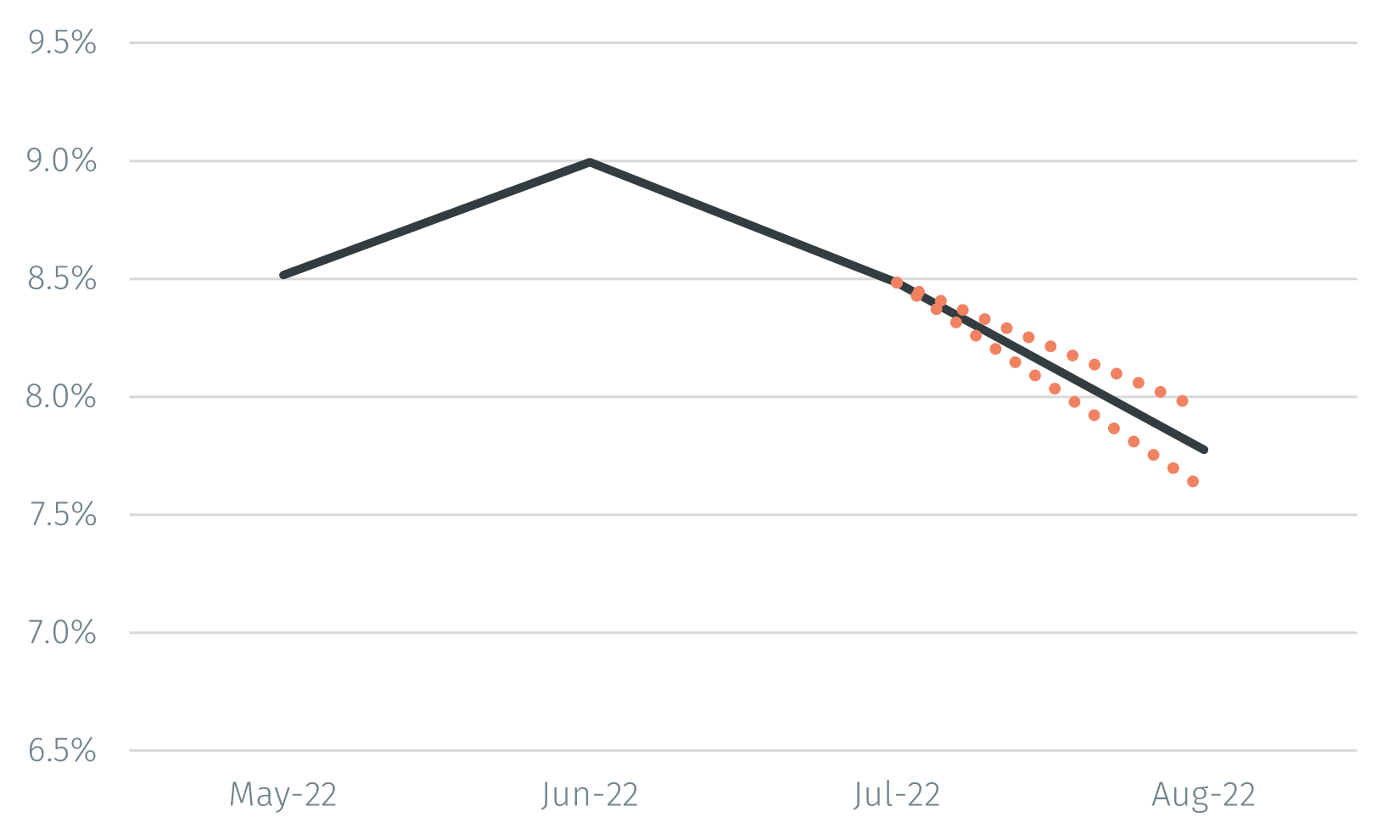

On 13 September US CPI inflation for August will be released. After reaching 9.1% in June, it fell to 8.5% in July. Chairman Powell stated in his Jackson Hole speech on 26 August that a one-month decline in CPI inflation is not enough for the Federal Reserve to question its outlook for US monetary policy, but a series of positive inflation surprises is likely to do so. Much attention is therefore focused on the August release.1

