Many commentators believe that the price of gold will soon rise due to the implementation of new rules on banks’ capital requirements under Basel III.1 First announced in 2017, the Basel III rules apply to banks operating in the US, the European Union and Switzerland since the end of June 2020. Notably, as of 01 January 2022 they will also apply to UK banks and hence to a dominant share of financial transactions related to gold settled on the London Bullion Market.

The new regulation distinguishes between allocated and unallocated gold accounts. Gold in allocated accounts is held in custody in a bank’s vaults but belongs to the bank’s clients. Unallocated gold accounts reflect financial transactions linked to gold including gold lending, swaps, futures, and hedging for producers and refiners as well as jewellers and other corporate users. Unallocated gold accounts belong to the bank.

Under the new regulation, allocated gold will be considered a Tier 1 asset and will continue to have zero risk weighting. Conversely, banks’ unallocated gold and exposures due to other financial transactions will be considered a Tier 3 asset subject to a Required Stable Funding (RSF) ratio of 85% like other risky assets such as equities. Under the new rules, banks are required to hold physical gold or other liquid assets for an amount equal to at least 85% of the value of unallocated gold on their books.

Unallocated gold accounts, often referred to as paper gold, are attractive to banks because they can leverage on the gold actually held in the vaults: some estimates put the ratio of unallocated gold to physical gold at up to 400 times, making it potentially very profitable to bullion banks. A likely, and probably intended, consequence of the Basel III rules will be a drop in the volume of financial transactions linked to gold. The increased cost of these activities will encourage bullion banks to reduce their exposure or to increase the price they charge clients, who may reduce demand for those products.

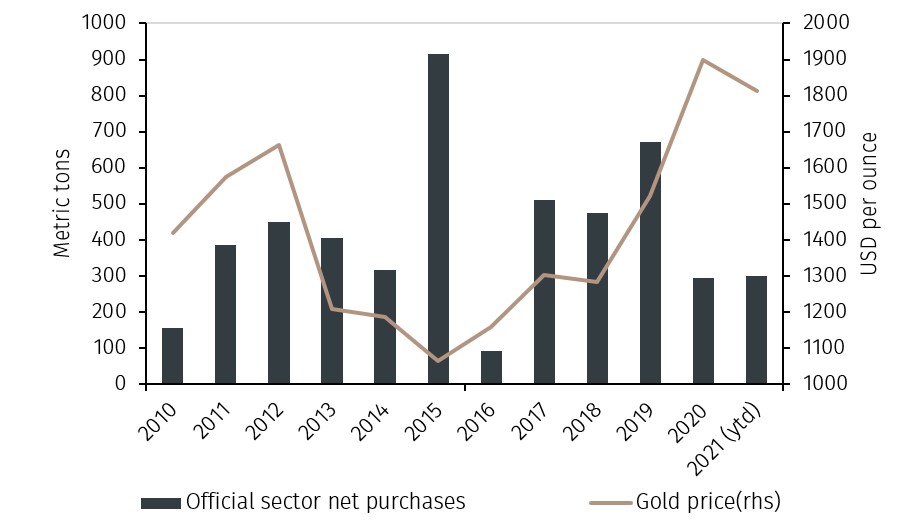

The new rules give physically held gold a preferential treatment over paper gold, and that should increase demand for bullion and support the price of gold. Many commentators see as no coincidence that since 2017 central banks have purchased large volumes of physical gold and that gold prices have generally risen (see Chart 1). Because of the new rules, banks are expected to advise clients to turn unallocated into allocated gold positions, increasing, at least temporarily, the demand for physical gold. However, since this would mainly be an accounting effect rather than a real increase in demand for the yellow metal, the impact on gold prices looks uncertain.