Chart 1. Central bank policy rates (%)

Source: LSEG Data & Analytics and EFGAM. Data as of 13 November 2023.

Let us know where you’re located so we can tailor our information to make your experience more relevant.

Investment Insights • MFN

4 min read

Over the last few years, the Bank of England (BoE) has been viewed as more tolerant of inflation in comparison to other developed market central banks. Despite being one of the first advanced economy central banks to hike rates in the most recent cycle, the gradualist approach of the Monetary Policy Committee (MPC) in slowly raising rates, differed from the US Federal Reserve and the European Central Bank that both frontloaded their monetary policy tightening (see Chart 1).

Chart 1. Central bank policy rates (%)

Source: LSEG Data & Analytics and EFGAM. Data as of 13 November 2023.

Former members of the MPC argued at a recent BoE Watchers conference that the Bank’s dovish approach was due to the nature of the shocks that drove the surge in UK inflation. Commentators believed that the UK economy had been hit by a succession of tail risk events. Some of these were global events, such as the Covid-19 pandemic and Russia’s invasion of Ukraine. Others were idiosyncratic to the UK, such as Brexit. The MPC believed that, given the long lags with which monetary policy affects prices, over-tightening in response to these supply shocks would have risked magnifying the impact on activity.

On 2 November, the BoE voted to keep interest rates unchanged at 5.25%. In addition, the MPC highlighted the need to keep monetary policy sufficiently restrictive for long enough to bring inflation down to the 2% target. Markets, which expected this decision, interpreted the Bank’s comments as hawkish, after references to any imminent potential rate cuts were removed from the Monetary Policy Report. Nonetheless, markets have reached a consensus that interest rates in the UK have peaked and, in the absence of any large shocks to the economy, should stay at current levels for the rest of 2023 and part of 2024.

