After a sharp tightening of monetary policy in 2022 and 2023, several major central banks are now signalling that interest rate increases are over, barring new shocks. With inflation falling and growth slowing, financial markets are anticipating cuts to policy rates in the first half of 2024 (see Chart 1).

Investment Insights • MFN

4 min read

Four shades of pivot

Speculation is building that monetary policy in the US and Europe is about to change course. In December, central banks signalled, albeit with different nuances, that barring any new shocks to inflation, the next move of interest rates will be downward. In this Macro Flash Note, GianLuigi Mandruzzato reviews the most recent Fed, ECB, BoE and SNB meetings.

Chart 1. Policy rates, actual and market expectations

Source: LSEG Data & Analytics, and EFGAM calculations. Data as at 15 December 2023.

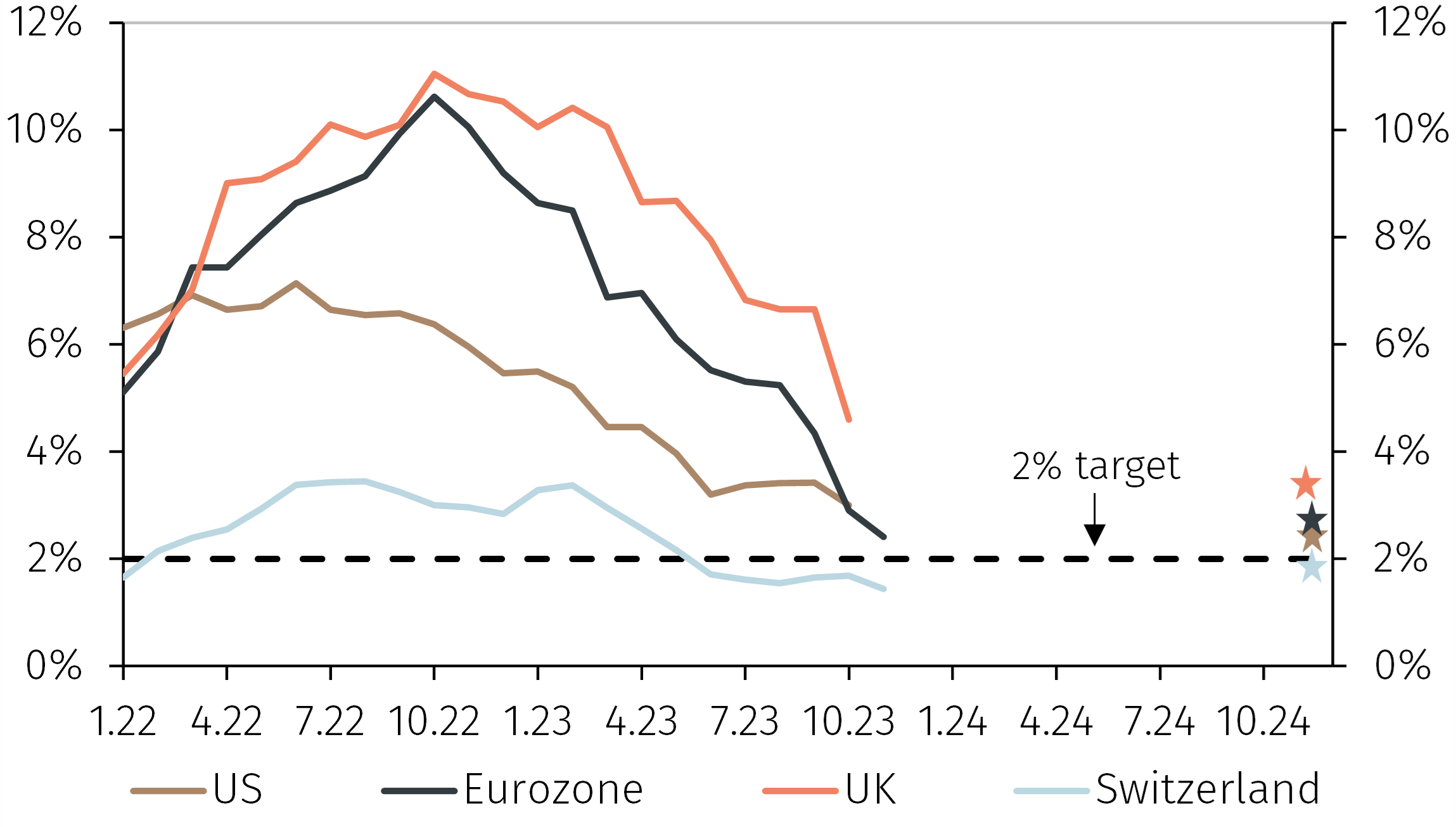

That inflation and economic growth fell a year and a half after interest rates were raised aggressively is not surprising. Furthermore, the delay with which rate increases dampen inflation suggests that the full impact of tighter monetary policy will emerge only in 2024. It is therefore reasonable that central banks now expect inflation to fall towards their objectives without further interest rate increases (see Chart 2).

Chart 2. Inflation and 2024 central bank forecasts (YoY)

Source: LSEG Data & Analytics, and EFGAM calculations. Data as at 15 December 2023.

Nevertheless, central banks’ views about interest rate cuts differ. The US Federal Reserve (Fed) appears most open to a relaxation of monetary policy, followed by the Swiss National Bank (SNB), European Central Bank (ECB) and the Bank of England (BoE). This is unsurprising given the Fed's dual mandate of maximum employment and price stability, in contrast to the other central banks whose mandates prioritise fighting inflation.

The FOMC’s dot plot suggests that the fed funds rate could be cut by 0.75% in 2024 and that rate cuts will continue in the following years if the economy evolves as it expects (see Chart 3). In December, Chair Powell said that the FOMC has already discussed how to proceed with rate cuts and that the committee is conscious of the risk that inflation falls below target if monetary policy is kept too restrictive for too long. Hence, Powell noted that interest rates should be reduced before inflation returns to 2%. Market participants now believe that the fed funds rate will be cut as early as March 2024, with up to six cuts to the end of 2024.

