The United States is running large budget deficits. In the spring, before the “Big Beautiful Bill” became law, the Congressional Budget Office projected that federal debt would rise from about 120 percent of GDP in 2025 to more than 150 percent by 2055. Forecasts are uncertain, but the debt is already very large, growing fast, and must at some point be brought under control. The question is how.

Most commentators regard a US default as so unlikely that it is barely discussed. There are no signs that investors fear the United States will struggle to meet its debt obligations. The Treasury market is deep and liquid, and the dollar remains the world’s reserve currency. Yet the United States has, in practice, defaulted before. Creditors were repaid on less favourable terms than agreed. The precedent of the 1933 abrogation of gold clauses is worth recalling.

Three points are useful to bear in mind. First, markets rarely anticipate defaults. They tend to happen, as Ernest Hemingway wrote of bankruptcy, “gradually and then suddenly”. For investors in US debt, it is prudent to think about what seems unthinkable, not because it is likely but because it is possible.

Second, if a US default were to occur, it would almost certainly be partial and presented under another name, perhaps as a fair adjustment or a necessary correction.1

Third, a precedent exists in trade policy. Tariffs have been justified as necessary for fairness.2 In 2023, Stephen Miran, now chairman of the Council of Economic Advisers and nominated by President Trump to serve as a Governor of the Federal Reserve, applied the same reasoning to debt markets. He suggested a “user fee” on foreign official holders of Treasury bonds to weaken the dollar and compensate the United States for the security it provides.3 If applied to existing bonds, it would reduce payments to creditors much like a partial default. His senior policy role shows that such ideas can no longer be dismissed as academic.

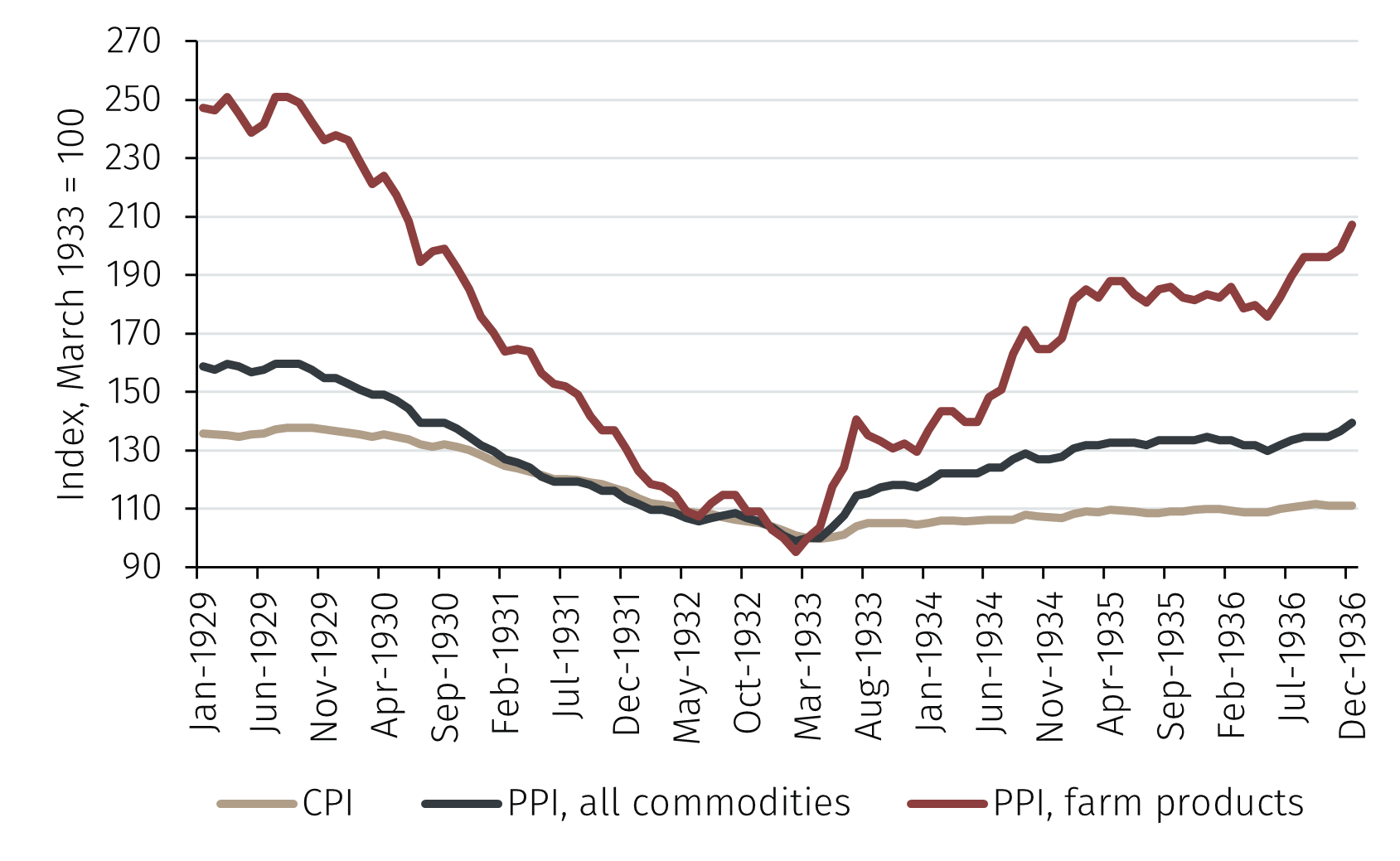

A precedent from the 1930s

In 1933 the United States was in the grip of the Great Depression. A central problem was the relentless fall in prices, which increased the real burden of debt and made it harder to service. Firms, banks, and households that had borrowed expecting prices and wages to keep rising instead saw them collapse. Debts grew heavier in real terms, forcing sharp cutbacks in spending, triggering defaults, and contributing to mass unemployment.

President Roosevelt saw that ending the downward spiral required higher prices, especially in agriculture. But with the United States on the gold standard since 1900, this meant devaluing the dollar, which in turn required breaking its link to gold.4