Central banks in Latin America have overcome different domestic pressures and supply shocks that have affected inflation and activity, driving a divergence in policy since the start of 2025. In this Macro Flash Note, economist Joaquin Thul focuses on the two largest economies within the region, Brazil and Mexico, together with the main countries in the Andean region, Chile, Peru and Colombia.

Latin America Series – Central Bank Update

Investment Insights • Macro

2 min read

Latin America Series – Central Bank Update

Five years after the onset of the Covid pandemic, the outlook for monetary policy in Latin America is characterized by a recent divergence in policy across different countries. In contrast to the global policy coordination after the Covid pandemic, the current setting is one of fragmented policy making reflecting differences in domestic priorities. This has the potential to affect prices and activity.

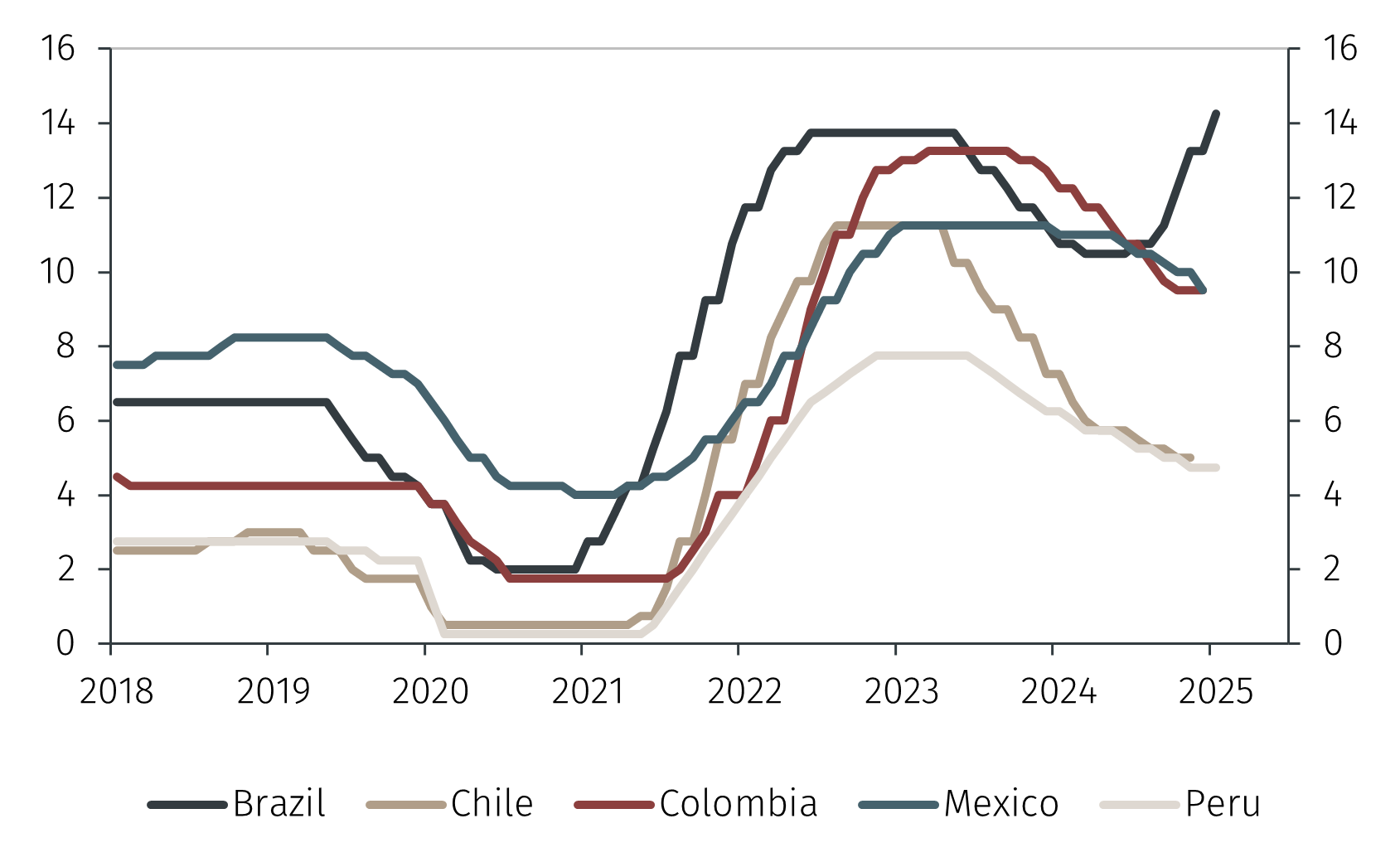

Figure 1. Monetary Policy Rates in Latin America (%)

Source: LSEG Data & Analytics and EFGAM. Data as of 4 April 2025

This group of countries can be divided in three, depending on the recent actions taken by their respective central banks.

