As expected, the Bank of England’s (BoE) Monetary Policy Committee (MPC) cut Bank rate by 25bps to 3.75% at its 18 December meeting. Although a few months ago this was not priced-in by analysts, recent data on inflation, wage growth and unemployment prompted five MPC members to vote in favour of a rate cut. The decision was reached by a majority of 5 to 4, with the swing vote coming from Governor Andrew Bailey.

No need for negative SNB rates

Investment Insights • Macro

3 min read

Governor Bailey swings the vote as BoE cuts rates

At its December meeting, the Bank of England delivered a hawkish rate cut. Despite reducing the Bank rate to 3.75%, it signaled that further monetary policy easing is not guaranteed. In this Macro Flash Note, Economist & Strategist Joaquin Thul discusses the latest decision.

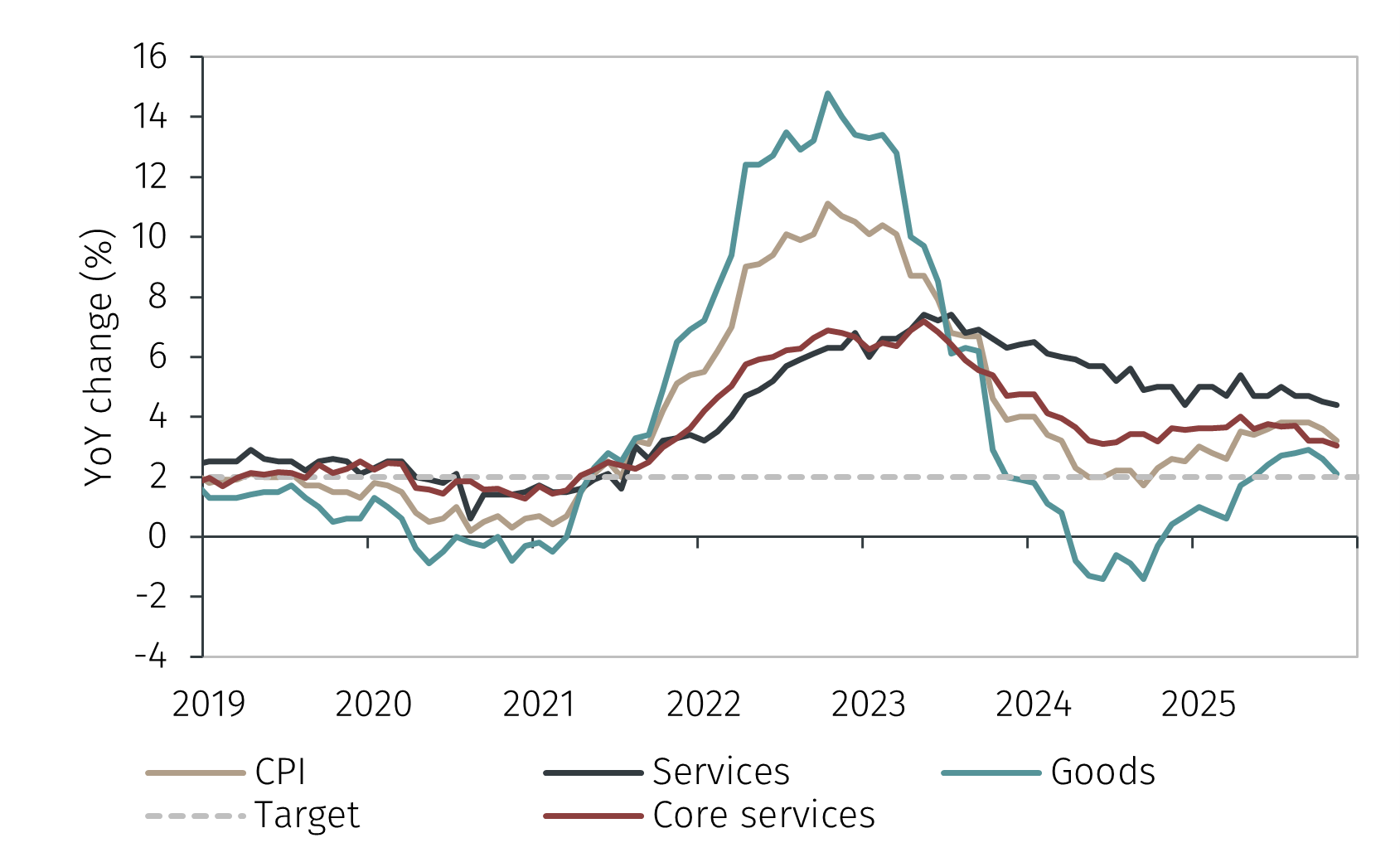

Chart 1. UK goods and services inflation

Source: LSEG Data & Analytics and EFG. Data as of 18 December 2025.

