|

Iran

|

Ceasefire talks fail and the new leadership doubles down with an aggressive approach to attacking US and Israeli assets. Other countries in the region become increasingly and reluctantly dragged into the conflict. The US puts troops on the ground, and the situation escalates. The Iranian regime successfully forces the war to drag on for at least several more months and possibly into year end. The Strait of Hormuz becomes militarised, acting as an ongoing deterrent to seaborne energy transportation, resulting in a prolonged increase in energy prices.

|

The US and Iran finally agree to a tentative cease-fire and the next two weeks sees a series of meetings, public arguments, rumours, and possibly the odd missile strike via proxies. Tankers and freights do start to move through the SoH with a co-ordinated supervision agreement for ships to transverse through the Strait. Fees to be paid for re-construction of Iran does become a bargaining chip longer term. Trump may not oppose this, but it certainly would become an issue for the other GCC countries. The Iranian leadership maintains the same philosophy as the prior regime but de-emphasises its short term nuclear and military ambitions, focussing instead on stabilising the domestic situation. The threat to US and Israeli assets - including via terrorist actions around the world – subsides but does not disappear. Trump claims victory although the situation remains highly fragile. Iran may rebuild its military capabilities over the longer term.

|

The new Iranian leadership adopts a much more conciliatory approach resulting in swift and successful ceasefire and disarmament negotiations. Within a few months a new nuclear deal is announced, and an agreement is reached to curtail Iran's ballistic missile program. The Israelis, although un-happy with the deal, step back driven by a large deterioration in popularity for the Israeli administration in the US according to the latest polls.

|

|

Political backdrop

|

Trump does not want an extended war. The longer the war goes on, the more problematic it is for the US given opinion polls and forecast mid-term performance. Trump's popularity even amongst his traditional “MAGA” base is on a downtrend due to Epstein, high and rising costs of living (energy prices), tariffs, and other initiatives driven by the White House. The Trump-Xi summit is now scheduled for 14 May and it is in Trump's interests to reach some sort of ceasefire/deal by then. However, this is not guaranteed.

|

Trump does not want an extended war. The longer the war goes on, the more problematic it is for the US given opinion polls and forecast mid-term performance. Trump's popularity even amongst his traditional “MAGA” base is on a downtrend due to Epstein, high and rising costs of living (energy prices), tariffs, and other initiatives driven by the White House. The Trump-Xi summit is now scheduled for 14 May and it is in Trump's interests to reach some sort of ceasefire/deal by then. However, this is not guaranteed.

|

Trump does not want an extended war. The longer the war goes on, the more problematic it is for the US given opinion polls and forecast mid-term performance. Trump's popularity even amongst his traditional “MAGA” base is on a downtrend due to Epstein, high and rising costs of living (energy prices), tariffs, and other initiatives driven by the White House. The Trump-Xi summit is now scheduled for 14 May and it is in Trump's interests to reach some sort of ceasefire/deal by then. However, this is not guaranteed.

|

|

Financial markets

|

The impact of the war is extended, due largely to the persistence of upward pressure on energy prices and the feed through to inflation / inflation expectations. There is a large equity market correction of 10-20% as markets reprice for higher oil and gas prices and the expectation of higher rates and rising bond yields. Risk premia generally move higher. Credit spreads - including emerging markets - widen and remain elevated for the next few months.

|

The market remains range-bound from the previous peak to down 10%. Investors take time to assess the consequences and what it means for asset prices. Once that assessment has been made and the likely future paths of the global economy, rates and earnings become clearer, calmness and order returns. There is mild credit spread widening from the lows at the end of February, but that’s the extent of it. Other factors, such as earnings, rate expectations, tariffs and the meeting with Trump and Xi will determine whether markets go to new highs.

|

Markets breathe a sigh of relief and a rally in risk assets continues. Equity markets rebound and reach new 52-week highs led by cyclicals. Credit spreads tighten back to levels seen in Q4 2025.

