Oil price dynamics

Historically, growth in the Gulf Cooperation Council1 (GCC) economies has been anchored in hydrocarbon production and exports. Oil and gas production accounted for approximately half of the region’s total gross domestic product (GDP) and as much as 70% of total government revenues between 2011 and 2015.2

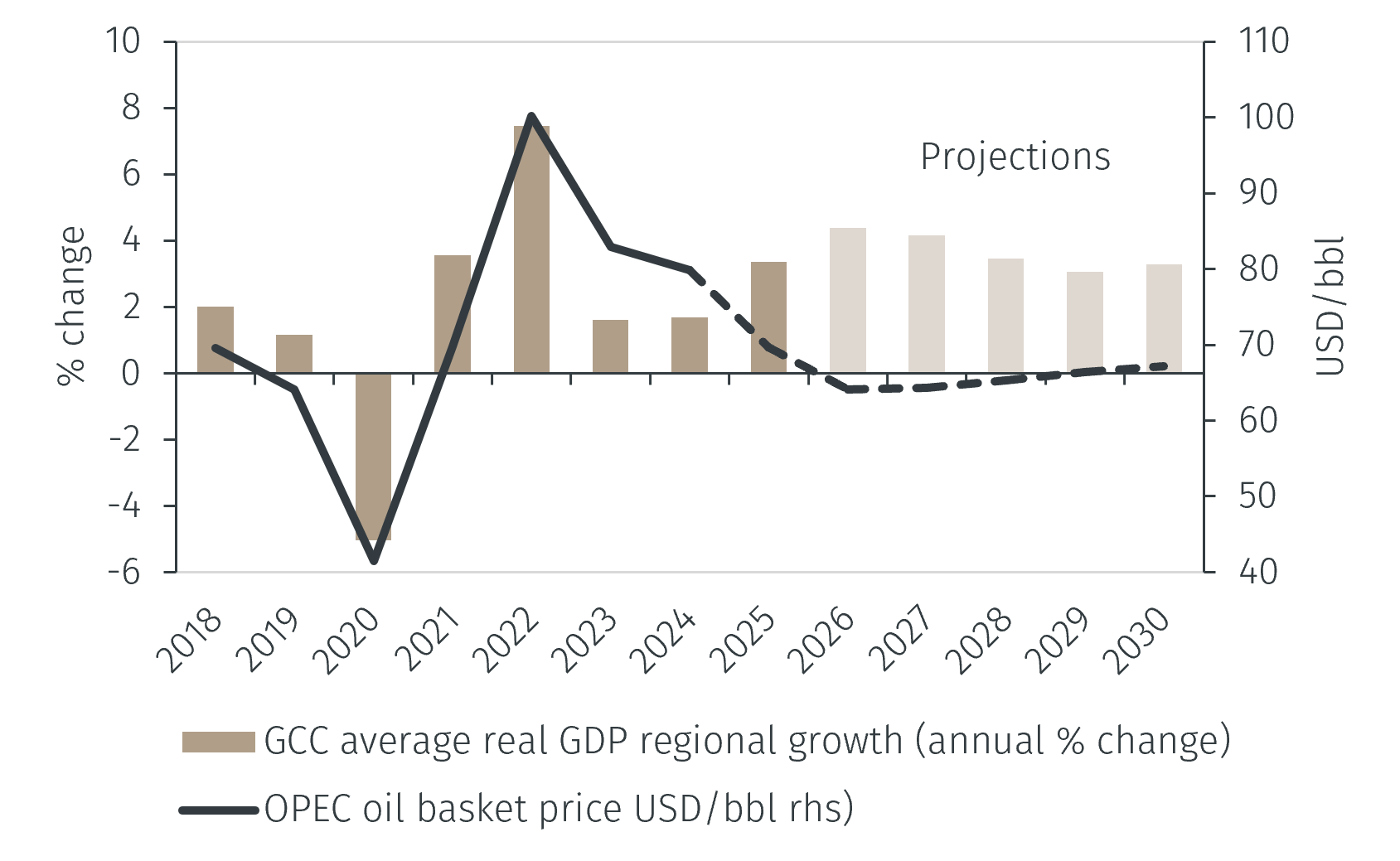

As such, GCC economies have been directly exposed to fluctuations in global oil prices. While this has generated large fiscal surpluses during episodes of strong oil prices, periods of price declines have led to a deterioration in fiscal positions and growth prospects, underscoring the need for more sustainable growth drivers. It is therefore positive that the proportion of GDP growth and government revenues accounted for by oil and gas production have declined over the last decade.3