- The central bank of Brazil is the only one among this group to be actively tightening monetary policy, increasing the Selic rate by 375bps since September 2024 (see Figure 1). At its latest policy meeting, the Banco Central do Brasil (BCB) hiked the Selic rate by 100bps to 14.25% and committed to at least one more rate hike, although of a smaller magnitude. Inflation in Brazil remains above 5.0%, that is, over the BCB’s 3% target. Although Brazil’s economy grew by 3.4% in 2024, growth slowed more than expected in Q4 2024. This suggests the cumulative impact of rate hikes seems to be feeding through to economic activity. However, the BCB expects the full impact to be reflected in the second half of the year, with GDP growth of 2.0% YoY in 2025.

Despite progress on reducing the primary fiscal deficit from 2.3% in 2023 to 0.3% of GDP in 2024, problems remain on the consolidated fiscal deficit given higher gross debt and interest rate payments. Developments on the fiscal side will remain key to anchor inflation expectations for the rest of 2025. - A second group of countries include Mexico and Colombia. Domestic price pressures, fiscal challenges and external uncertainty have driven Mexico’s central bank (Banxico) and Colombia’s Banco de la Republica (Banrep) to follow a more cautious approach, cutting interest rates seven times over the last 12 months.

Banxico recently cut interest rates by 50bps to 9.0%. It reiterated that although risks for inflation remain titled to the upside, given an environment of increased uncertainty and trade tensions, they have improved. Therefore, another rate cut of a similar magnitude should be expected at the next meeting in May. The recent announcements on US trade tariffs showed that Mexico will remain exempt of extra duties given the existing USMCA trade agreement. This was received positively by Mexican authorities, with the Mexican peso surging by 0.9% against the US dollar and Mexican equities up 2.0% on the day after the tariff announcements, highlighting the positive market sentiment.

In Colombia, Banrep commented that inflationary risks remain and kept interest rates unchanged at 9.5% for the second consecutive meeting. The Board was split between those that wanted to keep rates unchanged and those that voted in favor of a 50bps rate cut, with one vote swinging the decision towards keeping rates on hold. Although core inflation declined marginally from 5.0% to 4.9% year-on-year (YoY), the headline number which includes food and regulated prices remained elevated at 5.2% YoY.