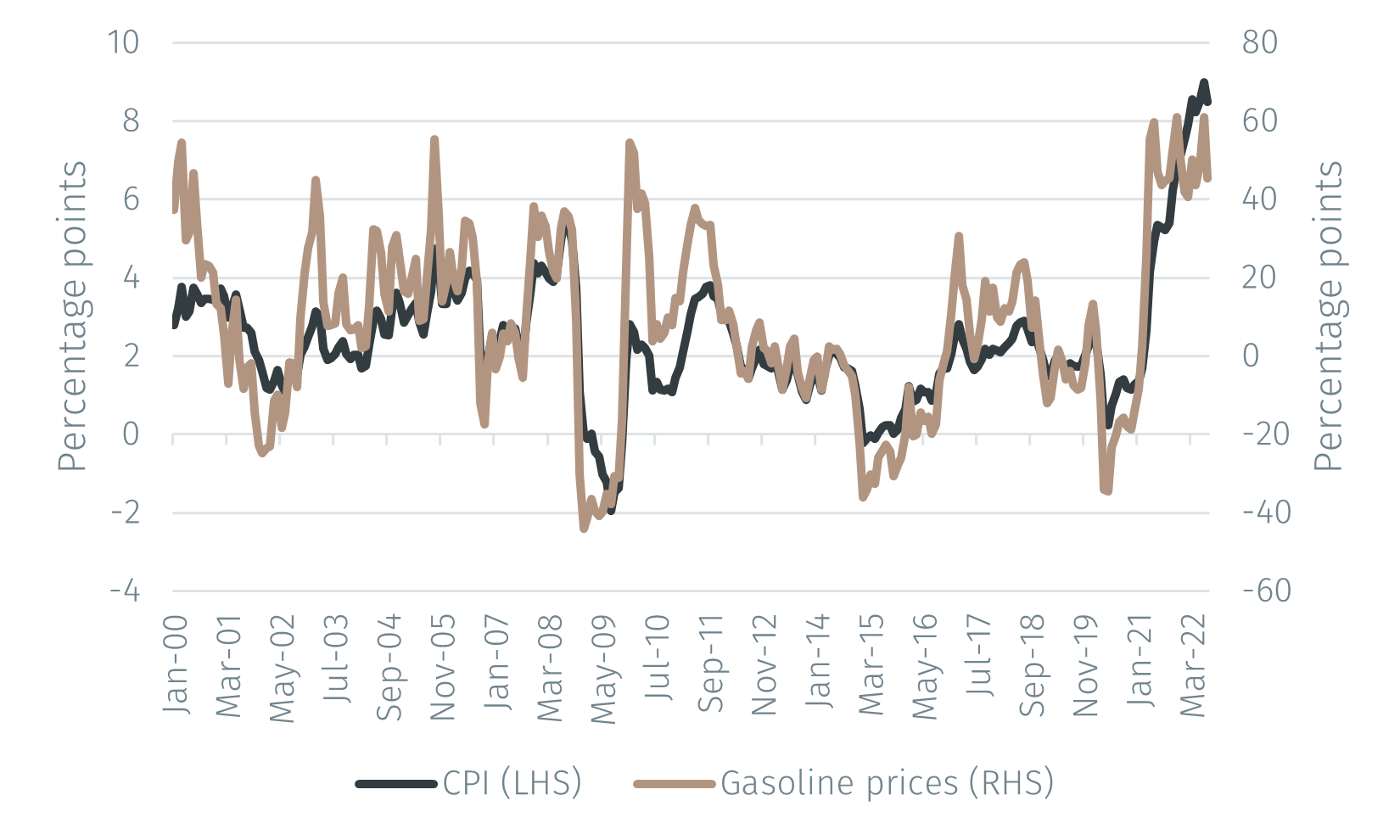

One important driver of CPI inflation has been energy prices, which constitute 9.2% of the US CPI and which rose 32.9% between July 2021 and July 2022. A large part of energy is gasoline prices, which have a weight of 5.2% and rose 44.0% in the year to July 2022. That these components contributed to the decline in inflation between June and July this year is clear: energy prices fell by -4.5% and gasoline prices by -7.7% on a monthly basis.

Gasoline prices at the pump are readily observed and are collected weekly by the US Energy Information Administration.2 We therefore know that average gasoline prices fell by -12.8% between July and August. The direct effect on this decline is thus to reduce the CPI by 0.7%. This suggests that the annual CPI inflation will fall further in August to perhaps 7.8%.

The chart below shows annual CPI inflation and the change in gasoline prices over 12 months. As it is clear, while gasoline prices experience swings of much greater magnitude, the two series are very strongly correlated (correlation = 0.84).