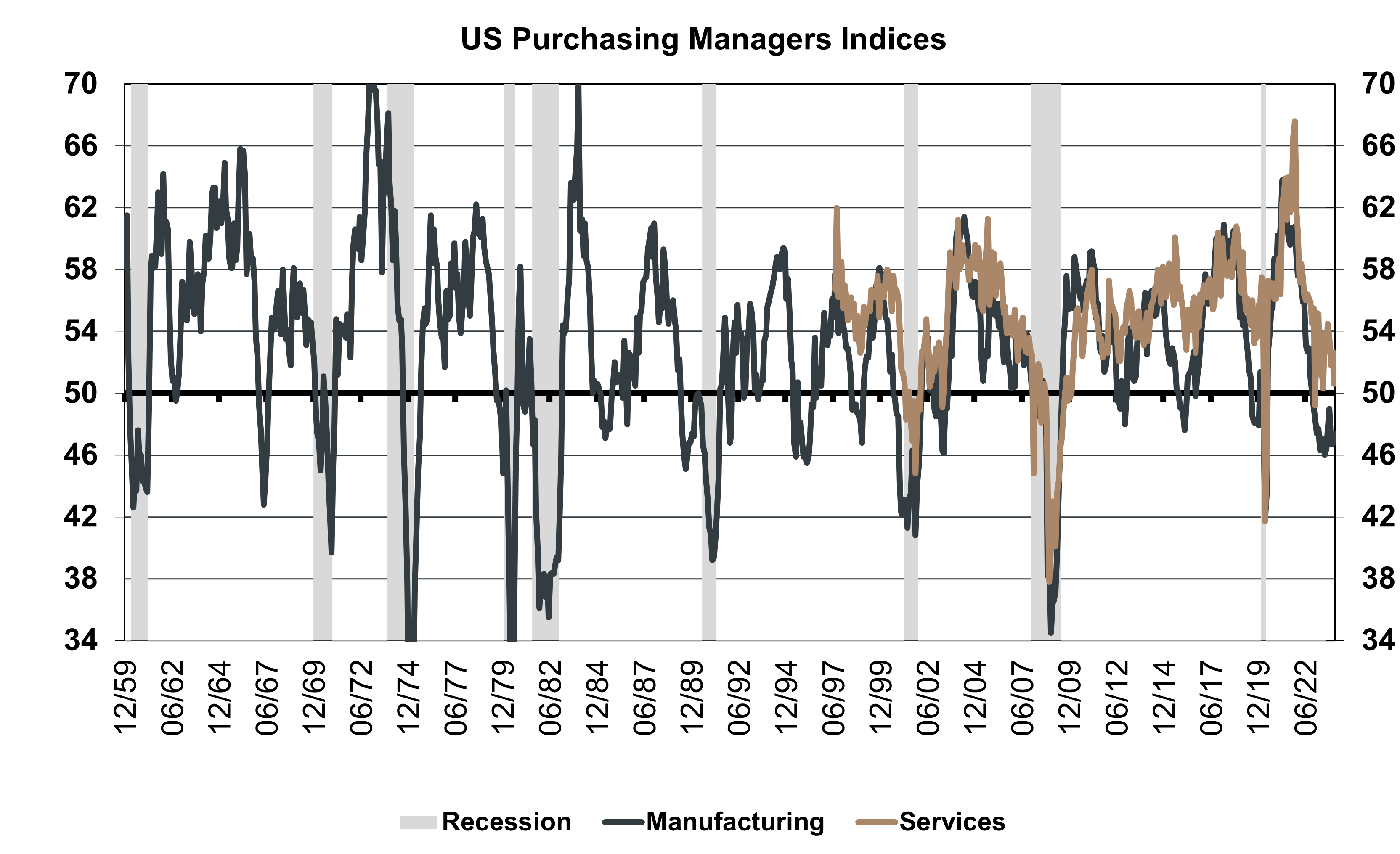

The headline Institute for Supply Management (ISM) Manufacturing Purchasing Managers’ Index (M-PMI) has been below 50 since November 2022, indicating that the sector has been in contraction. The ISM Services PMI® (S-PMI) has remained above 50 over the same period (apart from a brief and subtle dip below in December 2022) although it has been in steady decline over the past four months and is now only just above 50. Whilst PMIs at such levels do not always imply a recession, they are very often associated with one – see Chart 11. Indeed, the ISM’s December report notes that the current level of the Manufacturing PMI® (47.4%) “corresponds to a change of -0.5 percent in real gross domestic product (GDP) on an annualized basis”.

Investment Insights • MFN

2 min read

What regional data tells us about the US economy

Macro-economics, by definition, involves looking at the big picture. However, sometimes the big picture masks shifts in underlying elements that anticipate developments across the economy more broadly. It is therefore important to check for consistency across both the macro data and the component parts. Daniel Murray explores in this Macro Flash Note whether messages from US regional indicators of activity are signalling a different outlook to that implied by the national indicators.

Chart 1. PMIs and Recessions

Source: Institute for Supply Management, National Bureau of Economic Analysis, EFG calculations. Data as at December 2023.

In the current context this is important because expectations are widespread that the US economy will achieve a soft landing and avoid a full-blown recession, in contrast with the PMI data2.

Looking at regional activity indicators adds an extra layer of information about the US economic outlook. It is possible that most of the regional activity indicators are signalling a soft-landing but that the national PMIs are being dragged lower by one or two outlying regions3. If so, that would add credibility to the soft-landing narrative. If, however, the regional activity indicators are all pointing to a worsening of economic conditions, that would call into question the soft-landing call. It would not mean that a recession is inevitable, but it would suggest that the likelihood of one is greater than markets currently believe.

