The BoE’s MPC voted on 07 August to cut Bank Rate by 25 basis points to 4.0%. The decision was widely anticipated by markets. However, minutes from the meeting reflected the divergence among MPC members over their assessment of economic data.

Although MPC members agreed there has been a substantial progress on bringing down inflation closer to the 2% target over the last two and a half years, the split vote reflects the differences in how policymakers interpret recent data and where the risks to inflation lie.

UK activity has been weak, which has been consistent with the loosening in the labour market. This has offset the strong growth in the first quarter of 2025, which was attributed to domestic front-loading ahead of expected rises in taxes and international trade tariffs.

The arguments behind the decision

The Committee was initially split in three ways, with four members voting to maintain Bank Rate at 4.25%, four members voting to cut Bank Rate by 25 basis points and one member voting to cut Bank Rate by 50 basis points. A second round of voting was required to secure a majority decision. This time the motion was limited to either maintaining Bank Rate unchanged or reduce it by 25 basis points. The latter was then supported by five members. This was the first time, since the MPC was formed in June 1997 that a second round of voting was required to reach a majority.1

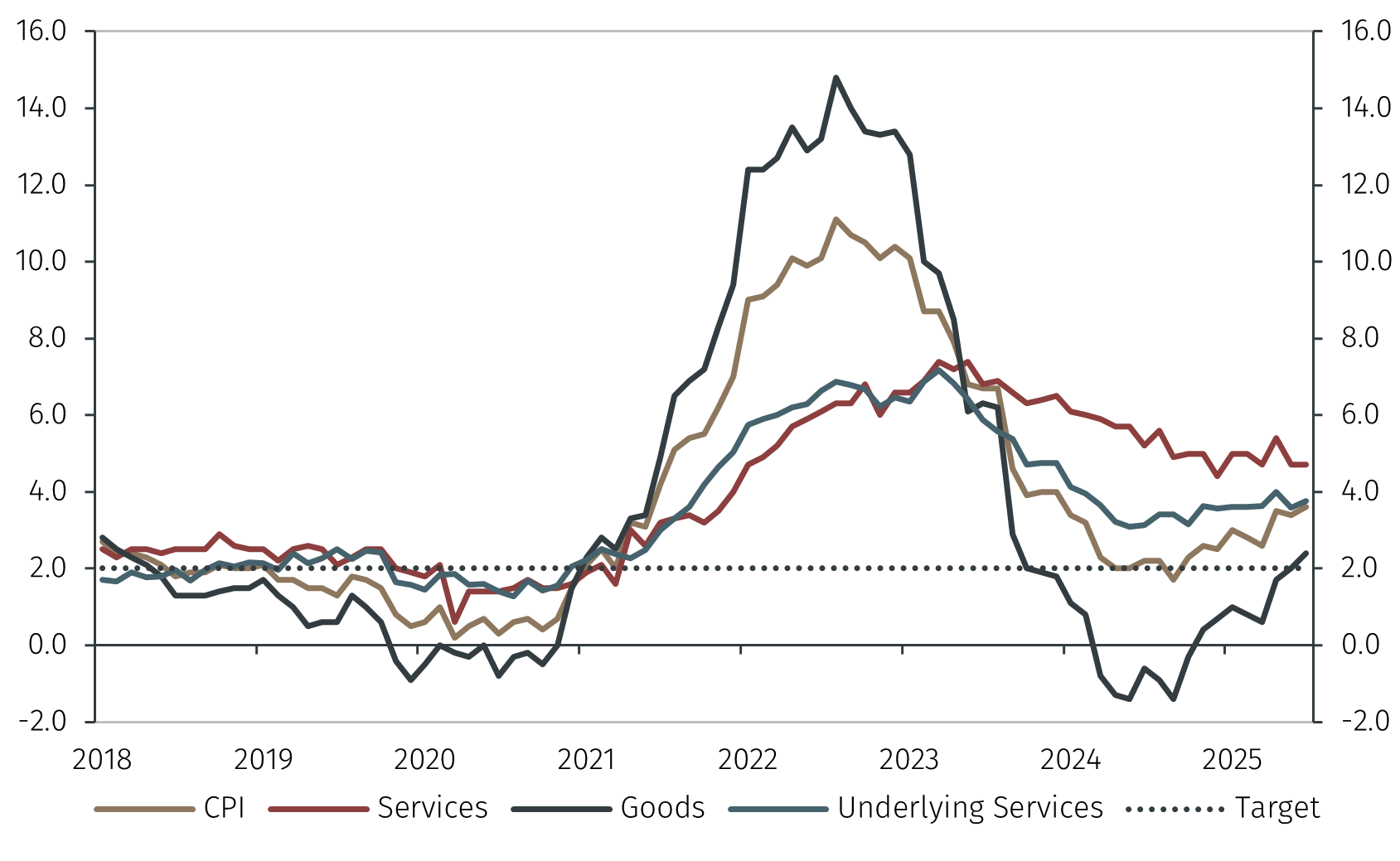

Minutes from the meeting highlighted the deceleration in services prices since the peak in 2023 and the softening in wage growth over the last months, although to different degrees. Data shows that headline Consumer Price Index (CPI) inflation accelerated to 3.6% year-on-year (YoY) in June from 3.4% YoY in May. However, services inflation remained elevated at 4.7% YoY. BoE’s estimates show that over half a percent of the rise in services prices can be attributed to administered prices, in particular vehicles excise duties.2

Therefore, to assess the developments of underlying service inflation we constructed a measure of services inflation that exclude components such as administered prices, indexed and volatile components, rents and foreign holidays. For simplicity, we have called this series Underlying Services, see Chart 1.3