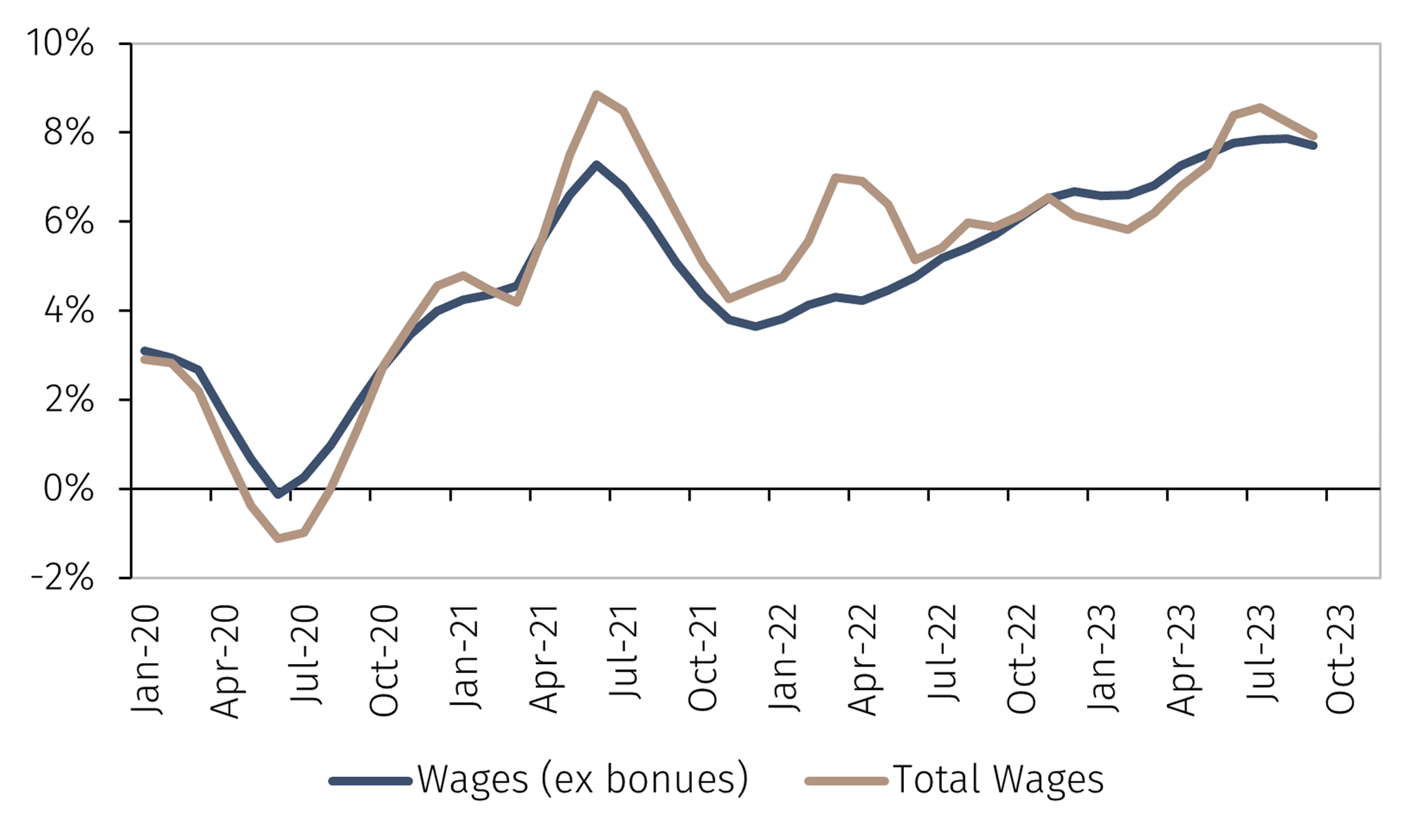

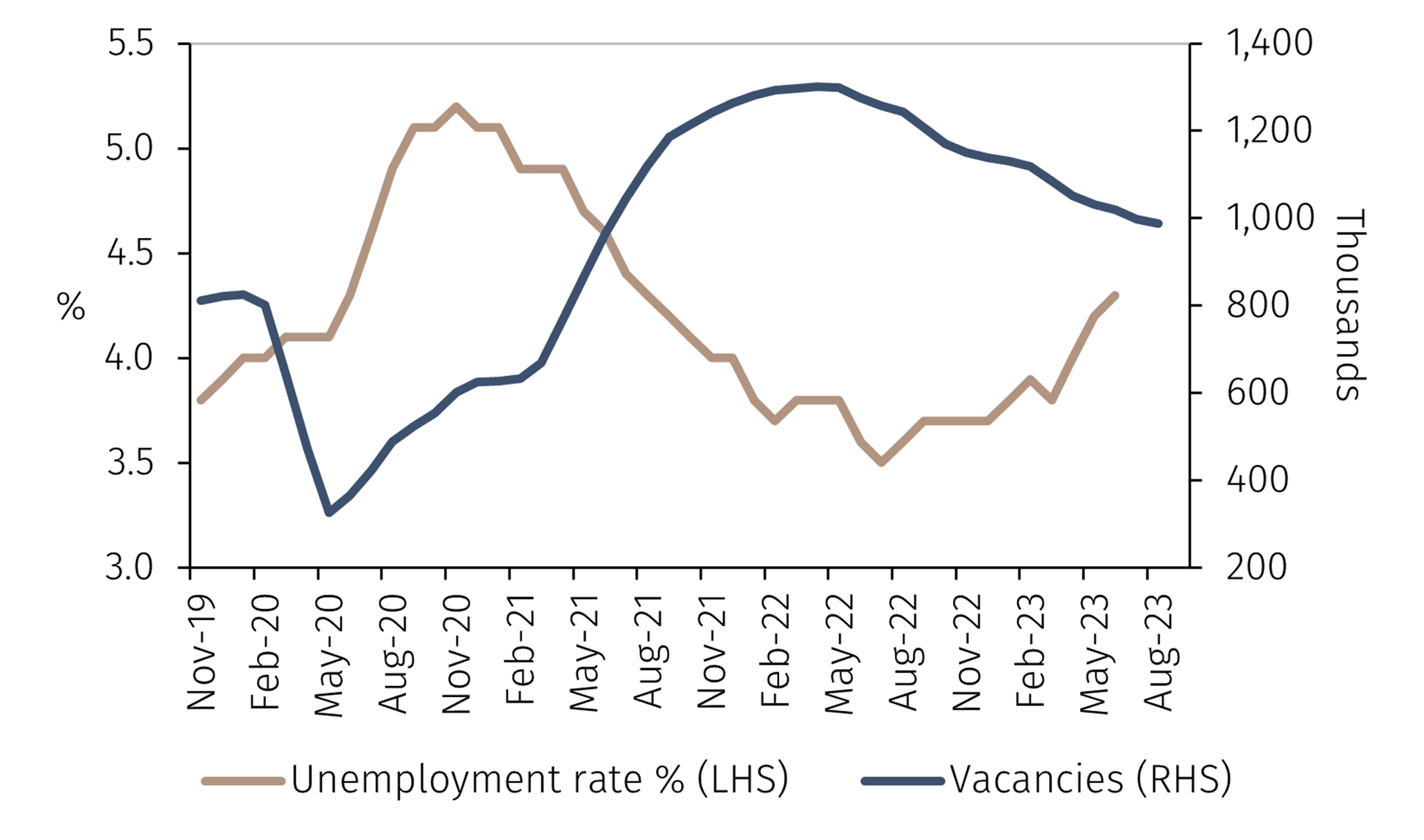

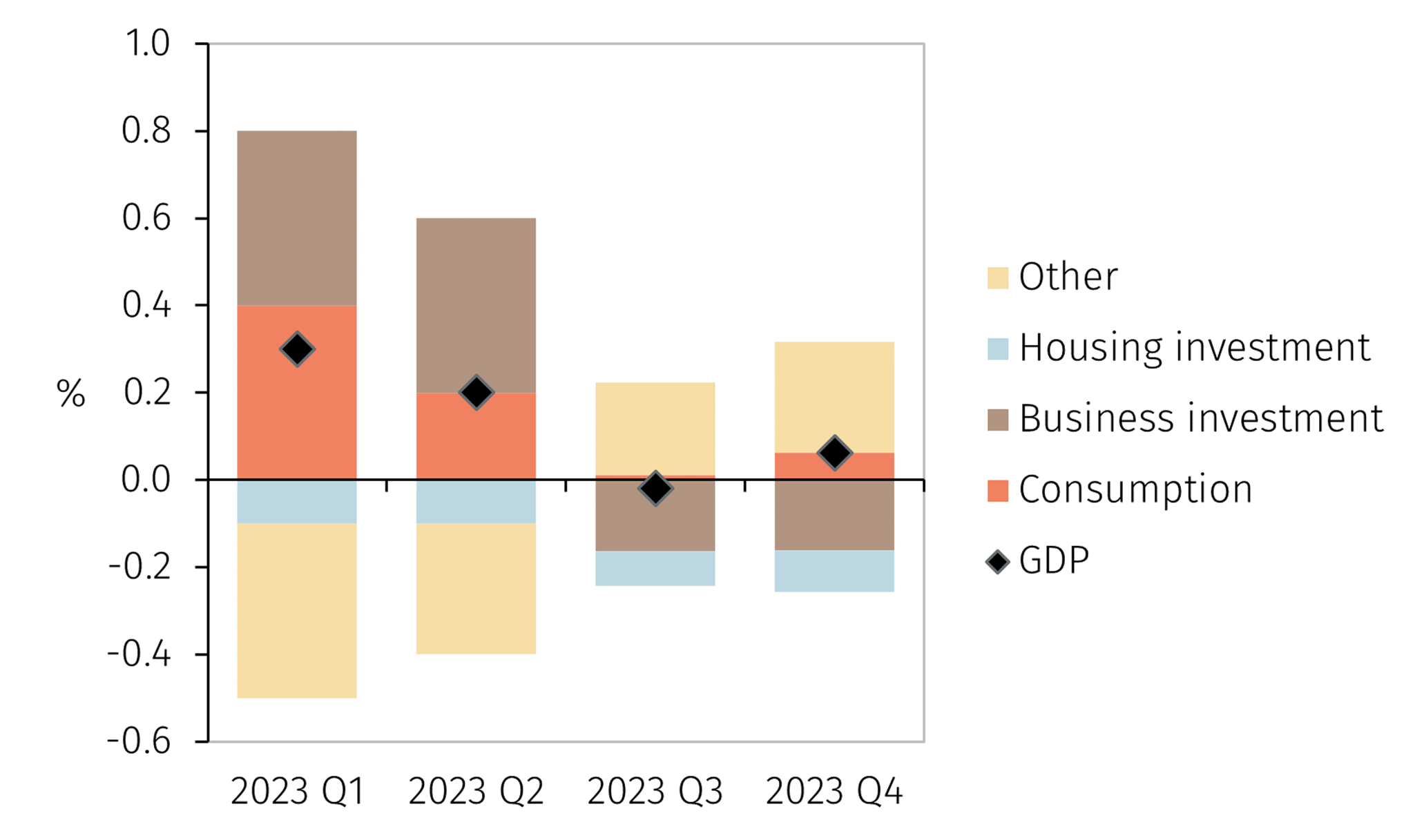

The MPC has previously referenced wage growth, the unemployment rate and GDP growth as the key variables the committee is following to gauge the evolution of prices and the impact of monetary policy on the economy. With interest rates having been increased by more than 500bps since December 2021, these three variables have started to show signs of deterioration:

Chart 2.1. Average weekly earnings %YoY)

Source: LSEG Data & Analytics and EFGAM. Data as of 13 November 2023.

Chart 2.2. Unemployment and vacancies

Source: LSEG Data & Analytics and EFGAM. Data as of 13 November 2023.

Chart 2.3. Contributions to quarterly GDP growth

