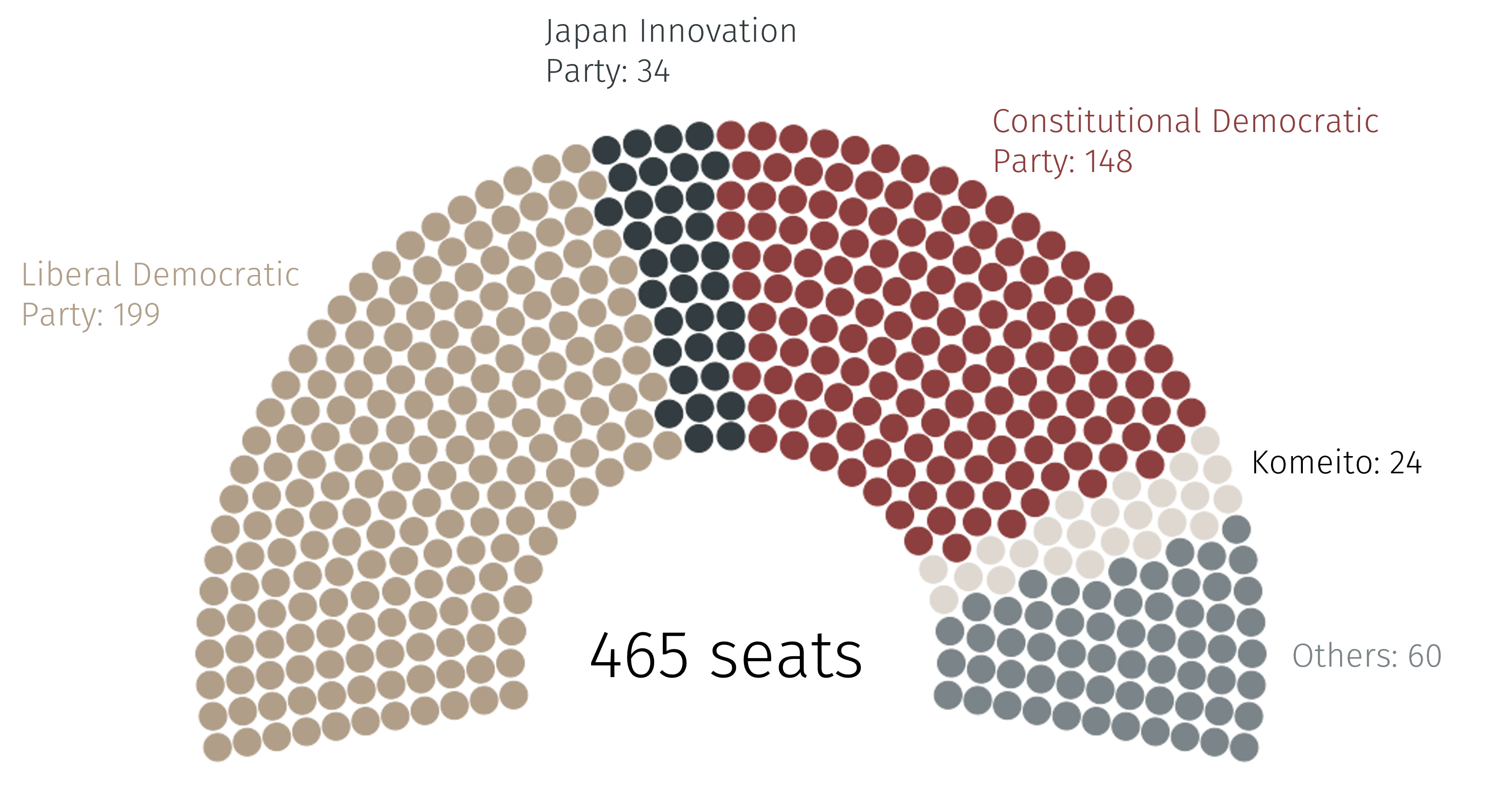

Source: Japan House of Representatives and EFG calculations. Data as at 26 January 2026.

Timing is everything

There is also an important timing piece to this election. Takaichi made comments in November which implied Japan would be willing to intervene using military force if China decided to invade Taiwan. This irked China, which responded by encouraging its residents not to visit Japan and imposing export restrictions on dual-use goods.

China was the top source of tourism for Japan in 2025.2 Yet in December, following Takaichi’s comments, the number of tourists from China fell by almost a half from the same month a year earlier.3 Of greater concern to Takaichi will be the imposition of restrictions on exports of dual-use goods. These goods include rare earths, an area in which China dominates the global supply chain.4

Takaichi is currently experiencing extremely high approval ratings.5 There is no doubt that she is seeking to capitalise on nationalist sentiment before any economic impact from escalating tensions with China is felt by Japan’s electorate.

Land of the rising sun

Takaichi has vowed to make Japan a “land of the rising sun” again. Her rhetoric often adopts elements that could easily find themselves in Trump’s “Make America Great Again” playbook. This is no accident. Fostering the US-Japan relationship is of the utmost importance to Takaichi. Despite having declared a new golden age for the alliance in late 2025, Japan’s Prime minister remains well aware of the need to keep Trump onside and avoid being caught in his crosshairs.

Recent events regarding Greenland make Takaichi’s nomination of Trump for the Nobel Peace Prize look like a masterstroke and the absence of Bank of Japan (BoJ) Governor Kazuo Ueda from the international central bankers’ statement in support of Fed Chair Jerome Powell should not be viewed as purely coincidental. Japan is carefully curating its relationship with the US and image plays a key role in doing so. When Takaichi visits the White House in March, she will be hoping to do so as a leader who carried her party to a large election victory and has a strong mandate to govern.

Election implications

The market implications of a strong LDP election victory could be meaningful. Such a scenario could reignite the “Takaichi trade” given expectations of more expansive fiscal policy, leading to a rally for Japanese equities spurred on by stronger growth expectations and a sell off for Japanese government bonds and the Japanese yen amid fiscal sustainability concerns.

Sustained yen weakness beyond what fundamentals warrant could pull forward the next BoJ interest rate increase. While the BoJ was on hold at its meeting on 23 January, there were many signals that provided a hawkish tilt. Notably, one Policy Board member dissented and voted in favour of raising rates from 0.75% to 1.00%, and the growth and inflation forecasts for the fiscal year starting in April were raised (see Chart 2).6