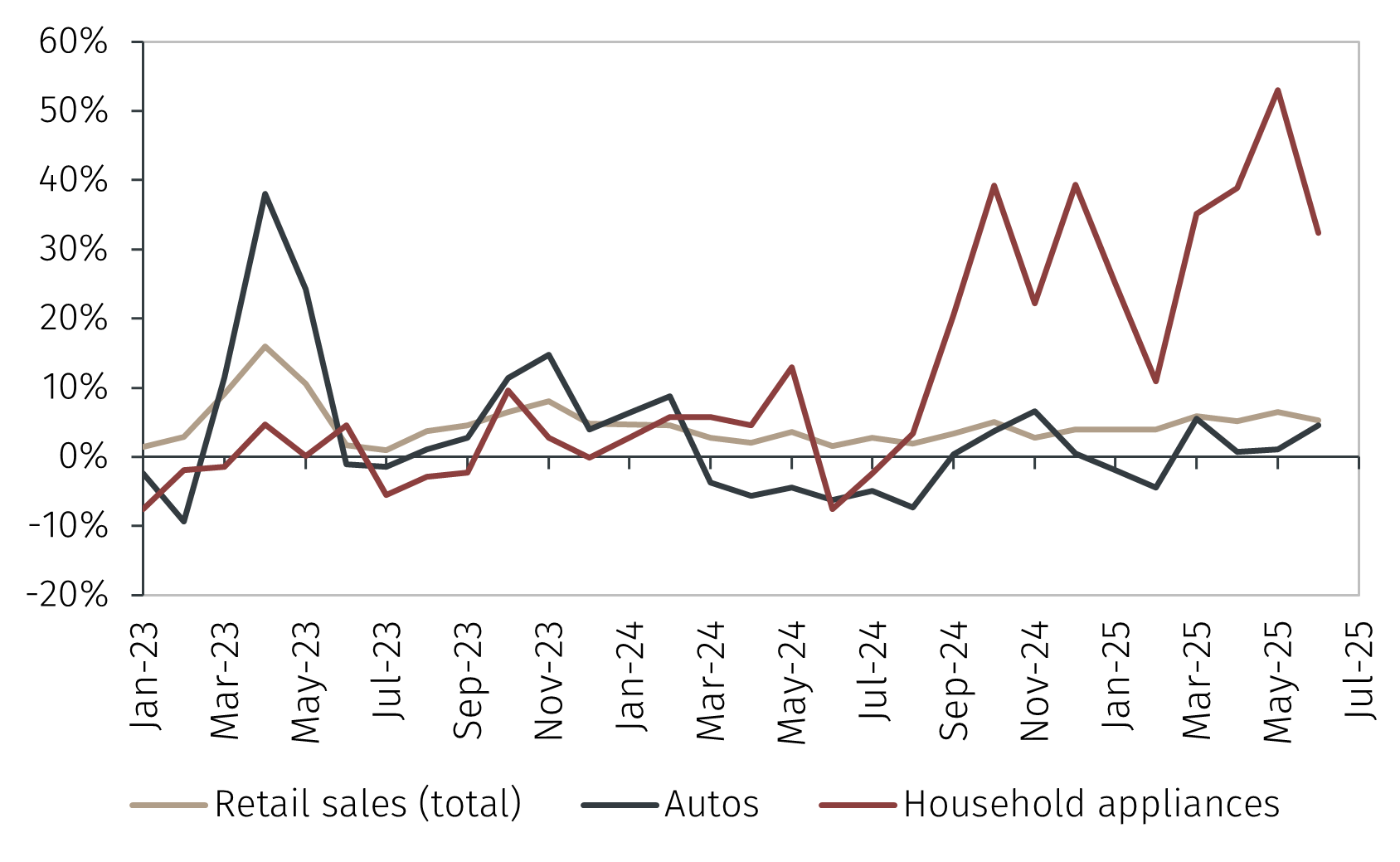

In summary, Chinese GDP growth was strong in H1, reflecting the success of the consumer trade-in program and frontloading/transshipments of exports. It is unlikely that these factors will be able to support the economy to the same extent in H2, meaning growth is likely to fade. Nonetheless, the growth target of “around 5%” appears easily attainable meaning the government is likely to feel less pressure to stimulate the economy, despite weak underlying demand.