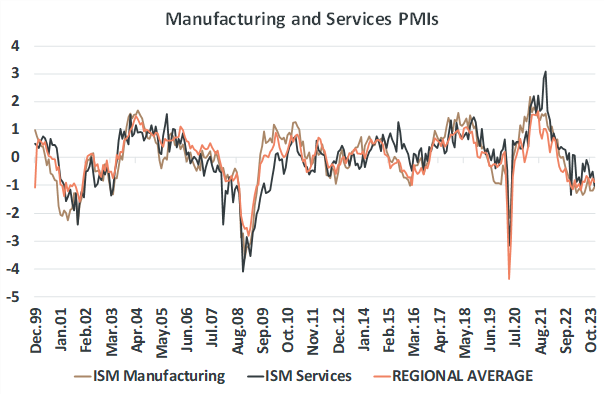

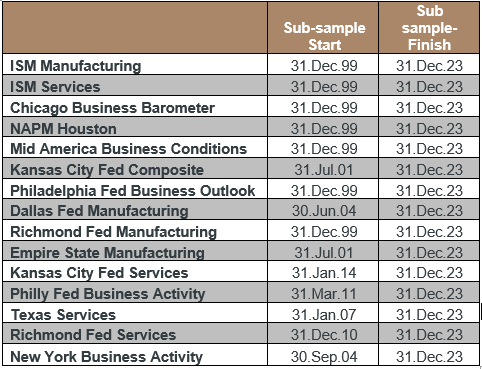

To investigate this, data on 13 different regional indicators of activity were collected for the period beginning in December 1999 and ending in December 2023. Note that data is not available for all indices from the start date. A full list is provided in the Appendix. The indices are produced predominantly by regional Federal Reserve banks (10 out of 13) with 3 produced by local business organisations. To allow for comparability, each index was then normalised and the average of those normalised indices was calculated. The results are shown in Chart 2 together with normalised M-PMI and S-PMI indices.

Chart 2. Average of Regional Activity Indicators and PMIs.

Source: Bloomberg, EFG calculations. Data as December 2023.

The chart shows how the average of the indices mimics well the PMI data. Whilst this is perhaps unsurprising, it is nonetheless reassuring as it shows that the regional average is a good proxy for the national indicators4. It is possible that some regional indicators are more informative about recession risks than others whereas the analysis here assumes that they are all equally important. Full analysis is beyond the scope of this brief note. However, because the simple average of the normalised regional data tracks the national data well, it suggests that there is not persistent undue influence of some regions over others5.

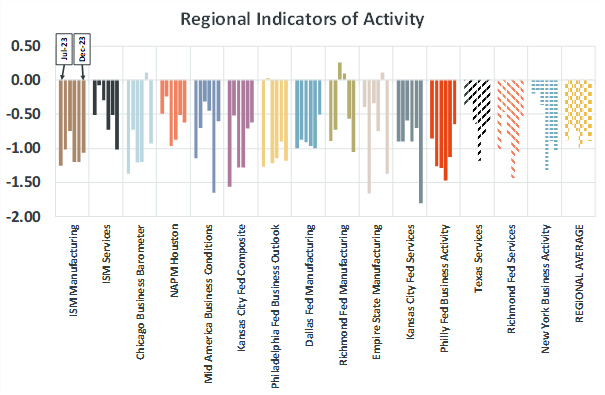

A related point to check is whether the regional average is being distorted by any outliers. For example, if 10 out of the 13 regional indicators were pointing to marginal growth but 3 out of 13 were in sharp contraction territory, that might be sufficient to drag the average into the contraction zone. This is a hard thing to visualise, but Chart 3 is an attempt to do so, showing the evolution of each regional normalised index together with the normalised M-PMI and S-PMI over the past six months.

Chart 3. Evolution of Regional Activity Indicators since July 2023.

Source: Bloomberg, EFG Calculations. Data as at December 2023.

The chart is interesting because it shows that there has been a remarkable degree of consistency across all regional activity indicators. There are some blips, such as the improvement in late Q3 and early Q4 in the Chicago Business Barometer, the Richmond Fed Manufacturing and the Empire State Manufacturing but these look like exceptions that were counter-balanced by worsening data elsewhere, leaving the average firmly in negative territory.

The overriding message is therefore one of greater downside risk to the US economy than currently indicated by consensus expectations. Recessions are always difficult to predict and often surprise markets. Whilst one is certainly not unavoidable, the degree of consistency across the regional indicators suggests that the likelihood of a US recession is elevated and greater than markets are currently pricing, a risk to which we remain highly alert.

Appendix

1 In 2012 and 2015 the M-PMI dipped below 50 but the S-PMI stayed firmly above 50 and recession was avoided. The S-PMI data begins in 1997 but there is a much longer history for the M-PMI. There are several instances in history when the M-PMI fell below 50 but a broad recession was avoided although all recessions have seen the M-PMI below 50.

2 ‘Bloomberg survey data shows that economists are forecasting positive growth in every quarter in 2024.

3 For the sake of clarity, the national PMIs are not aggregations of the regional PMIs; they are produced independently.

4 It would be possible to split out the regional indicators into manufacturing and services. However, there are two problems of doing so: (i) some regional activity indicators cover both manufacturing and services (ii) it would reduce the number of regional indicators in each group.

5 Further work would include weighting the indices by regional GDP or performing a fuller analysis of the influence of each regional index on national GDP.