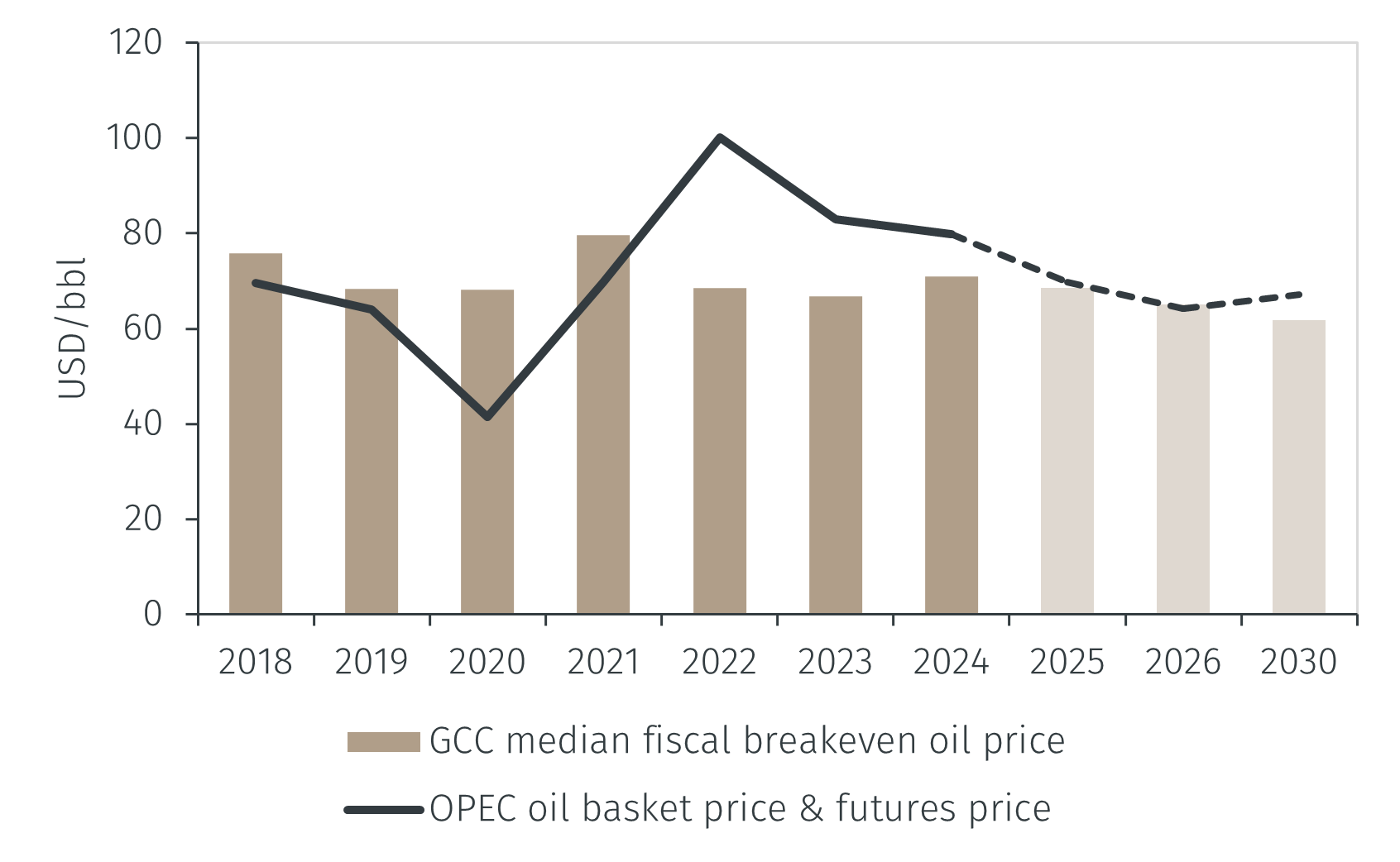

In recent years, OPEC4 oil prices have fluctuated, ranging between 59 and 128 USD per barrel (USD/bbl), contributing to narrower fiscal surpluses across the Gulf. The regional median fiscal breakeven oil price is projected to decline from about 70 USD/bbl in 2025 to 62 USD/bbl in 2030 (see Chart 1). This downward trend reflects fiscal consolidation and diversification efforts that are gradually improving the region’s ability to sustain growth amid lower oil revenues.