Softening inflation and labour market tightness

The change in Governor Bailey’s vote in relation to the previous meeting in November reflected the fall in inflation to 3.2% year-on-year (YoY) in November. Moreover, the softening in core services inflation has become more evident in recent months, highlighting easing domestic prices and reduced upward risks to inflation (see Chart 1).1

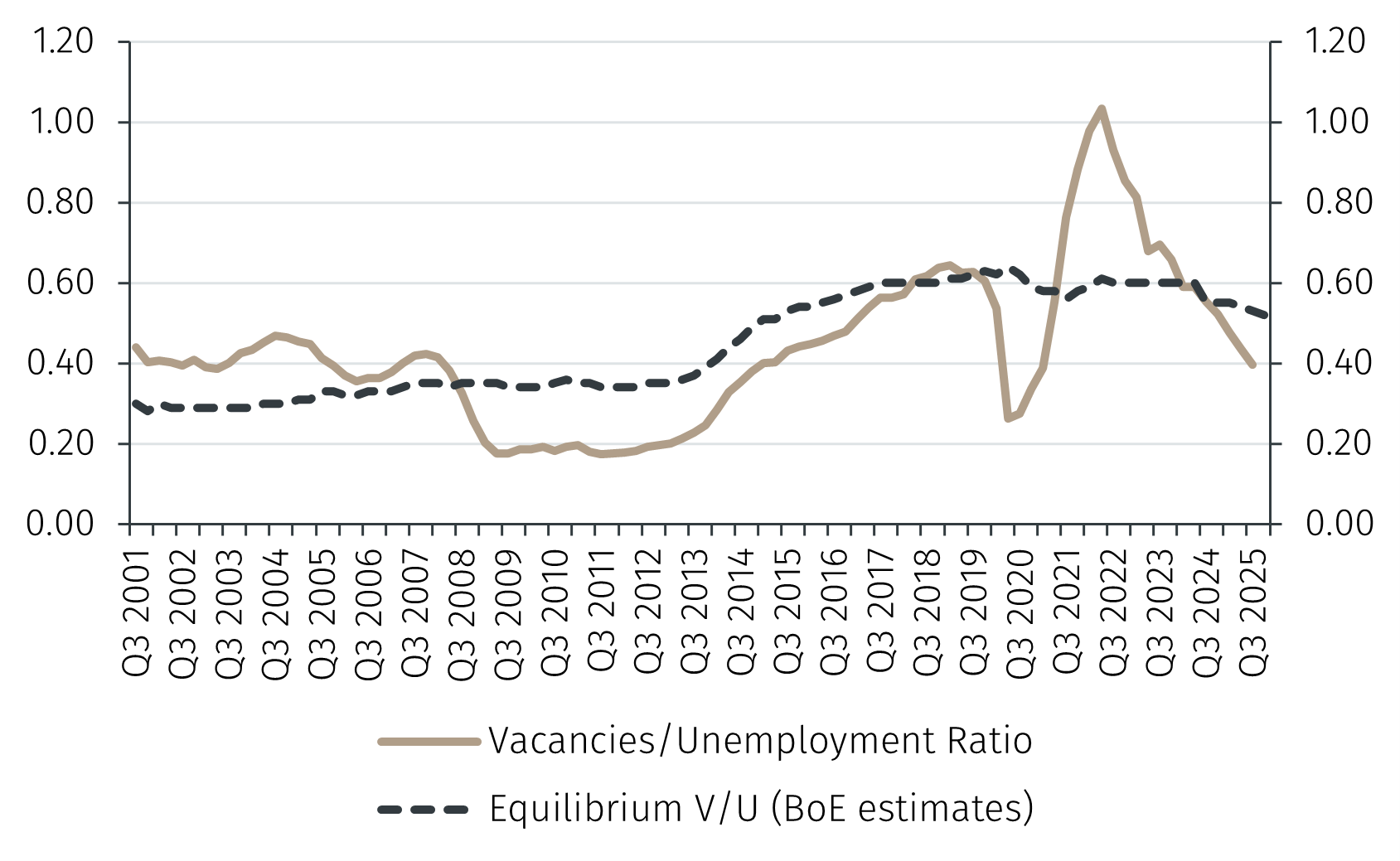

Additionally, wage growth, excluding bonuses, has decelerated to 4.4% YoY in October and the labour market has weakened further. The unemployment rate rose to 5.1% in September, employment declined for the third consecutive month, and the vacancies-to-unemployed ratio fell below the BoE’s equilibrium estimates (see Chart 2).

Chart 2. Vacancies-to-Unemployment ratio as an indicator of labour market tightness

Source: LSEG Data & Analytics and EFG. Data as of 18 December 2025.

A close call

Although the MPC acknowledged that Bank rate is expected to fall gradually, it noted that “judgements around further policy easing will become a close call” from now on. This shows the Committee judges Bank rate to be close to the neutral level and that this will likely be reached in 2026. Some of the comments from MPC members that voted in favour of keeping rates on hold referenced the persistence of wage growth pressures and the potential impact this could have on inflation.

The MPC referenced the impact that some of the measures announced by the UK government in the recent Budget could have on reducing Consumer Price Index (CPI). The one-off reduction in energy bills and charges to fuel duty will contribute to reduce the actual CPI print. This added to downward pressures on oil and gas prices, which are also important inputs for the UK. However, it is important to recognise that these measures will be temporary, and although they will contribute to bring inflation down, they could potentially affect future inflation expectations when they are reversed.

Market response