Source: Bank of England and EFGAM. Data as of 13 November 2023.

To conclude, given the ongoing normalisation of labour market conditions and the weakness of GDP growth, the BoE’s decision to keep rates on hold in November was unsurprising. At this point, the committee seems to prefer avoiding overtightening monetary conditions and magnifying the expected decline in activity. In the absence of shocks, we would expect the BoE to remain on hold for the remainder of 2023 and the first half of 2024. This is in line with market expectations, which currently assign a probability of 40% to a rate cut in June 2024. The MPC adopted a more gradual pace of policy tightening in 2022 and it could be argued that this led to more persistent inflationary pressures. It remains to be seen whether they will follow a similar strategy when it starts cutting rates.

1 It is worth noting that the risk of a wage-price spiral appears overstated; see EFG Infocus, ‘How high is the risk of a wage-price spiral?’, September 2023: https://go.pardot.com/e/931253/-Infocus-wage-price-spiral-pdf/3qpfx/290673036/h/feagkiTL29h2qYQ5g-JBo5aOHBslTaOMT1M8AaMABc8

2 Productivity growth measured as output per hour worked in Q2-2023. https://go.pardot.com/e/931253/oductivity-rebounds-in-q2-2023/3qpg1/290673036/h/feagkiTL29h2qYQ5g-JBo5aOHBslTaOMT1M8AaMABc8

3https://go.pardot.com/e/931253/ference-labour-market-dynamics/3qpg4/290673036/h/feagkiTL29h2qYQ5g-JBo5aOHBslTaOMT1M8AaMABc8

Let us know where you’re located so we can tailor our information to make your experience more relevant.