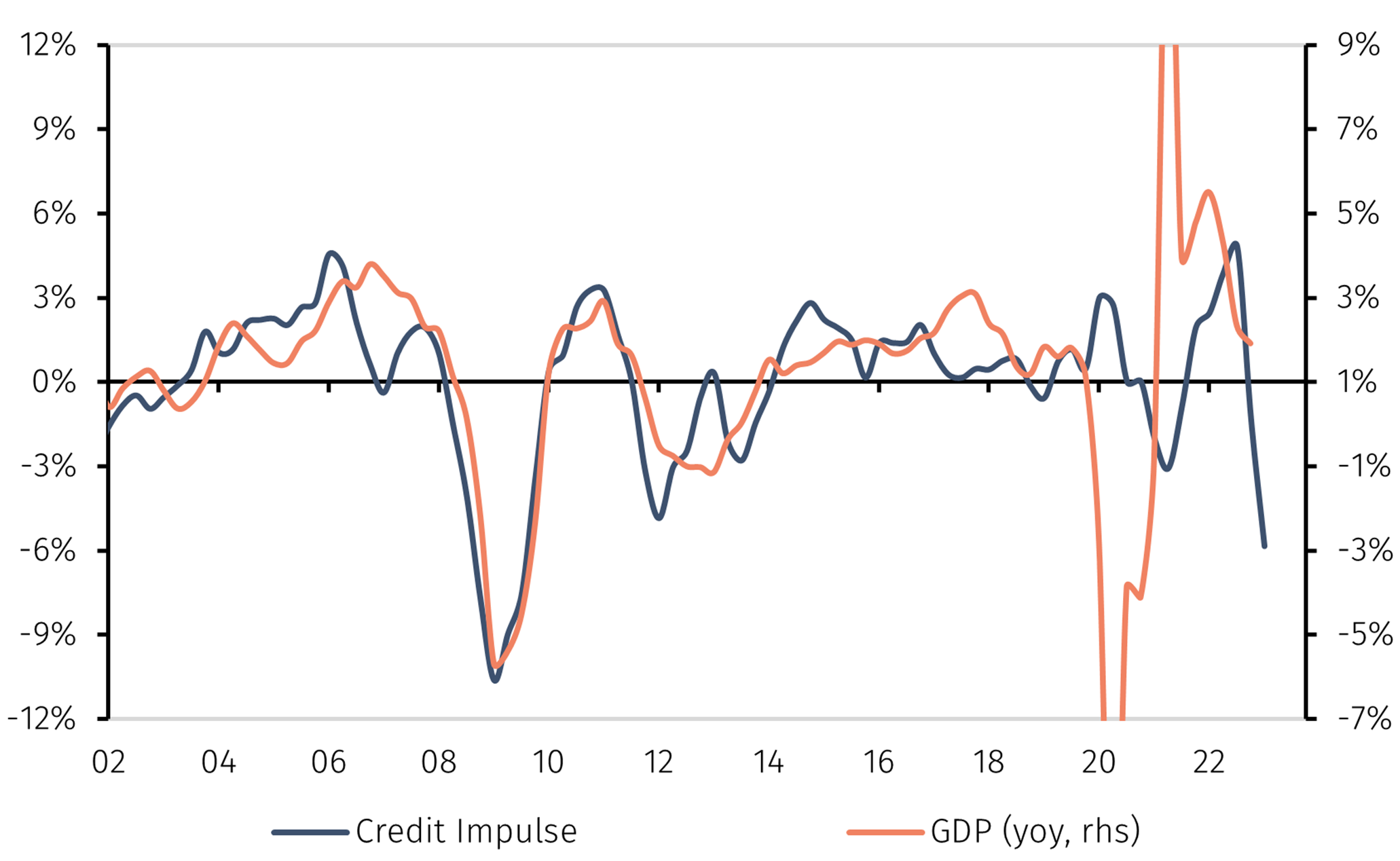

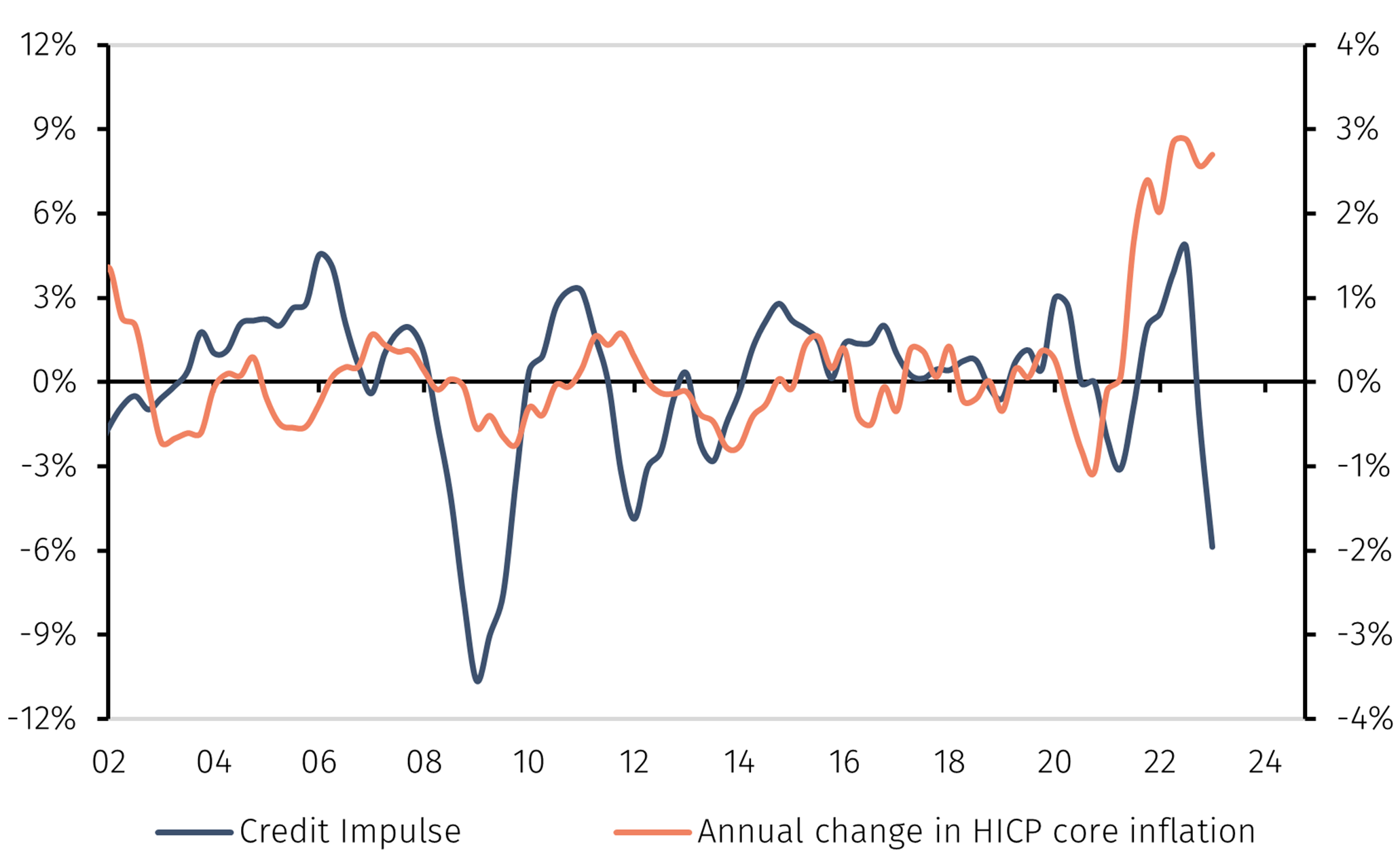

Monetary policy affects the business cycle with long and variable lags. Higher central bank interest rates increase the cost and reduce the availability of credit to the private sector, discouraging demand, slowing GDP growth and inflation. In a bank-centric system like the eurozone, bank lending flows to the private sector are therefore a good guide to how much monetary policy tightening has impacted the economy.

It is notable that net credit flows to the private sector collapsed as soon as the ECB raised its deposit rate above zero last September. In the October-February period, the monthly average of new loans was practically nil compared to about EUR75 bn in the first nine months of 2022 (see Chart 1). Even before the banking turmoil that erupted in March, eurozone credit flows had already evaporated, raising the risk of a full-blown credit crunch.