Chart 3. The Fed's December Dot Plot

(Implied fed funds target rate, %)

Source: Federal Reserve and Bloomberg. Data as at 15 December 2023.

In Europe, central banks have been more cautious about rate cuts. However, the SNB significantly trimmed its inflation forecasts for the coming years and made clear that, unlike the last two years, currency market interventions will no longer be aimed solely at supporting the Swiss franc. It also noted downside risks to economic growth, which was already expected to be below potential in 2024. This has led markets to price in interest rate cuts as early as next March and a cumulative 0.75% reduction in the whole of 2024 (see Chart 1).

The ECB also lowered its inflation and growth projections for the coming years. However, President Lagarde said the Governing Council had not discussed rate cuts and reiterated that to bring inflation back to target, interest rates must remain at the current level for a prolonged period. Despite the faster-than-expected fall in inflation and the downside risks to growth, the ECB seems in denial about the implications for monetary policy. However, as highlighted by Lagarde, the ECB remains “data dependent” and it would not be surprising if inflation projections were reduced further in March 2024, opening the door to rate cuts as markets expect (see Chart 1).

Finally, the BoE left rates unchanged, but three of the nine Monetary Policy Committee members voted for an increase of 0.25% and the official policy statement noted that rates could rise further if inflation proves more persistent than expected. The BoE's relatively hawkish message compared with the other central banks reflects the greater distance between current and expected inflation and the 2% target. This is despite the BoE having raised interest rates earlier than most other major central banks in developed countries.

In conclusion, it is increasingly likely that interest rates have peaked and that monetary policy will be eased in 2024 in many countries. The Federal Reserve has been explicit in this regard, while central banks in Europe have been more cautious. However, if inflation continues to decline as expected, interest rates will also be cut in Europe, perhaps from spring 2024, and monetary policy normalisation will likely continue in 2025.

1 The Fed’s dot plot, updated quarterly, shows each FOMC member’s projection for the appropriate level of the federal funds rate at the end of each calendar year.