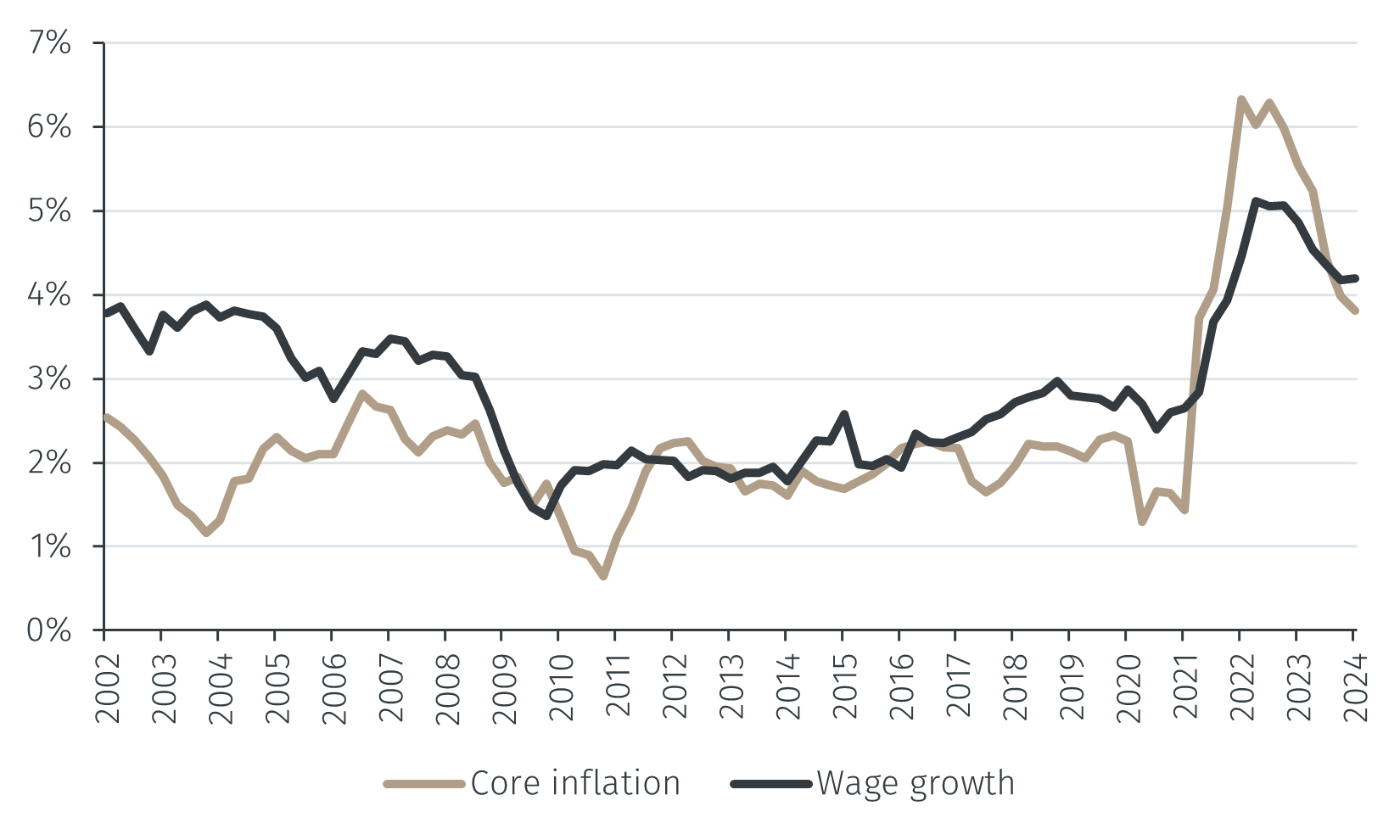

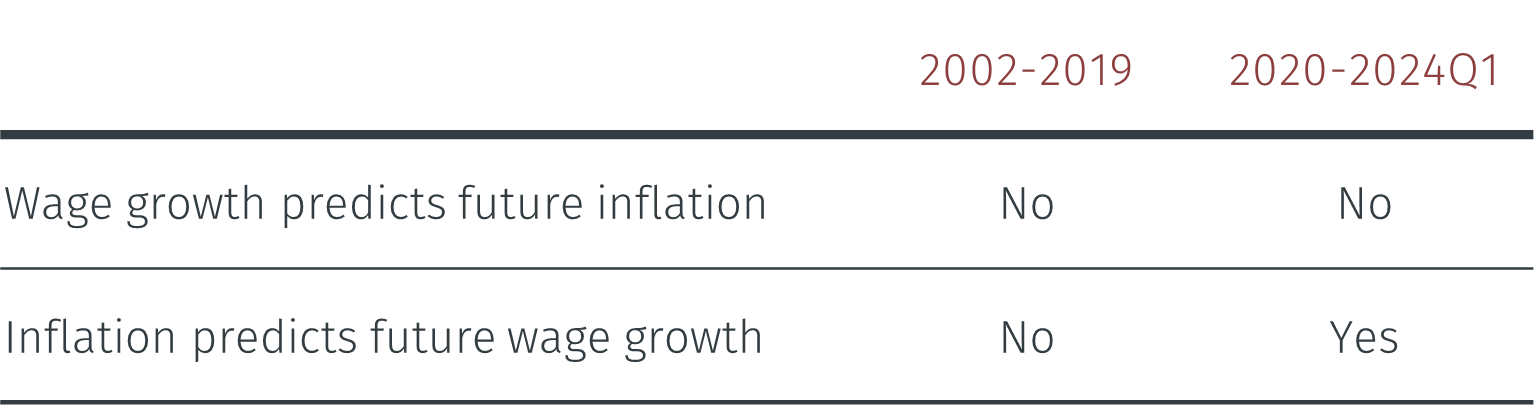

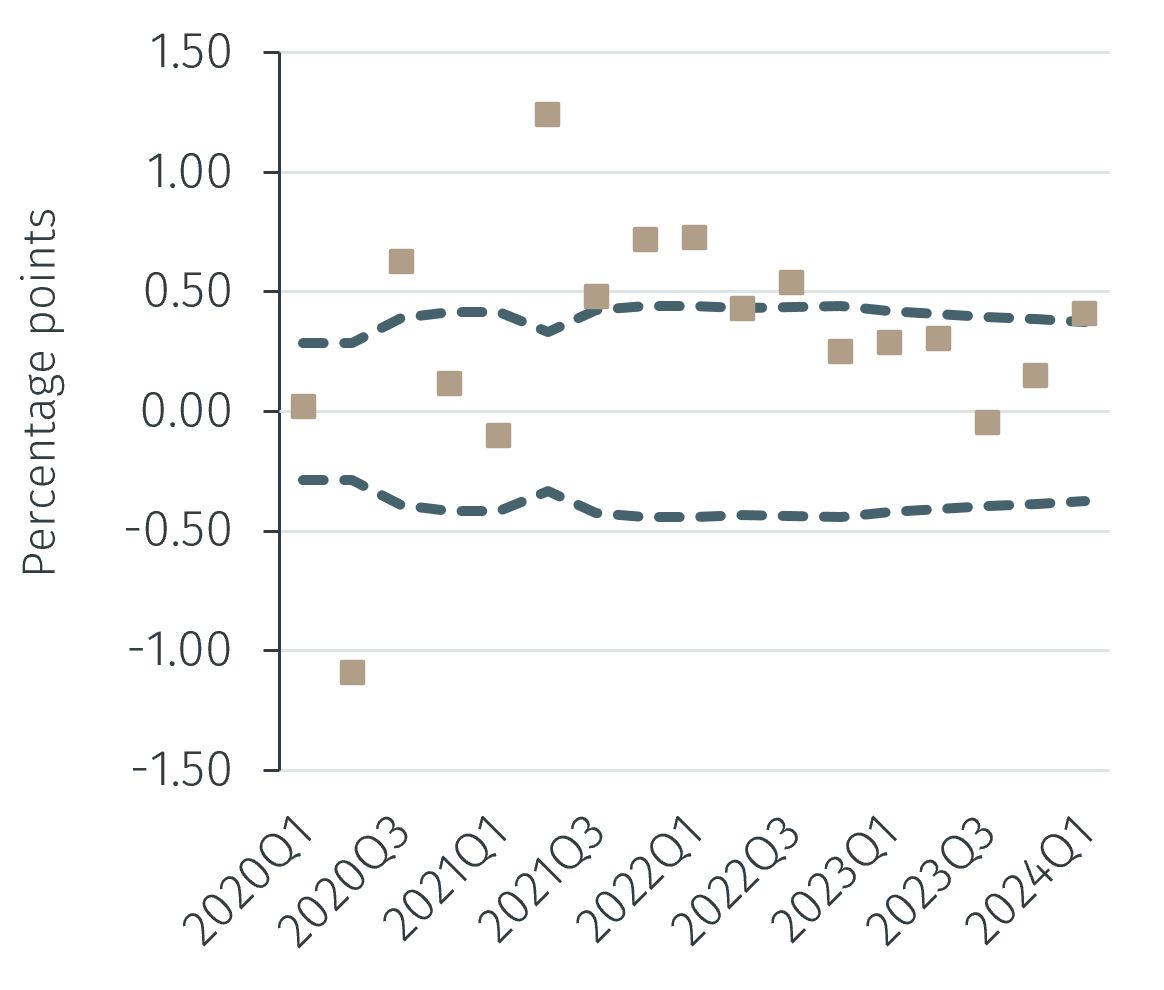

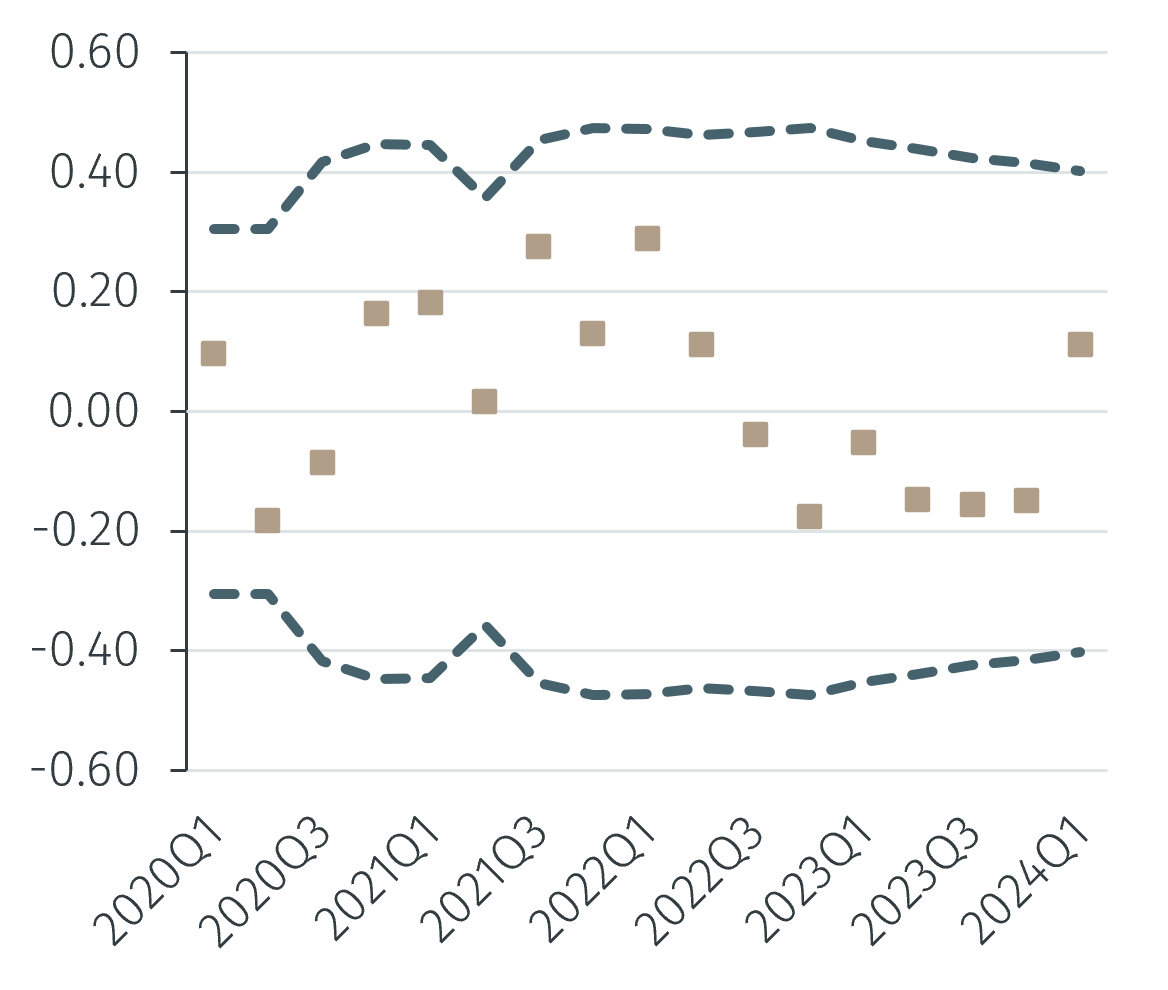

While the surge in US inflation in recent years is generally attributed to the Covid pandemic and the subsequent Russian invasion of Ukraine, it is often argued that strong wage growth has been preventing inflation from returning to levels compatible with price stability. While this sounds plausible, an alternative view is that wage costs simply reflect past inflation. Since inflation lowers real wages (and raises firms’ profit margins), workers demand compensation in the form of higher nominal wages. Under this view, labour market developments contain little information about future inflation.

To attempt to distinguish between these two views, it is useful to look at the behaviour of core inflation and the Employment Cost Index (ECI) which incorporates wages and salaries and the cost of benefits.1