Communications from the BoE have been clear since the start of the easing cycle in August 2024. MPC members have guided markets and analysts through their assessment of the UK economy, the risks ahead and the balance between a cautious and gradual approach to monetary easing. This has allowed economists to anticipate, with a high degree of confidence, policy decisions ahead of each meeting. As a result, the market reaction to yesterday’s decision was fairly contained, with the pound sterling rising marginally from $1.33 to $1.34, and 2 and 10-year Gilt yields rising from 3.71% and 4.48% to 3.73% and 4.51% respectively.

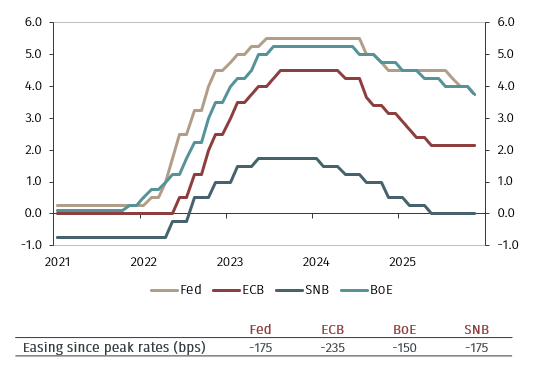

Since the BoE started cutting interest rates in Q3-2024, Bank rate has come down by 150bps, which is less than the level of easing from other major central banks such as the Federal Reserve, the European Central Bank or the Swiss National Bank (see Chart 3). This speaks both to the cautious approach from the MPC, but also to the persistence of inflationary pressures in the UK, which continues to have an elevated level of inflation in relation to the 2% target.

Chart 3. Monetary policy rates in US, Europe, Switzerland and UK (%)

Source: LSEG Data & Analytics and EFG. Data as of 18 December 2025.

Overall, the decision from the BoE to cut Bank rate to 3.75% was anticipated, given the recent weakening in UK economic data. Weak inflation print in November combined with declining employment and decelerating wage growth provided the necessary conditions for what can be labelled as a “hawkish rate cut”. As we move into 2026, the MPC has guided that further rate cuts will be dependent on the evolution of economic data. In the absence of any external shocks, it would be reasonable to expect two more rate cuts by the BoE in H1-2026 as its own expectations for inflation get closer to target in the second half of next year.

1 Core services, as defined by the BoE, include services prices excluding volatile components, rents and packaged holidays. This series is calculated by EFG Asset Management.