- The continuation of the war in Ukraine has heavily influence market direction since it began on 24 February. As seen during previous episodes of heightened geopolitical tension, volatility has soared, the prices of safe haven assets have risen, and equities have fallen. In addition, commodity prices have risen sharply as a result of sanctions imposed by Western countries on Russia that limit their availability.

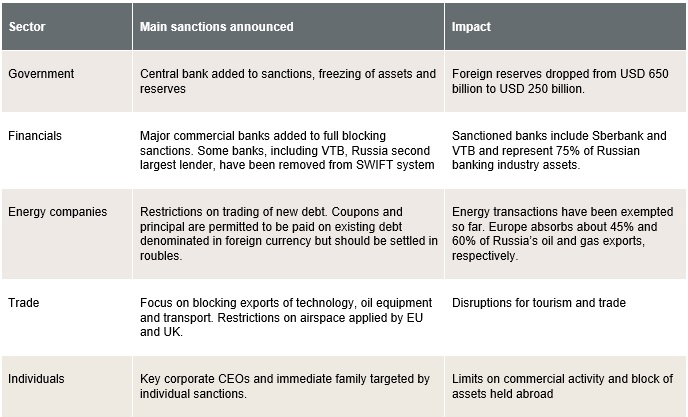

- Russian assets have been under severe stress after a series of credit downgrades and their expulsion from various indices, including those managed by MSCI and FTSE. On 28 February, the Central Bank of Russia raised the official interest rate to 20% and said the stock market will be closed until at least 11 March. After the seizure of a significant share of Russian foreign reserves and the exclusion of most Russian and Belarusian banks from the SWIFT system of international payments, the Russian government has decreed that the maturing foreign debt of Russian entities must be settled in roubles, although it seems that private companies have some leeway if they hold enough hard currency offshore. As for domestic bonds, the government decreed that no payment should be made to residents in one of the listed “unfriendly” countries.

- While the situation remains highly fluid and uncertain, it is encouraging that in the last couple of days markets have regained some ground from heavily oversold conditions and two-way price action has re-emerged. This may reflect the hope that diplomacy will eventually prevail in bringing about a negotiated solution.

- Meanwhile, the Russian army is advancing and slowly taking control of an increasing proportion of Ukrainian territory. At the time of writing, the Russian army had not entered the capital, Kyiv, or taken control of other important cities such as Odessa and Lviv.

- Despite the superiority of the Russian army, the resistance of the Ukraine army and people has so far been stronger than expected and is reported to have caused a rising number of casualties among Russian troops, possibly thanks to the military equipment sent over by Western countries.

- Beyond providing humanitarian and limited military support, Western countries are raising the pressure on Russia and Russian oligarchs close to Putin by imposing a very strict set of sanctions. Russia is now subject to more than five thousand sanctions, mostly targeting individuals and entities. In addition, more than 300 Western multinationals have stopped doing business with or in Russia.

Ukraine Update

Investment Insights

5 min read

Ukraine Update

With the war in Ukraine continuing, GianLuigi Mandruzzato and Joaquin Thul take stock of recent developments and their potential implications for markets in this Macro Flash Note.

- The overall impact of sanctions on the Russian economy is still hard to estimate. Sanctions are not new, but the speed with which they have been imposed and the incremental impact they will have the longer they stay in place, suggests there will be a large negative effect on Russia GDP. Analysts’ projections anticipate a contraction of Russian GDP of between 7% and 15% in 2022. For comparison, the Russian debt crisis in 1998 triggered a decline of 5.3% in GDP.

- President Putin compared sanctions to an act of war. Moscow reacted by issuing a list of countries taking “unfriendly actions” against Russia, its companies and citizens.1

- Meanwhile, diplomatic efforts continue to try find an agreement that would stop the war. On 10 March, the Foreign Ministers of Ukraine and Russia met in Turkey. Although there was no progress made on a ceasefire, both parties said that they are ready to meet again if there is the genuine prospect of reaching an agreement. Before the meeting, Ukrainian President Zelensky indicated that he is open to the possibility of a compromise on Crimea (annexed by Russia in 2014) and the separatist region of Dombas. Russia for its part has said that it does not intend to “overthrow” the Ukrainian government.

- China has engaged in diplomatic efforts, offering support for a negotiated solution. While calling for a ceasefire, China has avoided criticising Russia and instead blamed NATO actions for the conflict between Russia and Ukraine. China also criticised the imposition of Western sanctions against Russia expressing concern about their negative impact on the economy.

- It is increasingly clear that higher energy and food prices and further disruptions to the global supply chain will take their toll on GDP growth and push inflation higher than previously anticipated. According to a preliminary assessment from the ECB, the crisis in Ukraine will reduce 2022 eurozone GDP growth by about 0.8% while inflation will be almost 2% higher.

- At the moment, the impact on the outlook for central banks has been limited to a minor downgrade to rate expectations. However, the longer the crisis lasts the greater the negative economic shock. That would be expected to encourage central banks to move more slowly on policy normalisation than previously anticipated.

- Reflecting a high degree of risk aversion, equity markets remain close to recent lows, with more stress in European markets and in growth stocks. We are continuing to assess the situation and adjusting our investment views accordingly.

1 The list of countries includes Albania, Andorra, Anguilla, Australia, British Virgin Islands, Canada, European Union member states, Gibraltar, Great Britain (including Jersey), Iceland, Japan, Liechtenstein, Micronesia, Monaco, Montenegro, New Zealand, North Macedonia, Norway, San Marino, Singapore, South Korea, Switzerland, Taiwan, Ukraine and United States.