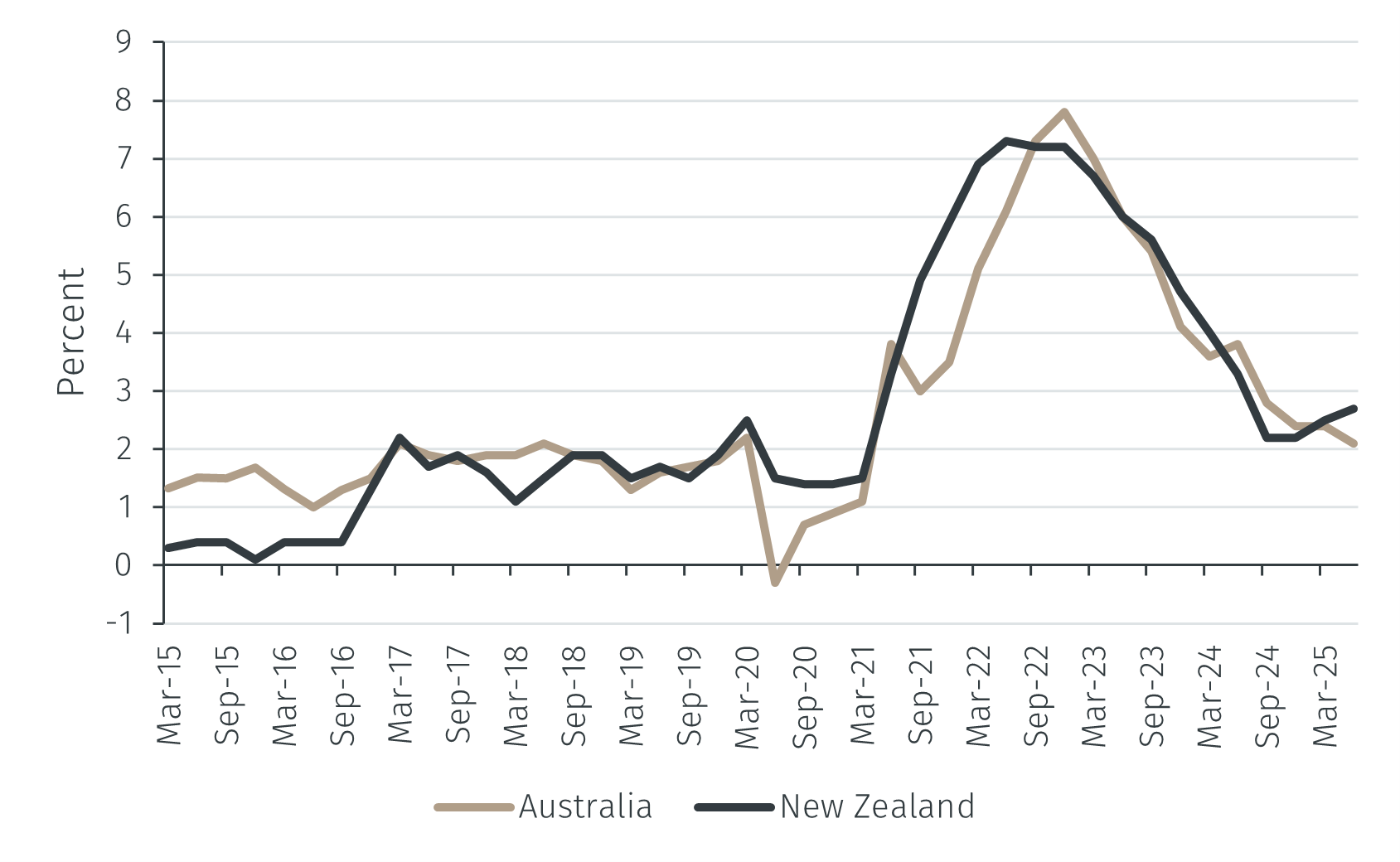

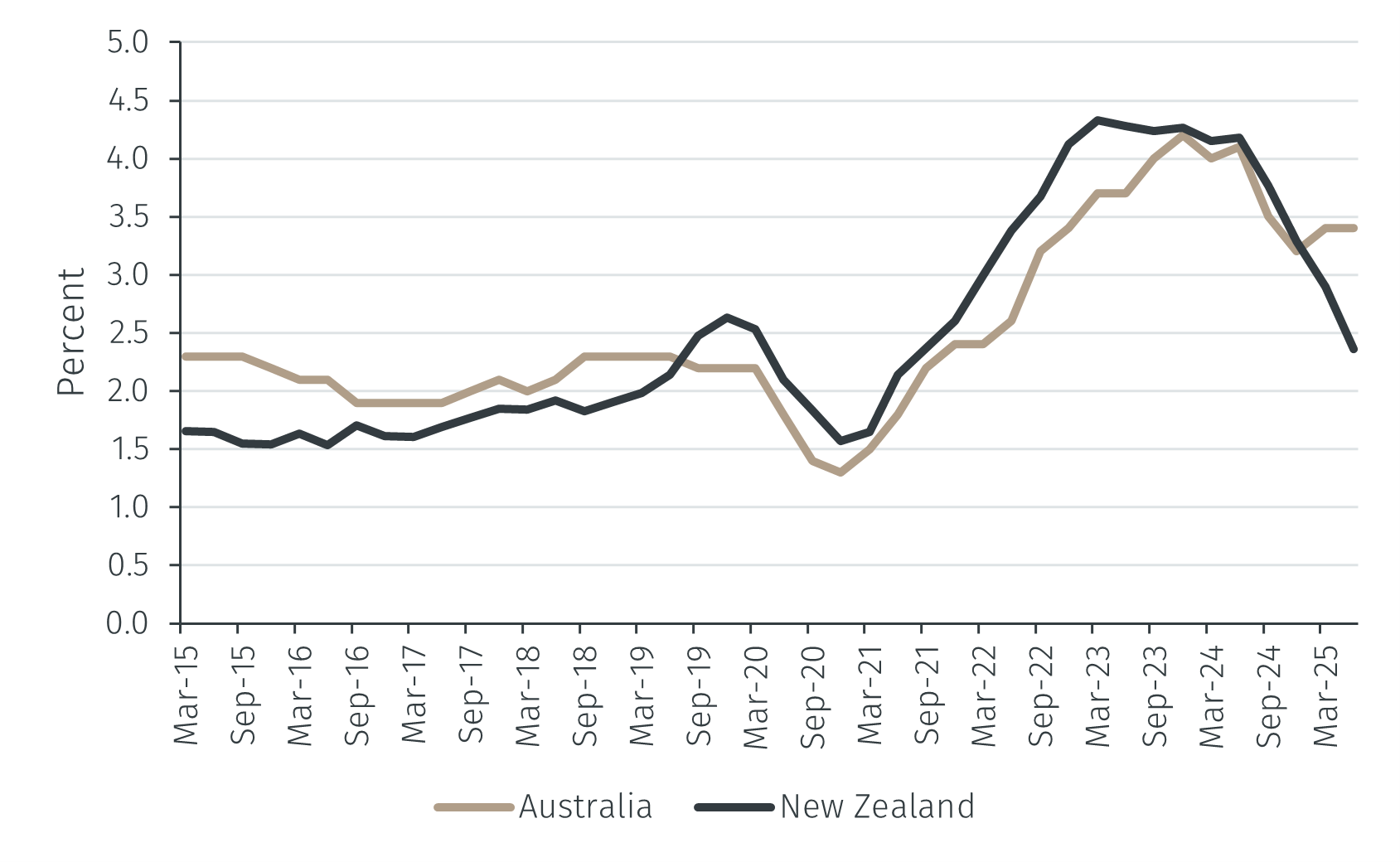

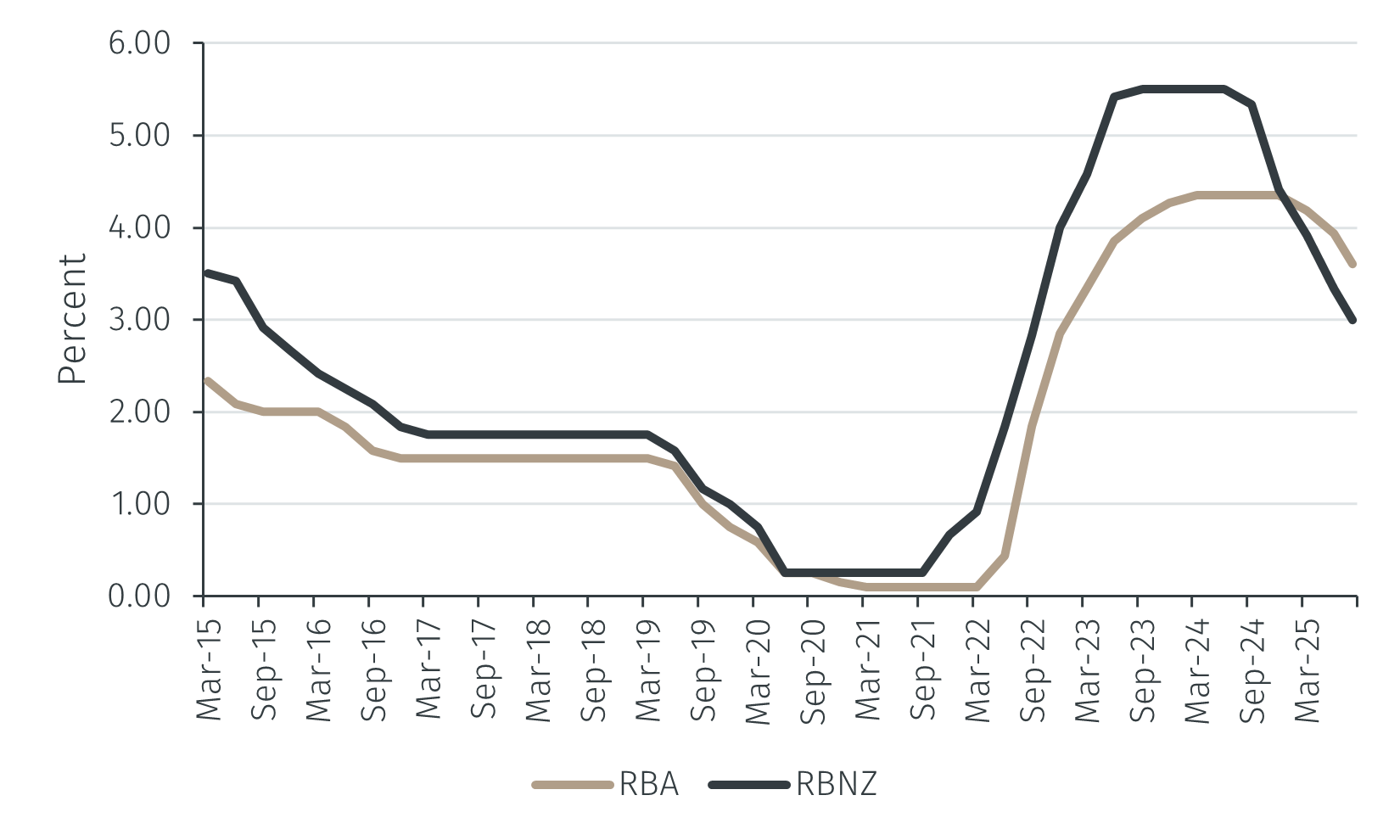

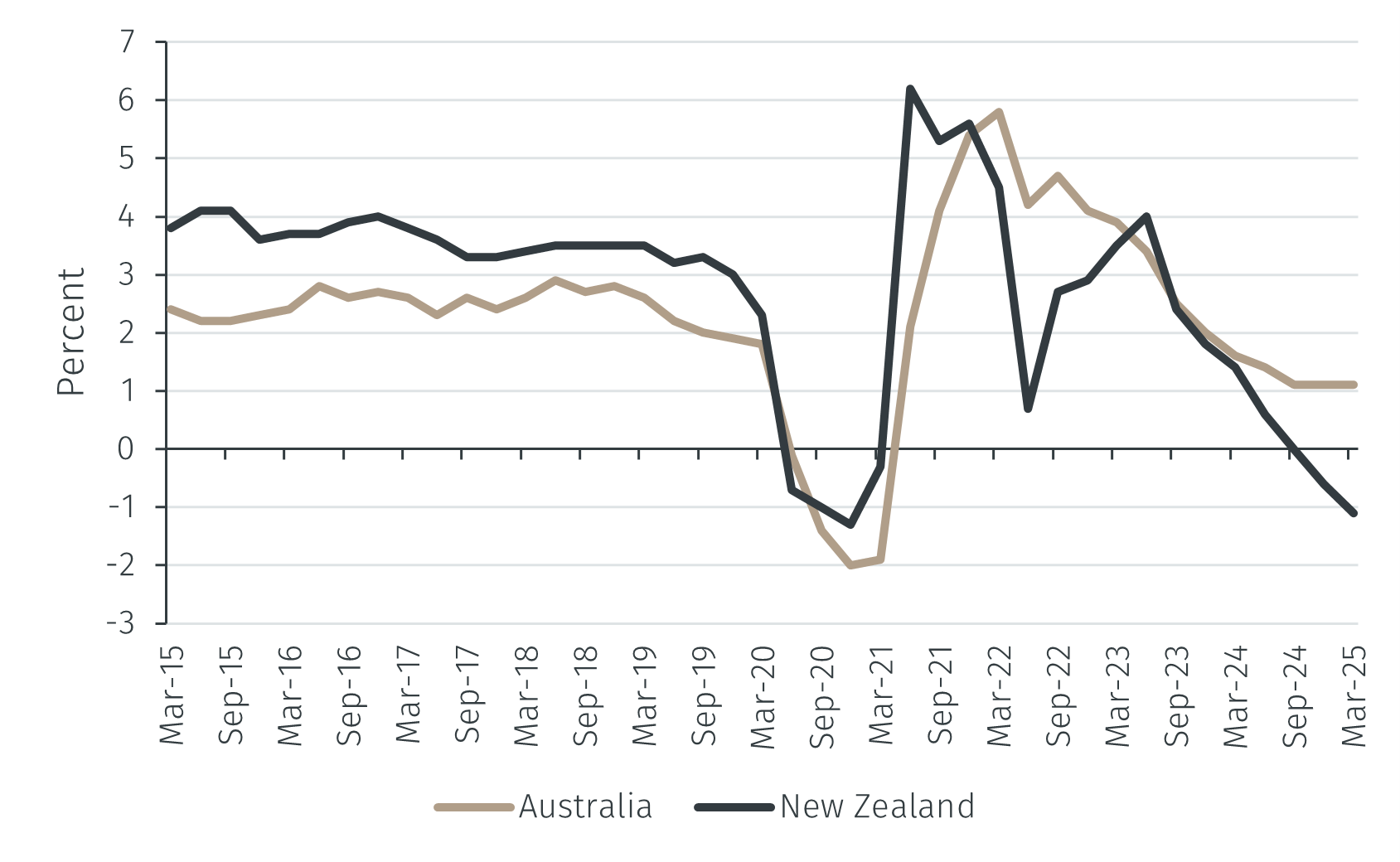

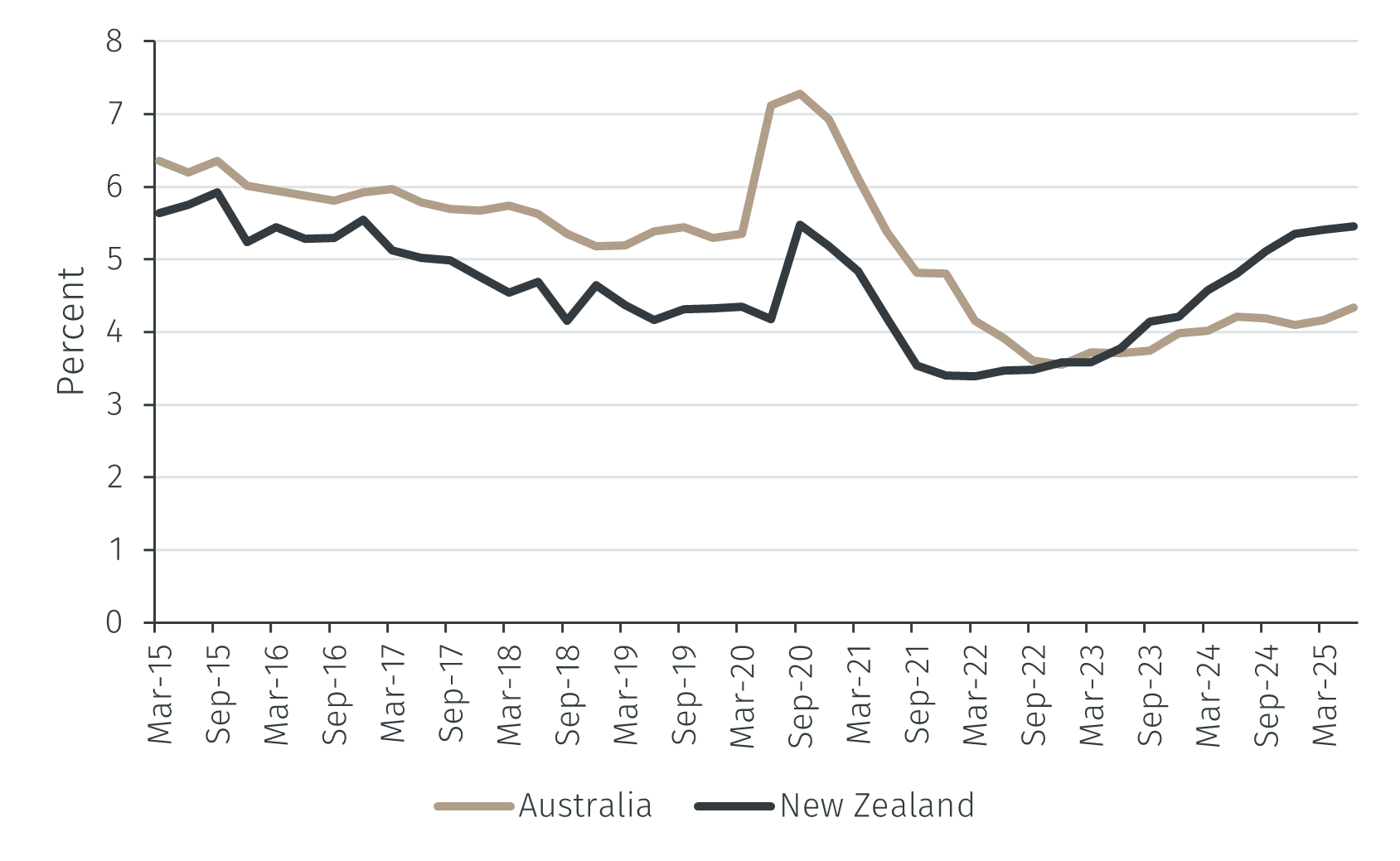

The Reserve Bank of New Zealand (RBNZ) was the first central bank to adopt inflation targeting in 1990, a framework that soon became the global standard. The Reserve Bank of Australia (RBA) introduced its own version a few years later. Since then, both have been seen as leading examples of how small open economies can manage monetary policy in a world of volatile trade, commodity prices, and capital flows.

This note reviews how the two banks have operated in recent years. Their mandates and institutional settings share many features, but the shocks of the past few years - Covid, surging inflation, and tight labour markets - produced different responses. Understanding those differences sheds light on how central banks balance inflation control with support for growth, and what that means for policy in the months ahead.