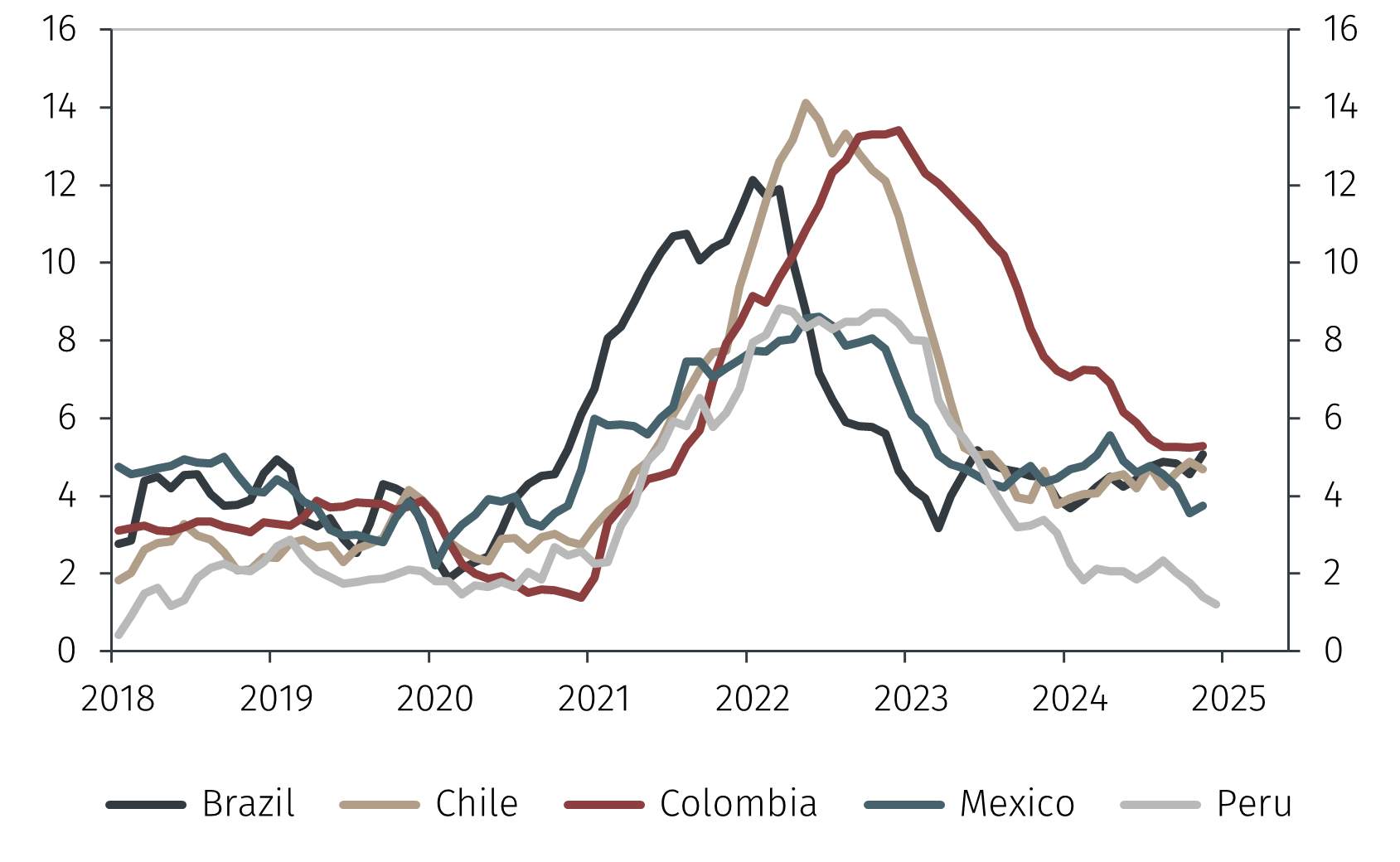

Figure 2. Consumer Price Index inflation rates in Latin America (% YoY)

Source: LSEG Data & Analytics and EFGAM. Data as of 4 April 2025

The decisions in Mexico and Colombia to cut rates seven times in the last year reflect a cautious view of the external environment. It is not a coincidence that both these economies are among those in the region with closest trade links with the US and potentially will be the most affected by a global trade war.1

- Finally, in Chile and Peru the central banks have kept interest rates on hold, although for different reasons.

In Chile, the Banco Central de Chile kept interest rates unchanged at 5.0%, highlighting the need for continued tight monetary policy given upside risks to inflation. Price pressures remain elevated, with inflation up by 4.7% YoY in February, driven by strong growth in housing, food and beverages, and services such as restaurants and hotels. Inflation is not expected to converge to the 3% target until Q1 2026, with the economy being stronger than expected, driven by solid consumption and exports.

Peru, on the other hand, has seen a continued slowdown in inflation from 2.3% in November 2024 to 1.5% in February 2025 (see Figure 2). This reflected a decline in food and transport prices and meant that inflation has remained within the target range for the last year. The Central Bank of Peru (BCRP) maintains that the effects from the supply shocks in 2022 and 2023 have receded and inflation is expected to remain within the target range in 2025 and 2026. Therefore, the BCRP has maintained the reference interest rate at 4.75% in the last two policy meetings. It has stated that future interest rate adjustments will depend on upcoming data.

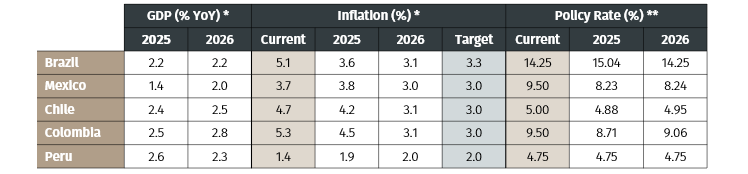

Table 1. Economic data summary

* IMF projections / ** Median market consensus, collected by JPMorgan

Source: LSEG Data & Analytics and EFGAM. Data as of 4 April 2025.

Overall, central banks in Latin America are facing diverse economic conditions, being at different stages in the cycle. As such, monetary policy is diverging across the region, creating opportunities for investors in countries such as Mexico, while the context for Brazil remains more uncertain. Aside from Mexico, the rest of the economies analyzed will be subject to an additional 10% on tariffs on exports to the US which will impact GDP growth in 2025. This is significantly lower than the tariffs announced for other emerging economies, particularly in Asia. Although this represents a positive development in the context of a potential trade war, it reflects the lower proportion of trade between the US and Latin America.

1 As of the end of 2022, the US was the destination of over 60% of Mexico’s goods exports and over 25% of Colombia’s goods exports.