USD 5.7 trillion of annual investment needed by 2030

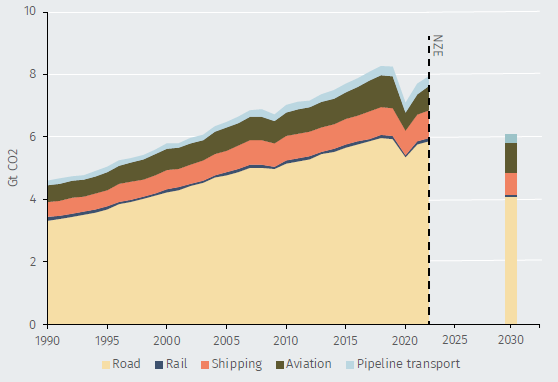

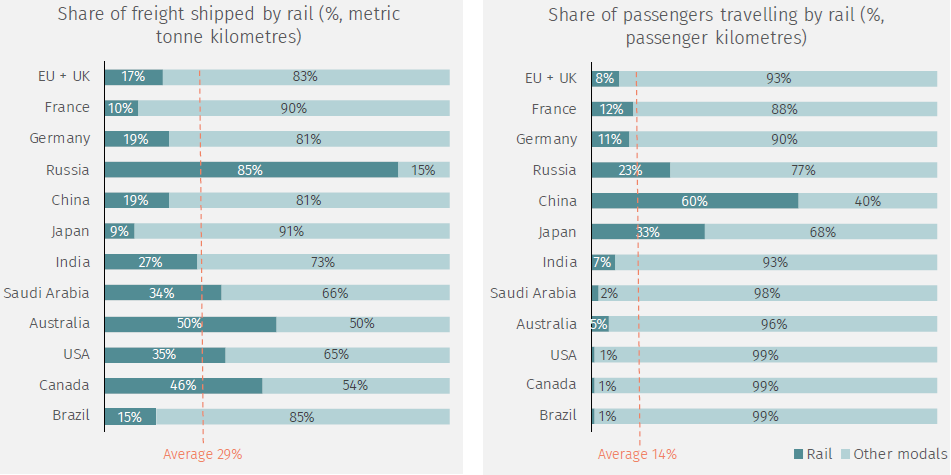

To align with the Net Zero Emissions by 2050 Scenario, the transportation industry will need to reduce its emissions by approximately 25% to around 6 gigatonnes by 2030. To realise this goal, there are four key areas that the sector must focus on: Achieving a swift transition to EVs on our roads, implementing operational and technical measures to increase energy efficiency, facilitating the commercialisation and widespread adoption of low-emission fuels – particularly in the maritime and aviation sectors – and enacting policies that promote a shift towards less carbon-intensive modes of travel. Annual investment of USD 5.7 trillion will be needed in the period to 2030 to realise these goals; this includes redirecting USD 0.7 trillion per year from fossil fuel investments towards technologies that facilitate the energy transition.

Road: EV adoption is key to transport decarbonisation

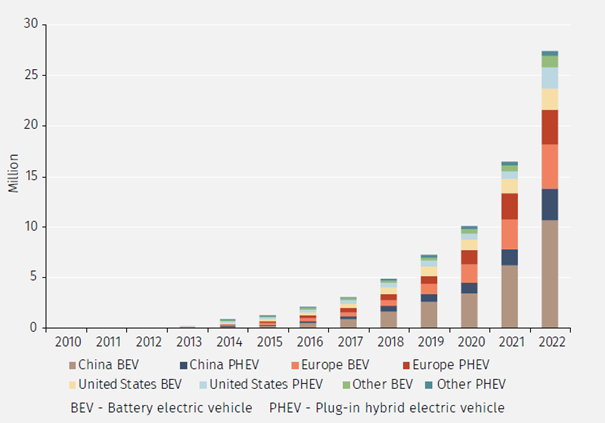

Efforts to boost the adoption of electric vehicles for road use, coupled with the decarbonisation of the power supply, are the most crucial factors in the transportation industry’s transition to net zero. Recent technological advances and, in particular, the latest breakthroughs in battery technology, have significantly enhanced the economic viability of EVs. Several G20 nations have set ambitious electrification goals to lower their reliance on fossil fuels. A notable example is Europe's strategy to ban CO2-emitting cars from its roads with effect from 2035.

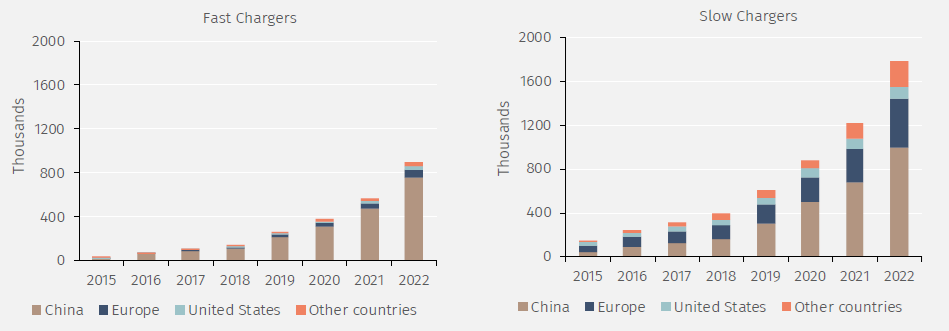

The electric car market is booming, with sales of EVs exceeding the 10 million-mark in 2022, a 55% increase compared to 2021. In fact, EVs accounted for 14% of all new car sales in 2022, up from around 9% in 2021 and from less than 5% in 2020. Further, global spending on EVs exceeded USD 425 billion in 2022, a remarkable 50% increase year on year.

If the recent surge in EV sales can be maintained, this has the potential to align car-related CO2 emissions with the Net Zero Emissions by 2050 Scenario. Importantly, however, rates of EV adoption vary significantly from region to region: While there has been a significant increase in EV sales in China, for example, as well as in certain European countries and some US states, this is far from becoming a global phenomenon. Sales in developing and emerging countries in particular have so far lagged behind other nations as consumers are deterred by higher upfront costs and an inadequate charging infrastructure.