|

|

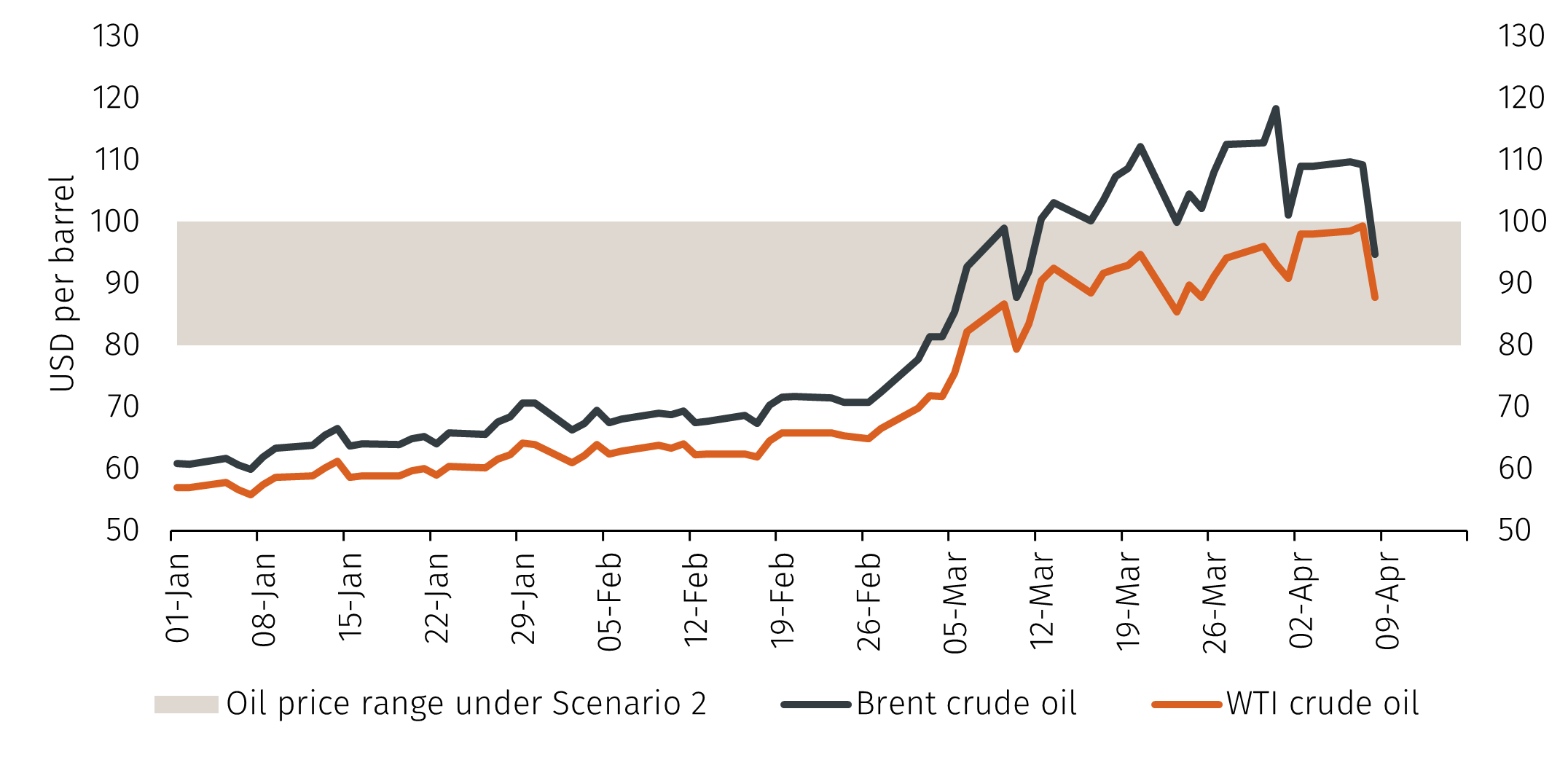

Oil price

|

The bulk of the move in the oil price has already taken place but over time the cost of a barrel of Brent continues to move higher, eventually reaching $140pb and staying elevated for some time. Gas prices follow a similar path, something that is more problematic for Europe than for the US.

|

Energy prices initially remain elevated, with the oil price levelling off in the range $80 - $100 per barrel. As the war concludes and traffic starts to move once again through the SoH oil prices recede but remain a little higher than before the war due to an elevated risk premia.

|

There is a more immediate and profound decline in the oil price of 25% due to the positive news flow and increased OPEC+ supply, however a small risk premium remains as countries from all around the world build strategic reserves. Renewables become an even greater focus which sows the seeds for an oil price below $50 per barrel.

|

|

Precious metals/FX

|

Gold stays within the range of $5,000/oz to $5,500/oz. The CHF stays stronger against the EUR and GBP but is weaker against the USD. In this scenario the USD remains the strongest currency.

|

Gold stays in the current range ($4,000 - $5,000/oz), driven by demand disruption vs geopolitical action. We expect the USD to remain rangebound against the majors and on a trade weighted basis.

|

The gold price trades in the middle end of the range at around $4,500/oz, as lower rates are offset by the diminished geo-political risks. The USD resumes its downtrend; however, the CHF is weaker against the GBP and EUR.

|