Federal Reserve Chair Jerome Powell spoke on Friday 22 August at the Federal Reserve Bank of Kansas City’s annual Jackson Hole symposium.1 Markets were eager for any indication of a rate cut ahead of the Federal Open Market Committee (FOMC) meeting on 17 September. While Powell does not set policy outside of formal meetings, his remarks are usually the best guide to the Committee’s thinking. He stopped short of making any commitment but suggested that the Fed may be preparing to ease policy in September, saying that “the shifting balance of risks may warrant adjusting our policy stance.”

A more definitive signal would have constrained the FOMC. The arguments for and against a rate cut remain finely balanced, and labour market or inflation data over the next few weeks will affect the decision. The next Personal Income and Outlays release is on 29 August, the JOLTS survey is due on 03 September, the Employment Situation report on 05 September, the producer price index report on 10 September, and the consumer price index (CPI) report on 11 September. With the FOMC meeting scheduled for 17 September, Powell left scope for those releases to shape the final decision.

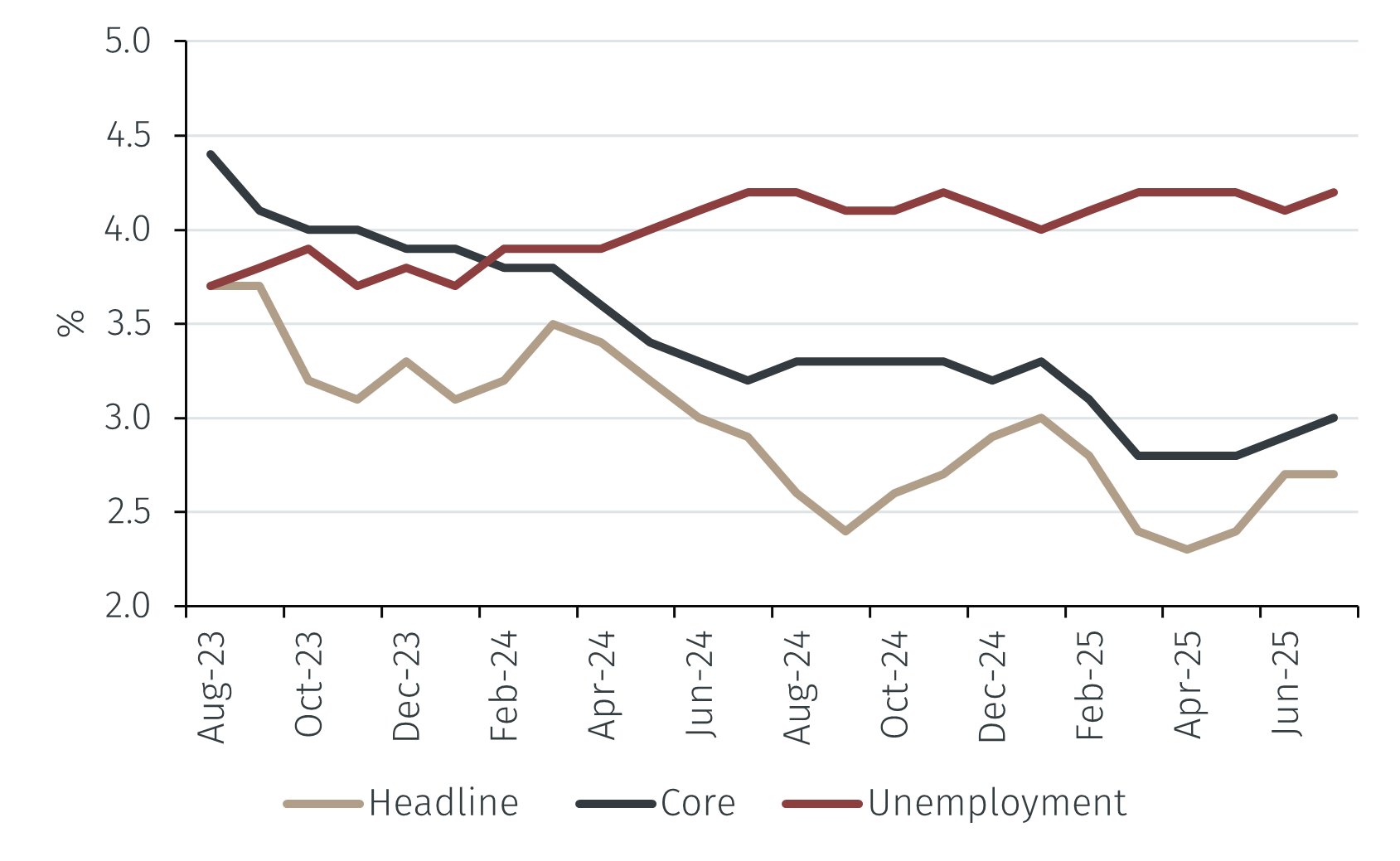

Powell’s assessment of the economy was measured. Inflation has fallen substantially from its post-pandemic highs but is not yet back at the 2% target.2 Since August 2023, headline CPI has declined from 3.7% to 2.7%, while core CPI has fallen from 4.4% to 3.1%, but both remain above target. Tariffs appear to be exerting some upward pressure on prices, though their full impact is highly uncertain and dependent on evolving trade policy.